Introduction

The share price has been quite volatile for Employers Holdings, Inc. (NYSE:EIG) for the last 12 months as the company is finding its footing and growing the bottom line very well. Since the report back in late July showing EIG able to quickly raise the bottom line to a positive level, the market has reacted by valuing the company higher. I wouldn’t say that EIG looks particularly expensive right now, as the company is only at a FWD p/e non-GAAP of 11. If the labor market continues to showcase a lot of resilience, I think EIG will be able to continue to grow very well over the long-term.

The company has also been distributing a dividend consistently over the last couple of decades. I think that given the quite low payout ratio of under 30%, the 2.7% yield is sustainable and will bring further value to investors and a good reason to invest. I like the business model and trajectory of EIG right now and will be rating it a buy.

Company Structure

EIG along with its subsidiaries, plays a prominent role in the commercial property and casualty insurance sector, with a primary focus on the United States. The company’s operations are divided into two key segments: Employers and Cerity. Within these segments, EIG provides essential workers’ compensation insurance services to small businesses operating in low to medium-hazard industries. These services are offered under both the Employers and Cerity brand names, catering to the specific needs of their clientele.

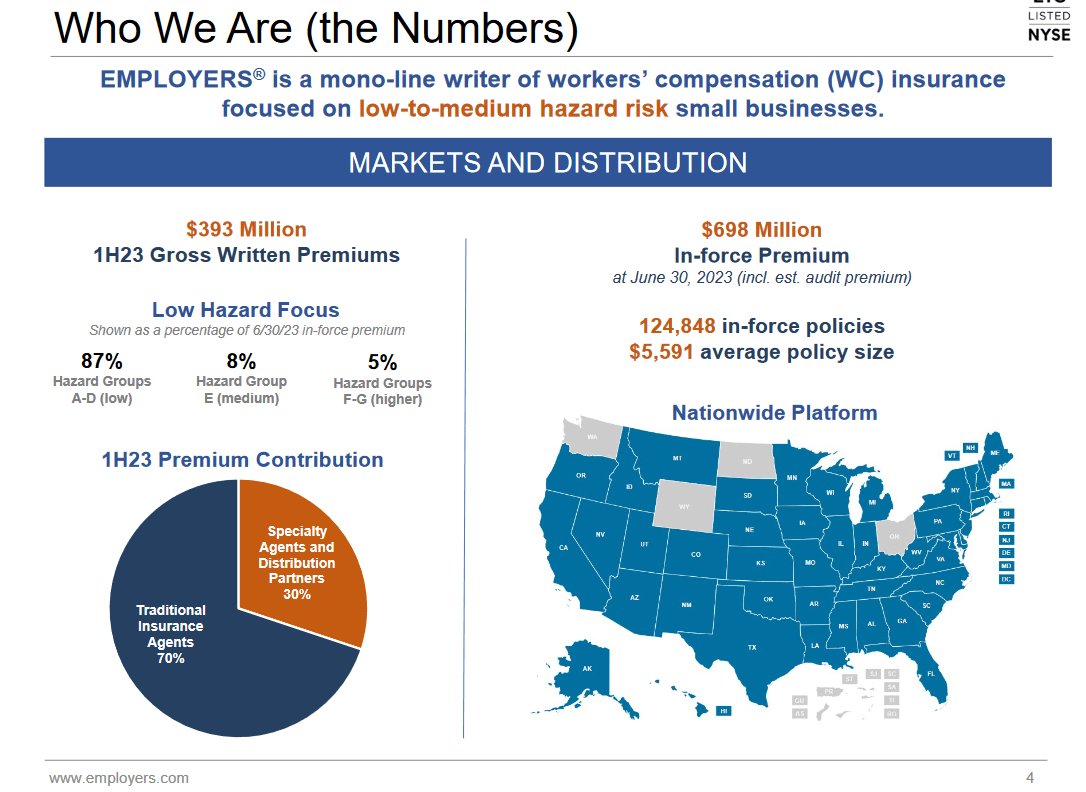

Company Numbers (Investor Presentation)

EIG faced significant challenges during the pandemic, primarily due to its substantial business operations in California and its focus on industries like restaurants and hotels. Unfortunately, these sectors experienced severe employment disruptions due to California’s stringent lockdown policies, impacting EIG’s bottom line. The company grappled with the economic fallout resulting from reduced business activity and increased insurance claims during this challenging period.

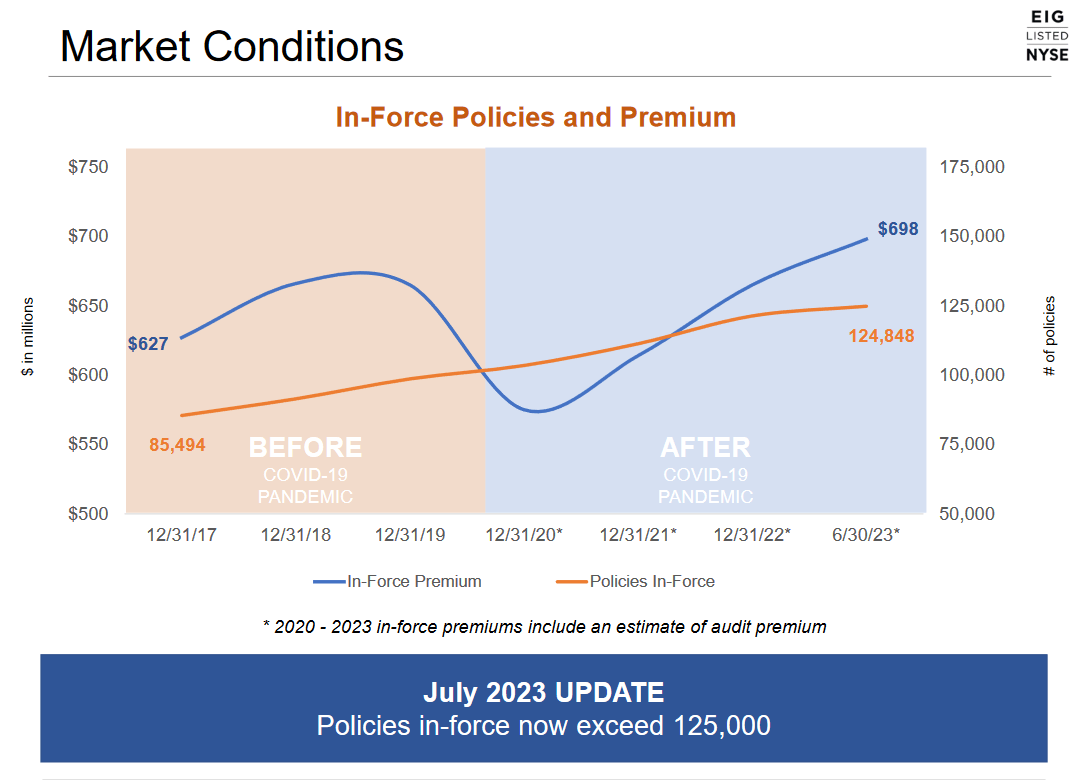

Policies (Investor Presentation)

The strength of the labor market has been clearly shown for EIG and the in-force premiums have risen steadily since 2017. Besides this, the policies in force have climbed very well to and sit at over 125,000 as of July 2023. If this is a trend that can continue, then I think the market will reward it with the premium it currently trades at. It’s almost viewed as a growth company right now.

Earnings Transcript

Back in late July on the 27th, the last earnings call was held by the company and the CEO of EIG Kathy Antonello had some very valuable insights on the company’s recent performance and where they are heading right now.

Wage increases a strong labor market, our thoughtful appetite expansion program and our new sales and underwriting operating model each contributed to this growth. As a result of these efforts, we ended the quarter with yet another record number of policies in force. And just last week, we celebrated achieving over 125,000 policies in force. Our net investment income was up 34%.

As said earlier, the last quarter for the company was a success with the net income reaching $34.9 million for the quarter, a massive improvement from the negative $15.6 million it was just a year prior. The company was heavily affected by the pandemic but seems to be on the recovery track, the expansion programs EIG has set in place seem to be paying off very well I think right now.

The sharp increase was primarily due to higher market interest rates impacting bond yields and higher invested balances of fixed maturity securities. We earned $27 million of net investment income during the quarter, an amount highly consistent with that of the quarter, with each being meaningfully higher than any other quarter in our history as a publicly traded company.

It wasn’t just the stronger labor market that yielded EIG a solid bottom line in the last quarter. It was also their efficient and strategic investments that made it a reality. If this is something that can be sustained for the business, I think a higher markup and premium is applicable here. Going into the coming quarters, I will be watching this quite a lot as it made a significant impact on the last earnings result with $27 million additional income.

Valuation

Furthermore, regarding the valuation of the company, I think it looks quite appealing. One of the common things I look at is the FWD P/B, which right now sits at 1. This is right in line with my preference and makes it a buy as a result. The given I have 1, or when possible below that as a threshold is given that many financial companies have their earnings potentially determined by their balance sheet, then paying a fair value, meaning 1 or lower is crucial here. With EIG I am getting that right now and as long as it stays at 1 or under I find enough value to make it a buy. To expand on the value here, the dividend is a strong appeal as well, which right now is above 2.7%, and together with shareholder returns like share buyback, investors are getting a solid deal here in my opinion. Recently the company has been growing its net income very well as a result of higher interest rates I do think rates are staying higher for some time and that will help deliver potentially even stronger earnings for EIG if their loan growth continues, which it recently seems to have been doing very well.

Risk Associated

Where I see some risks is the ongoing current climate, more specifically I’m concerned about the ongoing pressure on rates, especially with the likelihood of accident frequency returning to normal levels, which could lead to increased claims. While the last quarter showed a strong improvement in the bottom line, any signs of a slowing labor market or worsening economic conditions could potentially lead to a slide in the company’s share price as investors become more cautious about the future outlook.

The unemployment rate seems to be climbing again. This is most likely a result of the continued high interest rates in the country, which is taking a toll on companies and making cutting expenses a necessity right now. Furthermore, my concern extends to the pricing dynamics in the market and the potential for an uptick in both loss frequency and severity. If we observe a deterioration in the labor market, it could have a direct impact on EIG’s earnings growth potential. Consequently, this might necessitate a valuation adjustment, with the possibility of a lower valuation for the company. With the company already trading at a premium based on earnings compared to the sector, I think there is potentially more downside risk right now.

Investor Takeaway

Right now, I think that EIG exhibits an appealing buying opportunity as the company is both able to distribute a strong dividend yield and grow on the back of favorable market conditions. On a valuation basis, the company is trading at a premium to the sector, but I think a P/E of around 11 is fair to pay given the quality of the business and how well the management of EIG has been at capitalizing and growing the policies in force. I think that investors have a lot to gain from EIG and will be rating it a buy as a result.

Read the full article here