Investment thesis

Equinor ASA (NYSE:EQNR) is up +25% since my prior article from April (total return) and this European major also beat earnings on Friday. So is Equinor still a buy?

While I remain long-term bullish, I think over the next quarter the risks may be more weighted to the downside:

- Barring a major escalation of the conflict in the Middle East, the political risk premium baked into European TTF natural gas prices may quickly dissipate and cause a downward correction;

- The “come to Jesus moment” in offshore wind hasn’t left Equinor unscathed either and the company has already recorded an impairment related to its renewables business; the dust hasn’t yet settled in this sector;

- The generous capital returns will continue but this is a distribution of excess cash earned in the past; this cash pile is “static” and won’t change the company’s valuation.

In the meanwhile, the stock us up +25% since April while Wall Street’s targets have come down -10%, so the upside potential isn’t as great as before. I now view EQNR as a “hold.”

What are the highlights from Equinor’s Q3 earnings?

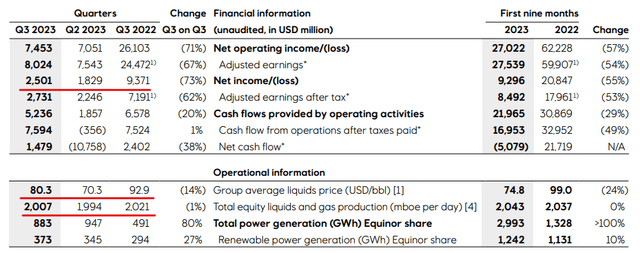

Net income in Q3 was up sequentially from Q2, but still down a lot from Q3 2022:

Equinor Q3 Report

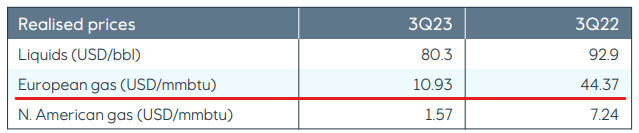

The 73% year-on-year drop isn’t driven by oil prices which have stabilized after the OPEC+ cuts. It has a lot more to do with the European TTF gas prices:

Equinor Investor Presentation

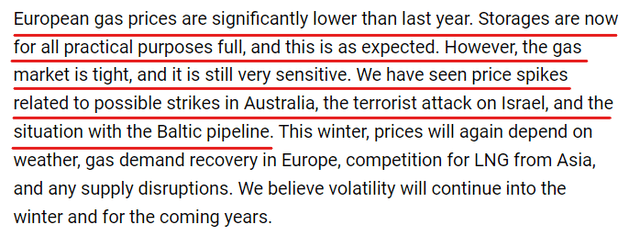

This was also acknowledged by management during the Q3 earnings call:

Seeking Alpha

We will come back to the gas market tightness point in a bit. Management also acknowledged the difficulties in its offshore wind segment due to inflation, high interest rates, and supply chain issues. As known, New York State denied the requests from Equinor and Orsted (OTCPK:DNNGY) for higher rates on a couple of offshore wind projects. I wrote about Orsted’s woes here, but Equinor faces the same issue. It’s just that Orsted is a 100% renewables company whereas for Equinor the wind business is fairly small proportionally.

Lastly, management re-affirmed the capital distribution plans. For Q3, the ordinary cash dividend is $0.30 per share but there is also an extraordinary dividend of $0.60, for a total of $0.90. This is about 11% annualized cash yield, but, again, note that the base part is only the 3.57% reported by Seeking Alpha. Including buybacks, management is looking at a total capital distribution of $17 billion for 2023 or about 17% of the current market cap.

Can TTF survive another warm winter?

In 2022, when TTF was briefly at 100 USD/MMBtu, the question dominating energy headlines was whether Europe would survive a cold 2022/23 winter. This time around, after one year of pain for natural gas bulls, we probably have to flip the question around and ask if gas prices can survive a repeat of last year’s warm winter.

After the major crash from the 2022 highs, European gas indeed bounced over the last few weeks due to the factors mentioned by Equinor’s management:

Barchart

While there’s no comparison to 2022, it is a +100% jump from this summer’s lows and this remains a very high price level historically.

However, from the factors singled out by management, the Australian strike for now appears to be over. The suspected Baltic line sabotage affects a connection between Finland and Estonia. Neither is a huge market and I’m not sure exactly how more sabotages would be bullish for Equinor as the latter also relies on subsea pipelines to export to most of its European customers. Finally, Israel’s halt of production from the Tamar field in the EastMed seems to be affecting Egypt’s LNG exports to Europe, but that represents less than 1 bcf/d. Compare that to 11-12 bcf/d and rising that is regularly exported out of the U.S. The risk premium is perhaps more due to fears of a major escalation that would affect Qatari volumes through the Strait of Hormuz.

In the meanwhile, the EU gas storage is now 99% full. With no rush from European heavy industry to ramp up given the economic slump that has taken hold over the continent, it would probably take a very cold winter to keep TTF at these levels or higher. As heating season has barely started in Europe, an elevated premium probably makes sense, but I feel the risk is more on the downside as we get deeper into the winter.

Offshore wind is a mess

I wrote more about the structural challenges ahead of the offshore wind industry here, but Equinor makes no exception among the other wind players. From the earnings call:

Our petition to New York for price adjustment of projects on the U.S. East Coast was denied together with similar petitions from many other developers. Contrary to in the UK and Poland, offtake contracts here or in the U.S. are not inflation-adjusted.

So, based on this, we have taken an impairment on the U.S. East Coast projects. We are now assessing the impact of New York’s decision, and we are working closely with the state as they further develop their 10-point action plan to expand and support the renewable industry.

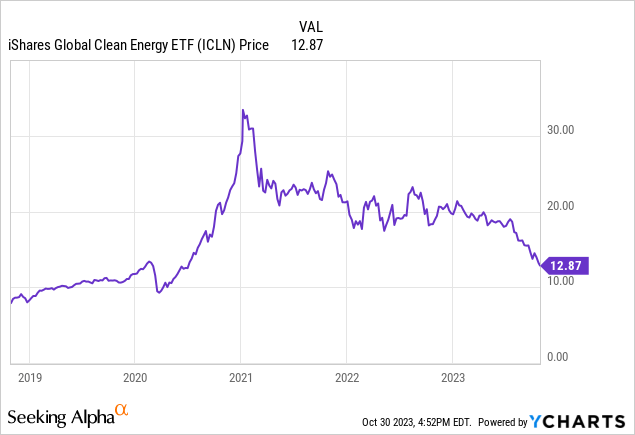

The impairment in question was about $300 million, which isn’t much on Equinor’s scale, but, unlike management, I don’t see the woes of the renewable industry as coming to an end. The iShares Global Clean Energy ETF (ICLN) remains in free fall:

Markets are waking up to the fact that wind technology has so far shown little ROI and are starting to punish every piece of bad news as just recently happened to Siemens Energy (OTCPK:SMEGF), after they announced they may look for government support.

For now, wind isn’t a big part of Equinor’s P&L, but management is obviously still committed to big capital expenditures in the area. In other words, further impairments shouldn’t be excluded as a possibility.

The risk-reward now appears more modest

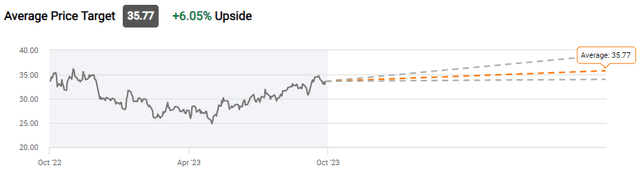

In April, Equinor was trading at $27 and the Wall Street average target was $38, implying +33% upside. Now, EQNR trades at $34 but the average target has come down to $36:

Seeking Alpha

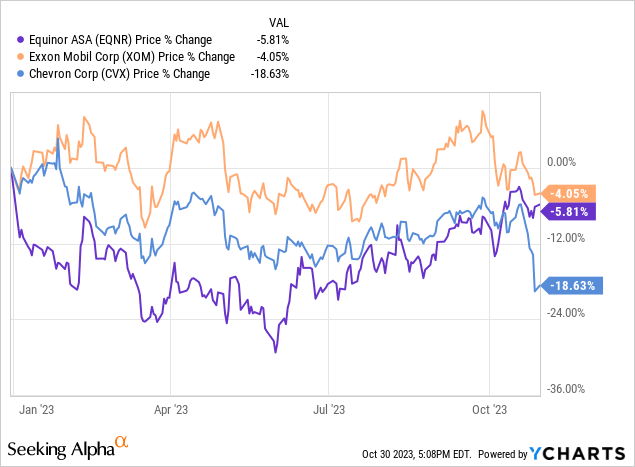

Moreover, while for the first part of the year Equinor’s relative performance was lagging behind other peers, EQNR has now practically caught up with Exxon (XOM) and is already outperforming Chevron (CVX):

There is some mean reversion in these relative performance comparisons, and my base case is that Equinor may continue sideways but is not necessarily such a compelling value as six months ago. That isn’t a reason not to hold as the long-term outlook for energy remains bullish, but I personally have now closed out my position to focus on more obviously undervalued opportunities.

Bottom line

Despite standing by its renewables agenda, Equinor remains a cash cow and will return 17% of its market cap to shareholders this year. However, in the near term a significant upside for Equinor would require a very cold winter in Europe and multiple LNG supply failures around the world. To me the European gas prices probably have more risk to the downside and we may also continue to get negative offshore wind news. That is why I consider Equinor to be a “hold” for the time being; a downward correction may make it a more convincing “buy” again.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here