The Eaton Vance Floating-Rate Income Trust (NYSE:EFT) is a closed-end fund, or CEF, that can be employed by those investors who are seeking to earn a high level of current income from the assets in their portfolios. This is evidenced by the fund’s current 11.48% yield. This is easily much higher than most assets generally favored by income investors, but unfortunately any time a fund obtains a yield that is higher than 10%, it is considered to be a sign that the market expects that the fund may be forced to cut its distribution in the near future. However, as I mentioned in a previous article, that rule may not be as true today as it was a few years ago due to the simple fact that yields on everything are much higher than they were a year ago. We should still make sure that we analyze the fund’s finances to ensure that it is not overdistributing.

As regular readers may recall, we last discussed this fund in early August. The fund has delivered a respectable performance since that time, as investors have received a 1.42% total return compared to a loss in the S&P 500 Index (SP500):

Seeking Alpha

That is not exactly surprising when we consider the assets that this fund invests in. As I pointed out in the previous article, this fund should perform much better than many other things during a period of rising interest rates. As everyone reading this is no doubt well aware, interest rates have been rising over the past two months as investors begin to accept that the fight against inflation is far from over and it is very unlikely that the Federal Reserve will pivot and significantly reduce interest rates anytime soon. With that said though, the ten-year U.S. Treasury (US10Y) is still priced as though rates will be lower within the next two years than they are right now. Fortunately, this fund can perform fairly well in any rate environment.

About The Fund

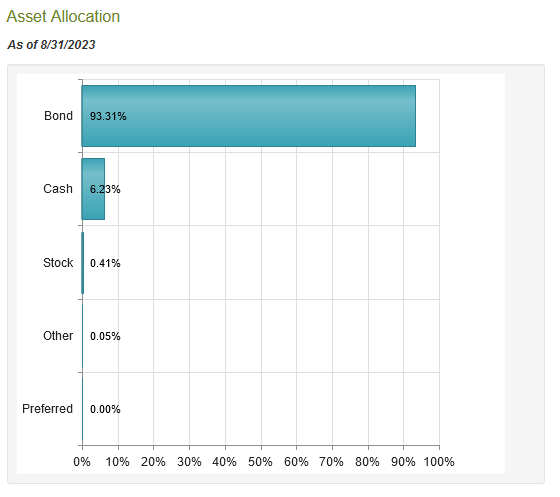

According to the fund’s webpage, the Eaton Vance Floating Rate Income Trust has the primary objective of providing its investors with a high level of current income. This is not particularly surprising considering that this fund primarily invests in debt securities. As we can see here, 93.31% of the fund’s portfolio is invested in bonds alongside a relatively large position to cash:

CEF Connect

It is very rare to see a closed-end fund carry such a large amount of cash. After all, these funds are not like open-ended mutual funds. A closed-end fund does not need to be ready to meet investor redemptions at any given time. After all, investors in these funds can easily convert their shares to cash at a moment’s notice by selling them on a stock exchange. In most cases, carrying a large cash position is a drag on performance, so there is no reason to carry more than is needed to fund opportunistic buying and possibly pay the distribution. As such, most funds have a cash position that is less than 2% or so of assets.

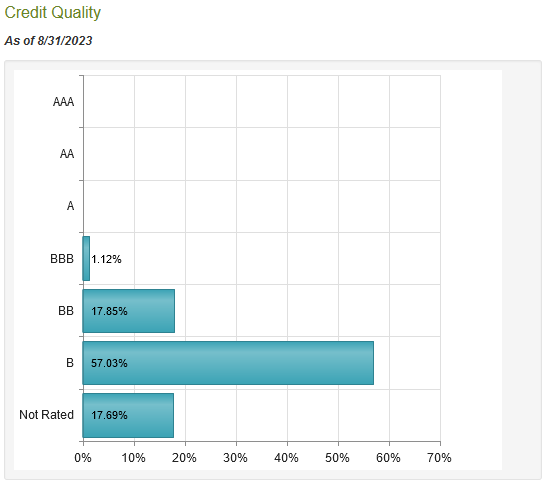

In this case, though, the fund’s cash position actually makes sense. This is because the securities that the fund invests in are debt securities that actually benefit from rising interest rates. That description would apply to a money market fund just as well as it applies to floating-rate debt securities. In fact, because the yield curve has been inverted for a while now, it may actually result in a higher level of income to purchase short-term cash-equivalent securities than long-dated securities, depending on what the fund is buying. That statement is more applicable for Treasury and investment-grade securities than for speculative-grade securities, for example. This fund is investing primarily in speculative-grade debt securities, as we can see here:

CEF Connect

An investment-grade security is anything rated BBB or higher. As we can clearly see, that only describes 1.12% of the fund’s total assets. The remainder is invested in junk-rated debt. That is something that may be concerning to those investors who are concerned about overall risk. After all, junk-rated debt has a much higher default risk than investment-grade securities. As such, the risk of losses due to defaults is much greater here than it would be with a more conventional investment-grade bond fund. The fact that the fund’s largest position only accounts for 1.27% of its assets helps to offset this risk somewhat though, as does the fact that this fund has 505 total current holdings. Thus, the proportion of the fund that is allocated to any given issuer is quite low. If any issuer were to default, it would not have a noticeable impact on the fund as a whole. We probably do not need to worry about default risk here.

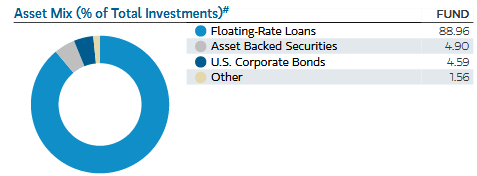

We also do not need to worry about interest-rate risk very much, either. This is because the Eaton Vance Floating Rate Income Trust invests primarily in floating-rate debt securities. In fact, the fund’s fact sheet states that 88.96% of its assets are invested in these securities:

Fund Fact Sheet

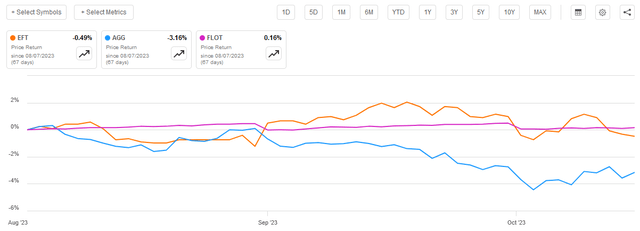

This is important because these securities do not have the same problem that traditional bonds have during periods of rising interest rates. As everyone reading this is no doubt well aware, bond prices decline when interest rates rise. This is why the Bloomberg U.S. Aggregate Bond Index (AGG) is down 3.16% since the last time that we discussed this fund. The same does not apply to floating-rate loans. As we can see here, the Bloomberg U.S. Floating Rate Note Index (FLOT) has been almost perfectly flat since August 7 (the date that my last article on this fund was published):

Seeking Alpha

I explained the reason why bond prices correlate inversely to interest rates in my last article on this fund:

“The reason why bond prices decline when interest rates go up is that newly-issued bonds will have an interest rate that corresponds to the market interest rate at the time of issuance. As such, a bond that is issued today will have a coupon rate that is much higher than that of a bond that was issued back in 2021. As such, it makes no sense for anyone to purchase an existing bond when they could buy an otherwise identical one that has a much higher rate. The price of the existing bond thus needs to decline until it delivers a yield-to-maturity that is comparable to an otherwise identical brand-new bond.”

That does not apply to floating-rate bonds, however. The bonds in which this fund is invested have coupon rates that change based on some interest rate benchmark, such as LIBOR. As such, they will always deliver a competitive yield to otherwise identical brand-new securities. This tends to result in very stable prices over time. We can see evidence of this in the fact that the Bloomberg U.S. Floating-Rate Note Index has been almost perfectly flat over the past ten years:

Seeking Alpha

The only exception to this stability was a very brief point during the Spring of 2020 when the COVID-19 pandemic fears were at their maximum level and investors were generally selling off everything in order to move into safe assets such as cash. As such, we should expect that the Eaton Vance Floating Rate Income Trust should be pretty stable in terms of price regardless of what interest rates do. Unfortunately, that has not been the case over the past decade:

Seeking Alpha

As we can see here, shares of the fund declined by 22.79% over the period, despite being invested in assets that are reasonably stable. This is partly due to this fund’s use of leverage, which we will discuss in just a moment.

Fortunately, things get much better when we consider the fact that the Eaton Vance Floating Rate Income Trust boasts a much higher yield than the floating-rate bond index. The distributions paid by the fund naturally offset some of the price declines. In fact, over the period, investors in this fund ended up earning a 50.60% total return over the past ten years. This was a substantial improvement over both the floating-rate index and the Bloomberg U.S. Aggregate Bond Index:

Seeking Alpha

This should cause this fund to have a certain amount of appeal to any income-focused investor. After all, much of this period was dominated by extremely low interest rates, but this fund still managed to perform reasonably well. However, it does tend to do much better during periods of rising interest rates. That makes sense since the coupon payments that the fund receives from its assets increase during such an environment.

One of the big questions right now for debt investors is what direction interest rates will take from here. In a few recent articles, I suggested that the United States may be on the verge of descending into a recession. This is a view shared by a majority of American consumers as well as most corporate Chief Executive Officers, at least based on recent economic surveys. A few retailers have even publicly stated that consumer spending is beginning to slow down, which furthers this narrative. The yield curve is currently inverted (at least between two-year and ten-year Treasuries), which likewise suggests a recession in the near future. The market is expecting that the Federal Reserve will pivot and cut rates when that happens, but this may not happen this time due to inflationary pressures from rising crude oil prices and the incredible increase in the money supply that occurred during the pandemic. A rate cut will almost certainly reignite inflation, even if the economy is in a recession.

Even if the Federal Reserve were to cut the federal funds rate, there is no guarantee that this would reduce interest rates. In a recent article, I pointed out that the Federal Government’s borrowing activity has crowded out the private sector. As foreign buyers and even domestic banks have begun to reduce their buying activity in the Treasury market, the only buyer left is the U.S. consumer. When we consider the pressure that consumer budgets are under right now, they might not step up to the plate to nearly the degree that is needed. That will drive up interest rates as the few buyers available demand ever higher interest rates to continue to finance the government. If the Federal Reserve tries to prevent this by buying Treasuries itself, inflation will take off.

Thus, it would be a good idea to have something in your portfolio that will react positively to high or rising interest rates. The Eaton Vance Floating Rate Income Trust may be one way to obtain that exposure.

Leverage

Earlier in this article, I mentioned that the Eaton Vance Floating Rate Income Trust employs leverage as a method of boosting its effective portfolio yield. This is a strategy that most closed-end funds use to one degree or another. I explained how this works in my last article on this fund:

In short, the fund borrows money and then uses that borrowed money to purchase floating-rate debt securities. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, so this will usually be the case. Unfortunately, this strategy is not as effective at boosting yields today as it once was. This is because the difference between the yield of the purchased securities and the interest rate of the borrowed money is a lot less than it was back when interest rates were at 0%.

The use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund does not employ too much leverage since this would expose us to an excessive amount of risk. I generally do not like to see a fund’s leverage exceed a third as a percentage of its assets for this reason.

As of the time of writing, the Eaton Vance Floating Rate Income Trust has levered assets comprising 34.09% of its assets. This is the same as the last time that we looked at the fund. That is not especially surprising since the fund’s net asset value has actually been perfectly flat since August 7, 2023:

Seeking Alpha

As was the case before, the fund is a bit above the one-third cutoff that we usually like, but it is probably okay. One reason for this is that the fund’s leverage is barely above that one-third level. A second reason is that its assets are not especially volatile, so it should be able to carry substantially more leverage than an ordinary equity closed-end fund. As such, we probably do not need to worry too much about the fund’s leverage right now. It appears that everything is probably okay here.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Eaton Vance Floating Rate Income Trust is to provide its investors with a high level of current income. The fund accomplishes this by purchasing floating-rate speculative-grade securities. These securities tend to have very high yields, with the average coupon yield being 9.03% right now. The fund collects the payments from these securities and applies a layer of leverage to boost the yield well above this figure. It then pays out the money that it generates from its portfolio, minus any expenses that are billable to the fund. This can be expected to give the fund a very high yield.

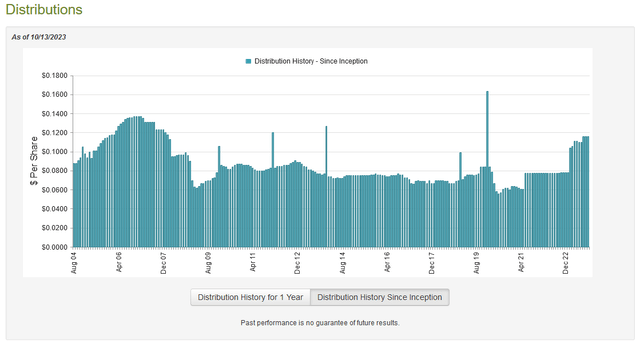

This is certainly the case, as the Eaton Vance Floating Rate Income Trust pays a monthly distribution of $0.1160 per share ($1.3920 per share annually), which gives it an 11.48% yield at the current price. That is certainly comparable to any other high-yielding debt fund right now. Unfortunately, the fund has not been especially consistent with respect to its distribution over the years. In fact, it has varied it numerous times. We can see this here:

CEF Connect

This extreme variation over time is likely to reduce the fund’s appeal somewhat to those investors who are looking for a source of consistent income that they can depend on for bill payments. However, it is very typical for a fund like this to change its distribution over time. After all, the income provided by floating-rate securities tends to vary with interest rates and the securities themselves tend to be so stable that the fund cannot really make a lot of money exploiting changes in prices. Indeed, this fund only has a 16.00% annual turnover, so it is not trying to make money trying to trade securities.

As is always the case, we want to examine the fund’s finances to determine how well it is covering its distribution. After all, we do not want the fund to be paying out too much money and unnecessarily depleting its assets. That is not sustainable over any sort of extended period.

Fortunately, we have a fairly recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the full-year period that ended on May 31, 2023. This was a rather interesting period because it includes both the impact of rising rates during the second half of last year as well as the optimism surrounding the potential for a near-term pivot during the first half of this year. However, as we have already seen, most of the securities held by this fund are not really going to be affected by the market’s feelings about future interest rates.

During the full-year period, the Eaton Vance Floating Rate Income Trust received $1,072,827 in dividends and $48,224,702 in interest from the assets in its portfolio. This gave the fund a total investment income of $49,297,529 during the period. It paid its expenses out of this amount, which left it with $33,572,147 available for shareholders. This was more than enough to cover the $30,661,298 that the fund paid out in distributions over the period. Thus, this fund is simply paying out its net investment income to its shareholders.

That should prove to be sustainable indefinitely, although the fund did realize $7,368,012 in losses during the period. That is quite disappointing and over the long term, it could result in the fund’s assets being depleted, but there will almost certainly be years in which the fund manages to earn a net realized gain. For the most part, its current distribution should be sustainable as long as interest rates do not decline significantly.

Valuation

As of October 13, 2023 (the most recent date for which data is currently available), the Eaton Vance Floating Rate Income Trust has a net asset value of $13.16 per share but the shares currently trade for $12.08 each. This gives the fund’s shares an 8.21% discount on net asset value. That is quite a bit better than the 6.74% discount that the shares have had on average over the past month. Thus, the current price looks like a reasonable entry point for anyone who wants this fund today.

Conclusion

In conclusion, the Eaton Vance Floating Rate Income Trust is a good way for investors to obtain both a high level of income and still have some protection against interest rate risk. The assets in this fund should prove to be much more stable than what is held by a typical bond fund, and they boast very high yields in the current interest rate environment. When we consider that the actual trajectory of interest rates from here is rather uncertain, it may be good to have this protection. The fact that the fund is easily covering its distribution solely out of net investment income and is trading at a discount is the icing on the cake. Overall, this fund is worth considering for your portfolio today.

Read the full article here