Introduction

On July 31, I wrote an article titled General Mills: A Dividend Diamond In The Rough. In that article, I wrote that the company’s yield is somewhat stuck between dividend growth and high yield, making it less appealing to a lot of investors.

I also noted that General Mills (NYSE:GIS) was working on improving its business to gain pricing power.

General Mills presents a mix of headwinds and tailwinds for investors to consider. While the company has made progress in improving its business, its inconsistent performance has hindered its total return compared to peers and the market.

The 3.1% dividend yield falls between a growth stock and a high-yield stock, making it a challenging choice for portfolios.

However, there are positives to note, such as the recent dividend hike and the company’s focus on brand updates and innovation.

Despite inflation challenges, General Mills is generating significant free cash flow, leading to potential dividend growth and share buybacks.

While the company’s valuation appears attractive, it might be wise to wait for a better entry point, considering the current inflationary headwinds.

Especially in this environment, pricing power is key, as the market is punishing entire sectors that are expected to suffer from what could be a prolonged period of weakening economic demand and sticky inflation.

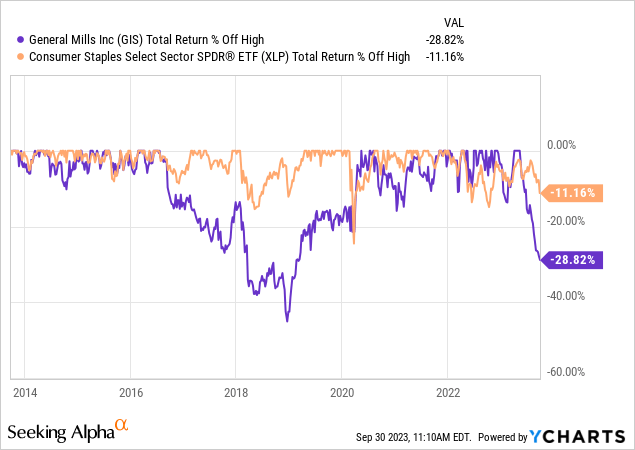

In light of what I wrote in my prior article, the stock continued to fall, dropping as much as 30% from its all-time high.

Including dividends, the stock is 29% below its high, making this the second-worst sell-off since 2013.

Now, I’m revising the stock after it has revealed its 1Q24 earnings and updated us on new developments during conferences.

So, let’s dive in!

How Bad Is It?

On September 20, General Mills revealed the first-quarter earnings of its 2024 fiscal year.

The company started its earnings call by highlighting its focus on navigating the evolving external environment, characterized by moderating inflation, stabilized supply chains, and a cautious yet resilient consumer.

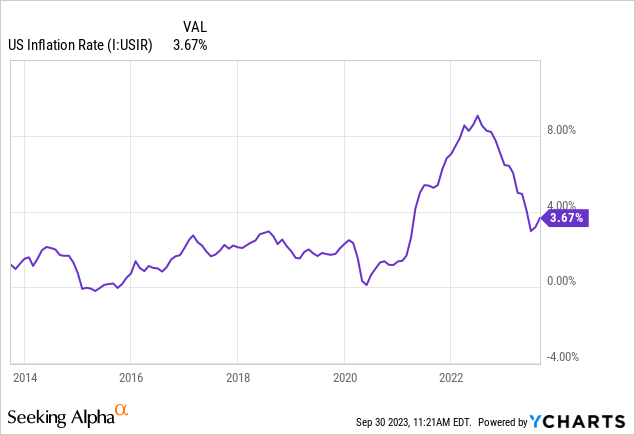

One of the reasons why GIS and its peers (it’s not alone when it comes to declining stock prices) are selling off is that the market is telling us it doesn’t believe that inflation is easing. It disagrees with what a lot of companies are expecting.

For example, inflation is rebounding before getting close to the Fed’s target.

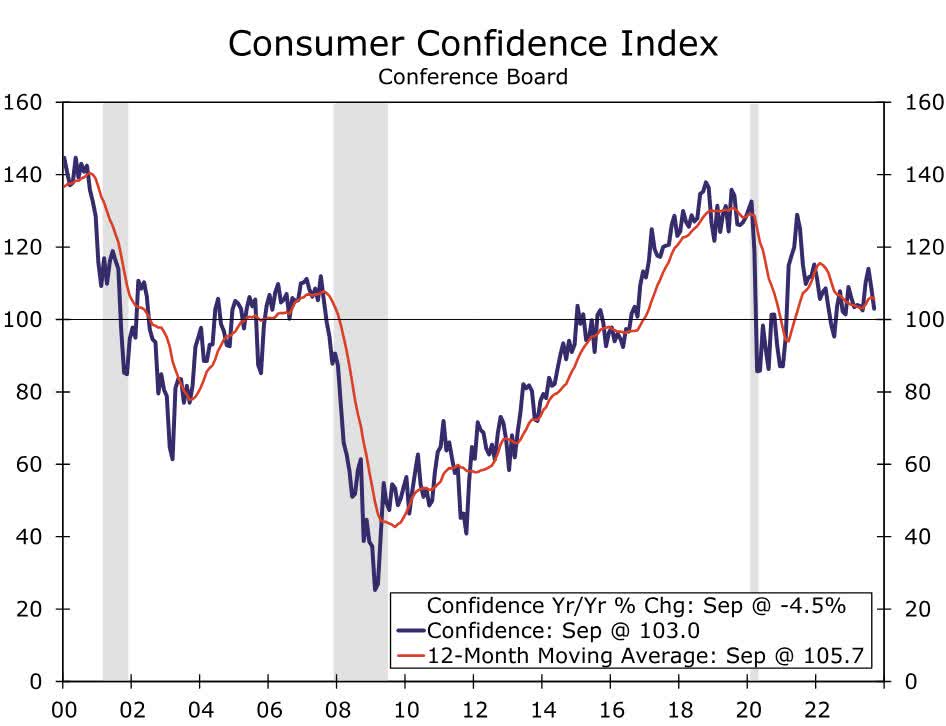

Consumer confidence is also declining again.

Wells Fargo

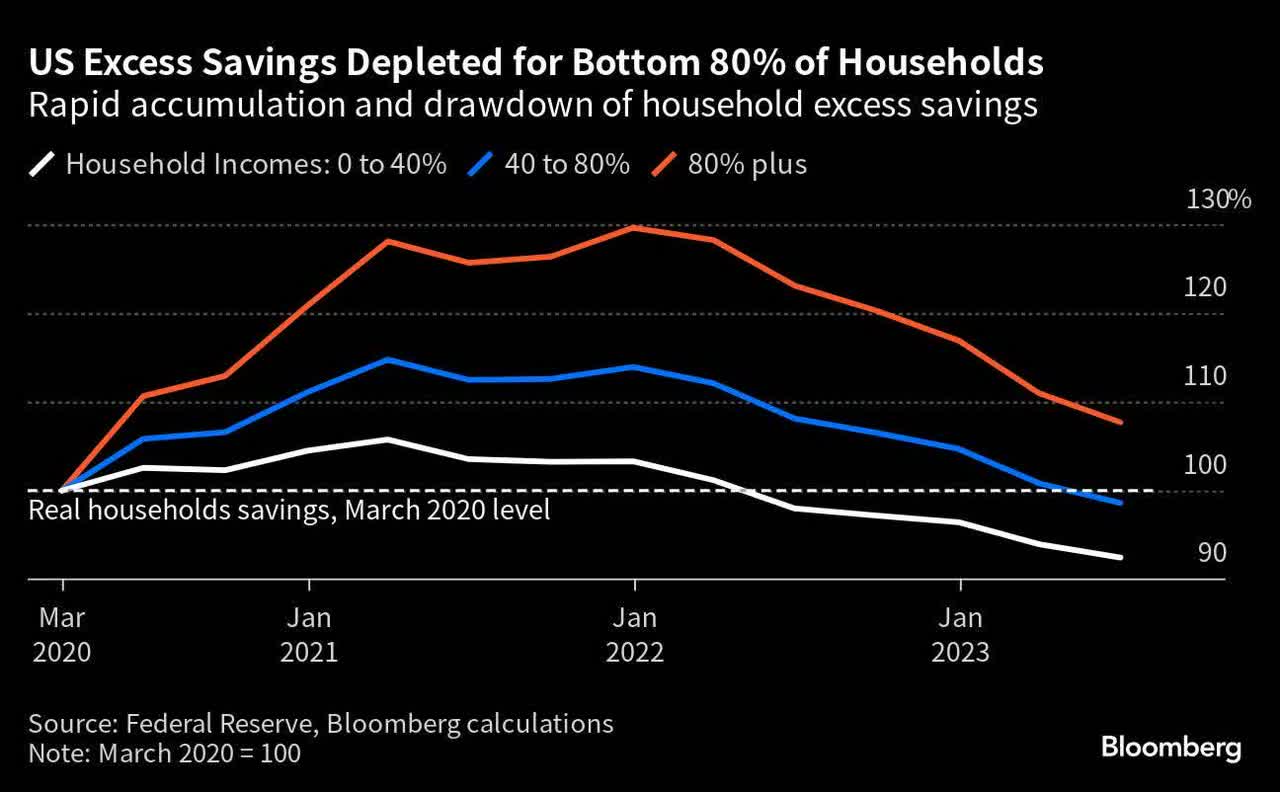

The worst part is that the decline in consumer confidence is now having a bigger impact on the economy because consumers are out of savings. Well, at least the bottom 80%, according to the chart below.

Bloomberg

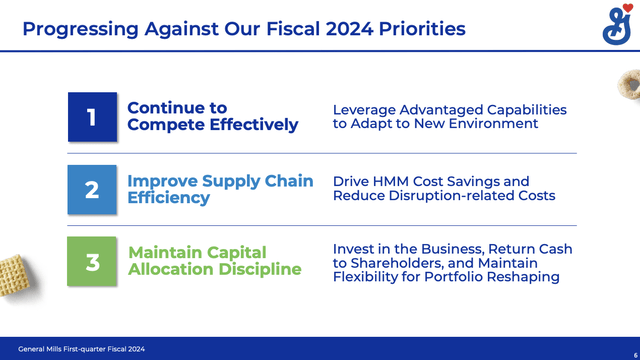

Going back to the 1Q24 call, General Mills also reiterated the three key fiscal 2024 priorities: effective competition through brand building and innovation, supply chain efficiency improvement, and disciplined capital allocation.

These measures are important, as growth is sluggish.

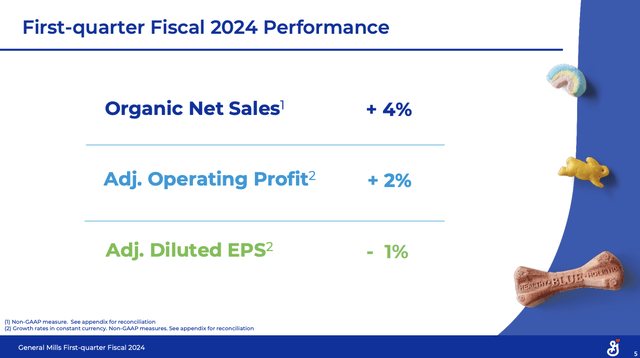

In the first quarter, General Mills achieved a 4% organic net sales growth rate, propelled by carry-over net price realization resulting from Strategic Revenue Management (“SRM”) actions taken in response to significant input cost inflation during fiscal year 2023.

General Mills

However, the adjusted diluted earnings per share experienced a decline of 1%.

Having that said, let’s take a closer look at its results.

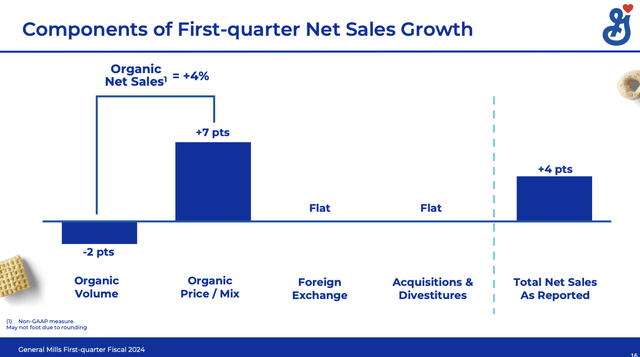

The positive net sales growth was mainly driven by a favorable price/mix scenario, albeit somewhat mitigated by a reduction in pound volume, which is quite common in these challenging times, as consumers are reducing spending and/or switching to generic brands.

General Mills

When it comes to the segment performance, we also see a few interesting developments.

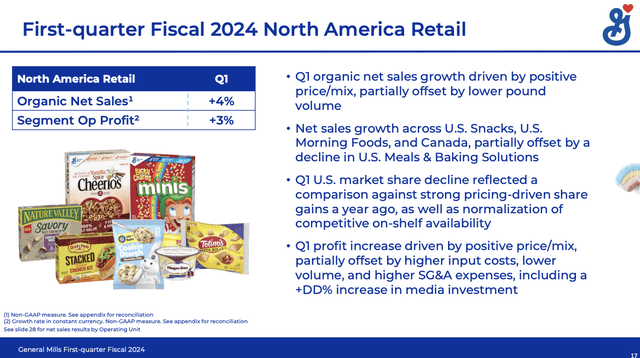

- The North American retail segment witnessed a 4% organic net sales growth, supported by a positive price/mix. Unfortunately, this was moderated by a reduction in pound volume. The operating units within North America Retail displayed distinct growth patterns, with U.S. Snacks leading at an 8% increase in net sales, followed by U.S. Morning Foods at 3%, and Canada at 4% in constant currency. However, U.S. Meals & Baking Solutions experienced a 1% decline, a result of the Helper and Suddenly Salad divestiture.

General Mills

Furthermore, the market share in the U.S. dropped during Q1. This was attributed to a challenging comparison to the previous year’s exceptional share gains.

The anticipation is that this market share will gradually improve as the year progresses and the comparisons become less challenging. If that doesn’t happen, I think we can make the case that generic products are becoming too competitive. For now, we cannot make that case.

The food service segment did a bit better.

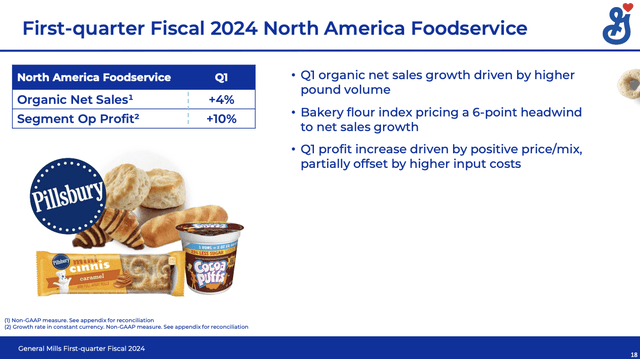

- The North American Foodservice segment displayed a 4% organic net sales growth, which was attributed to an increase in pound volume. This was noteworthy considering a 6-point headwind from market index pricing on bakery flour. Consumer traffic in hospitality, travel, education, and other non-restaurant away-from-home food channels increased during Q1, compensating for relatively stable restaurant traffic levels compared to the previous year.

General Mills

- The Pet segment saw a plateau in organic net sales. This stagnation was due to short-term consumer challenges in the premium pet food segment.

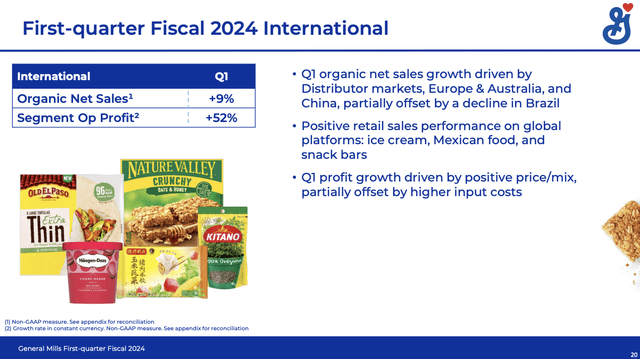

- The International segment recorded strong retail sales growth in key platforms such as ice cream, Mexican food, and snack bars.

General Mills

Having said that, let’s take a look at the company’s guidance and growth measures.

Improving Growth And Operations & Looking Ahead

One thing we discussed in my prior article is business improvements. These continued.

Allow me to quote the company (emphasis added):

At the start of the year, we outlined three priorities for fiscal 2024, as we continue to execute on our Accelerate strategy and drive shareholder value.

First, we’ll continue to compete effectively by leveraging remarkable brand building, innovation, and advantaged capabilities to win with a changing consumer.

Second, we’ll improve our supply chain efficiency, with a focus on increasing Holistic Margin Management [HHM] cost savings and reducing costs related to supply chain disruptions.

And third, we’ll maintain our disciplined approach to capital allocation by investing in the business, delivering strong cash returns to shareholders, and maintaining our balance sheet flexibility for portfolio reshaping.

General Mills

Earlier in September (before the 1Q24 release), the company also commented on growth progress during the Barclays Global Consumer Staples Conference.

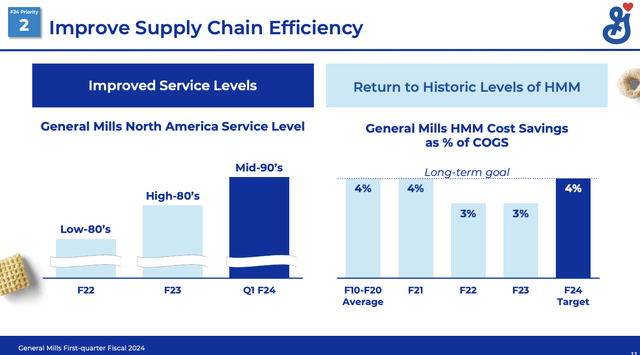

During this conference, the company highlighted the continuous improvement in its supply chain service levels, ranging from a low 90% to a mid-90 percentage point range for the year. The stable supply chain environment supports GIS’s expectation of achieving normalized levels of HMM cost productivity, historically at 4% or greater.

General Mills

The company also acknowledged consumer value-seeking behaviors and inventory corrections in its North American retail business. It also addressed shifts in pet parent behaviors within the Pet segment. These issues are pressuring the company to effectively rebuild its brands.

Having said that, GIS has confidence in its long-term growth prospects, driven by a focus on effective competition, supply chain efficiency, and disciplined capital allocation.

During the conference, the company cited a significant organizational reformation to enhance operational efficiency and agility, setting the stage for mid-term organic growth targets in the range of 2% to 3%, which is very ambitious.

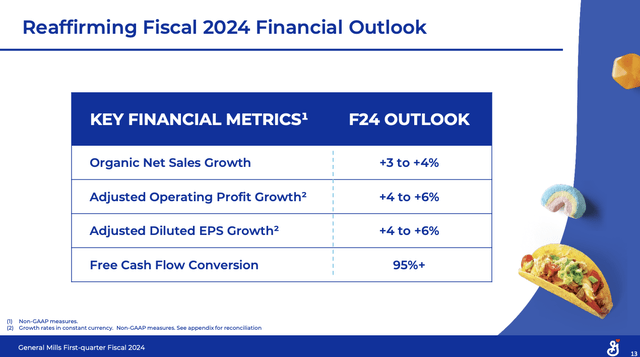

On a shorter-term basis, the company reiterated its full-year outlook during the 1Q24 earnings call.

It anticipates organic net sales growth of 3-4%, a 4-6% constant-currency growth in adjusted operating profit and adjusted diluted earnings per share, and a commitment to achieving a free cash flow conversion of at least 95% of adjusted after-tax earnings.

General Mills

These guidance numbers are good. The only problem is that the market isn’t eager to believe these numbers, as the risk of downside adjustments is growing rapidly (in light of economic developments).

Dividend & Valuation

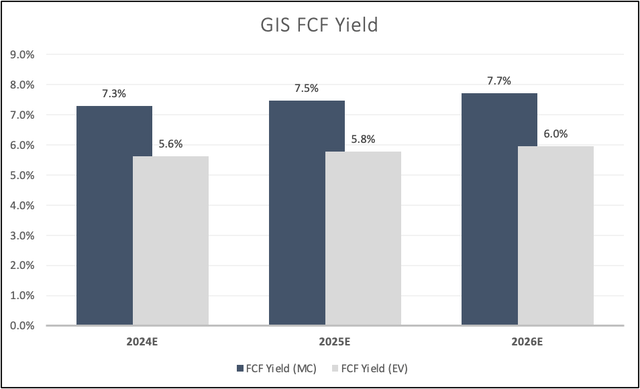

GIS pays a 3.7% dividend, which is backed by a lot of free cash flow.

Looking at the chart below, the company is expected to generate a 7.3% free cash flow yield this year, which suggests a 50% cash dividend payout ratio.

It is also backed by a healthy balance sheet. The company has a 2.5x 2024E net debt leverage ratio and a BBB credit rating.

Leo Nelissen (Based on analyst estimates)

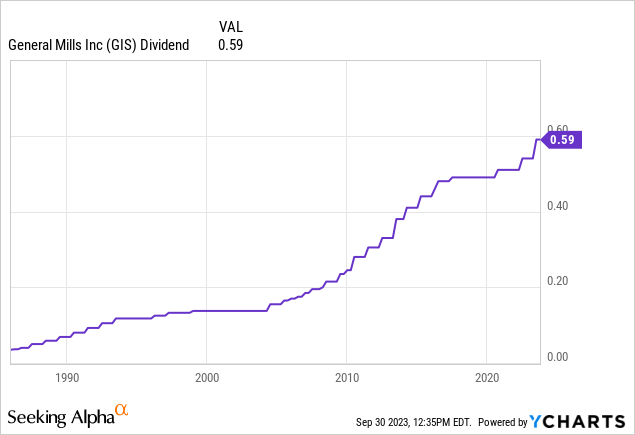

On June 28, the company hiked its dividend by 9.3%, which is remarkable, as the 10-year average annual dividend growth rate is just 4.9%.

This is clearly a sign that GIS believes in its turnaround strategy. It also benefits from a healthy balance sheet and plenty of free cash flow, so hiking by 9% wasn’t a huge risk.

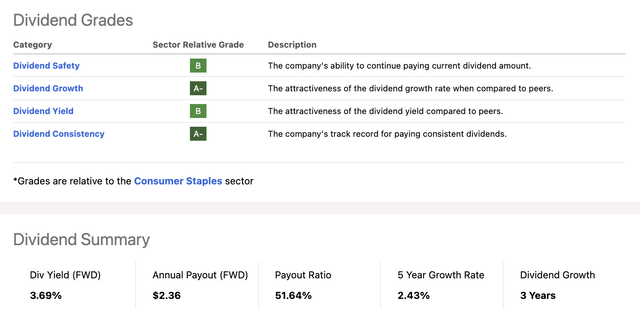

As a result, the company has a very favorable Seeking Alpha dividend scorecard, which shows that it is scoring high on key categories relative to the consumer staples sector.

Seeking Alpha

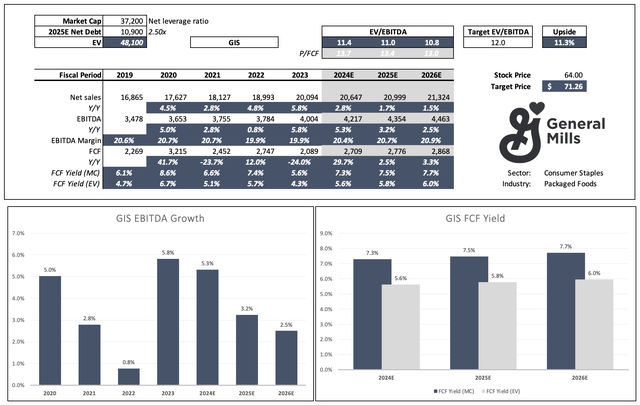

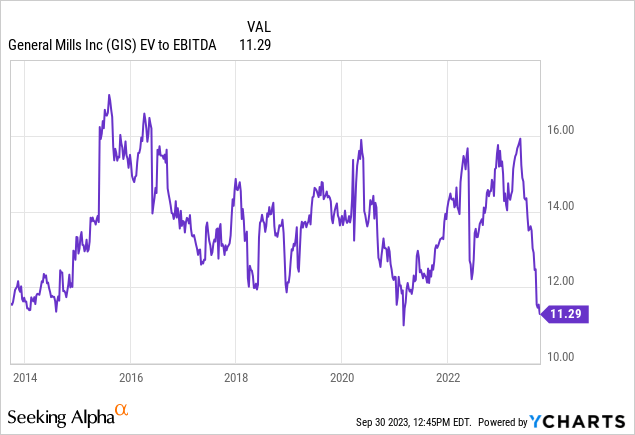

With regard to the valuation, GIS is trading at 11.4x 2024E EBITDA. That number drops to 10.8x using 2026E data. This is based on expected low-single-digit annual EBITDA growth in both the 2025 and 2026 fiscal years.

Leo Nelissen (Based on analyst estimates)

Having said that, the company’s valuation over the past ten years has been in a very wide 11x to 17x EBITDA range. In my model above, I’m giving the stock a 12x multiple. Expected EBITDA growth over the next few years is subdued, while macroeconomic risks remain elevated.

This would give the stock a fair price target of $71, which is 11% above the current price.

The current consensus price target is $74.

With all of this in mind, I believe that the sell-off isn’t an overreaction. Investors are fearful of sticky inflation, and rightfully so. Even the best stocks in this sector, like PepsiCo (PEP), are selling off.

While the challenging environment poses risks to GIS’ recovery measures, the stock is far from dead money. The yield has risen to 3.7%, dividend growth is up, and financials support long-term dividend growth.

The problem is that we won’t see a lot of upside until investors are willing to bet on a sustainable decline in inflation. Until that happens, I recommend investors interested in GIS accumulate shares on weakness. Do not take a large position at once, but buy in intervals.

I give the stock a Buy rating at these levels, although my rating does not come with a lot of conviction.

Takeaway

General Mills presents a complex investment scenario. The stock has faced a significant sell-off, driven by concerns over persistent inflation and declining consumer confidence. While the company’s 1Q24 results showed promise in terms of net sales growth, there are challenges, particularly in market share and the competitive landscape.

General Mills is actively working on business improvements, with a focus on brand building, supply chain efficiency, and disciplined capital allocation. The company’s dividend hike and strong free cash flow are positive signs for income investors. However, the market remains cautious, given economic uncertainties.

In this environment, patience is key. Despite the uncertainty, GIS offers a compelling 3.7% dividend yield and a favorable balance sheet. While there may not be an immediate upside, the stock is far from a lost cause.

Accumulating shares gradually on weakness seems prudent. I cautiously rate General Mills as a Buy, although I’m not excited enough to put it on my watchlist.

Read the full article here