Co-authored with “Hidden Opportunities.”

As I research and write about dividend payers, including common, preferred stock, and baby bonds, I come across a common sentiment – the best time to buy was October 2022 or March 2023. Often someone will tell me they are “waiting” for the prices to pull back to those levels.

The recency bias will always be there until the sentiment transforms to regret – “if only I bought XYZ in March 2020 …. “.

“If “ifs” and “buts” were candy and nuts, wouldn’t it be a Merry Christmas?” – Don Meredith, Football Commentator.

Billionaire hedge fund manager Ken Fisher has been bullish on the markets since the beginning of 2023, saying inflation is in the past and it is time for equities to rebound strongly.

“Inflation is deader than a doornail – markets just don’t know it yet.” – Ken Fisher in January 2023.

Mr. Fisher now says Wall Street is seeing an early bull market despite broader skepticism.

“No one knows exactly when a new bull market will start, it’s common to see pervasive investor skepticism during the bulls’ initial climb. Current economic conditions are better than most people believe and, therefore, we’re likely to see positive economic surprises on a regular basis as 2023 progresses—a feature that could lift global stocks but likely requires investors to remain patient a bit longer.” – Ken Fisher.

It isn’t too late to pick up big dividends at discounted prices. I am preparing for the new bull market by setting up a millionaire’s cash flow. Here are two picks I’m buying.

Pick #1: AWP – Yield 12.7%

Real Estate Investment Trusts (“REITs”) are an omnipresent yet ignored market segment. Places you visit while running errands or on vacation, your place of work, and several other physical locations are most likely tenants of one or more REITs. Even without leaving your house, you may be accessing several popular services like Netflix (NFLX) and Spotify (SPOT), which have the bulk of their cloud infrastructure setup in large-scale data centers which are managed by, you guessed it right, REITs. Source.

Dgtlinfra Website

Today’s public REITs have much more manageable debt levels than during the Great Financial Crisis. REITs, on average, have debt at 34% of assets (down from 65% during the financial crisis). Thanks to the near-zero rates in 2020-2021, about three-quarters of that debt is unsecured bonds or bank loans, making them essentially free of mortgage obligations. Almost 90% of REIT debt is fixed-rate, maturing in an average of seven years, which provides adequate legroom for them to wait for a more favorable interest cycle to refinance.

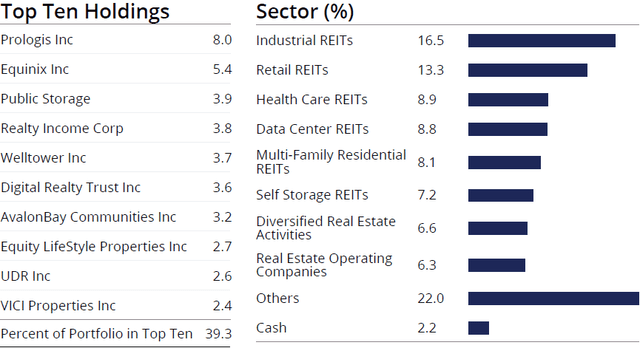

abrdn Global Premier Properties Fund (AWP) is a Closed-End Fund (“CEF”) diversified across 75 global REITs with almost ~50% allocation to industrial, retail, healthcare, and data center REITs. These highly location-dependent sectors tend to maintain their presence in the selected neighborhood for a very long time, ensuring reliable rent payments and steady occupancy levels for the landlords. Source.

AWP Jun 2023 Performance Data and Portfolio Composition

AWP’s top holdings are some of the most robust REITs with a higher allocation to companies with a solid track record of dividend growth over past decades. The CEF pays $0.04/share monthly, a solid 12.7% yield at current price levels. YTD 2023, AWP has paid nine monthly distributions, broken down as 73% Return of Capital (“ROC”), 1% Short-Term gains, and 26% Net Investment Income (“NII”).

For 1H 2023, the fund reported $5.8 million in NII and $34 million in unrealized investment appreciation. This indicates healthy coverage for the $20 million distribution for the period, with adequate room for the remainder of the year.

AWP is modestly leveraged at 20%, and the fund carries a 1.4% expense ratio, including a 0.21% interest expense. As shareholders, our $100 works as though it were $120 (with the leverage), and we get access to this leverage through a 21-cent interest expense. With traditional brokerage margin rates oscillating between 10-15% depending on the borrowing size, AWP’s interest expense is a bargain to boost allocations to this undervalued sector.

AWP trades at an 8% discount to NAV, making it an excellent time to buy/add to your holdings. This REIT CEF was introduced to our portfolio during the darkest of times in late March 2020. We have been through fear, negativity, and pessimism over the retail and travel industry then, and we will get through similar emotions towards commercial REITs (specifically office properties) now. Until then, we sit back and collect our monthly dividends. What are your plans this weekend? I bet there are some REIT services you will be utilizing.

Pick #2: GMRE Preferred – Yield 7.4%

If you seek exposure to real estate but are worried about digital disruption and the growing adoption of remote work, medical REITs are the best investments for you. These provide adequate protection from e-commerce disruption.

They also provide much-needed inflation protection, as many medical leases have structured rental escalations throughout the term of the lease. Medical practitioners like dentists, physiotherapists, etc., strategically establish their practice in a neighborhood and build their reputation in the community for years. As such, location is extremely important for their business, giving rise to long-term lease agreements.

Due to the stability and credit quality of the tenant base, and the essential nature of the services they provide, medical offices saw growing adoption through the pandemic.

The medical office sector typically has long-term tenants, presenting safe, inflation and recession-resistant assets for investors.

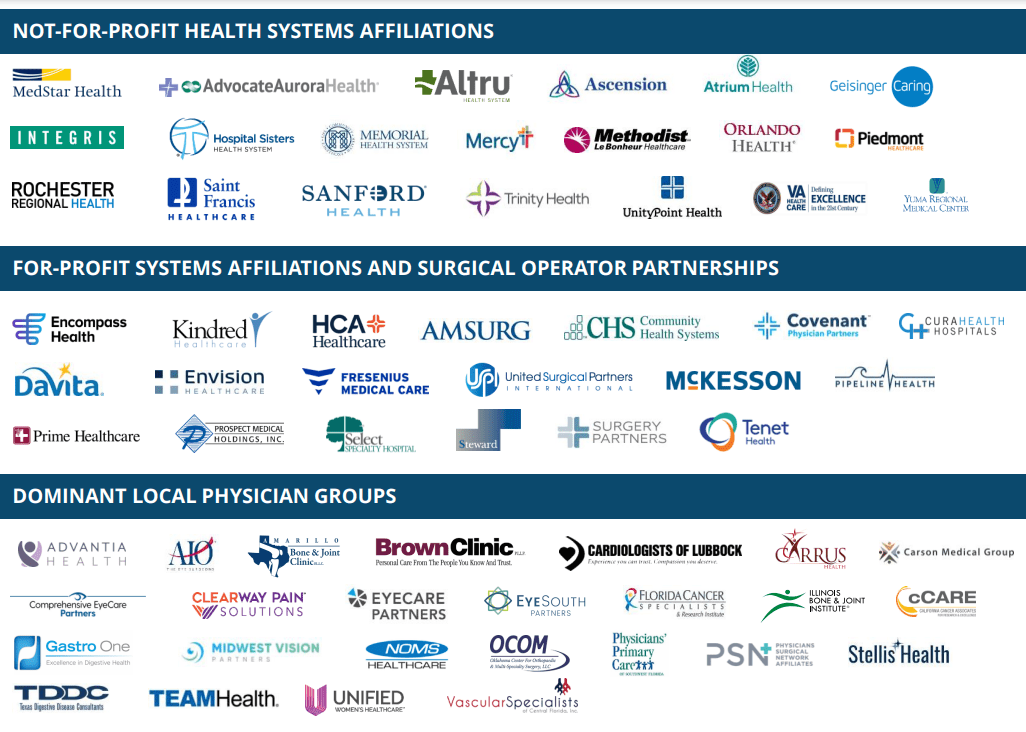

Global Medical REIT Inc. (GMRE) is a triple net lease REIT that operates a portfolio of 188 buildings and serves as the landlord for 274 tenants in the healthcare industry. The company ended Q2 with a portfolio occupancy of 97% and a weighted average lease term of 5.8 years. The REIT’s tenant base comprises some of the top physician groups and healthcare providers across the country, providing treatment and care for a wide range of health requirements. Source.

June 2023 Investor Presentation

As hospitals were grappling with treating more serious illnesses that may have gone overlooked during the initial months of the pandemic, the demand for ambulatory and outpatient services rose, allowing GMRE to utilize the industry tailwinds and reward shareholders with dividend raises.

GMRE paid down its variable rate debt, resulting in a leverage ratio at the end of Q2 of 44.5% and reducing its mix of variable rate debt to 12% of the total indebtedness. 88% of GMRE’s debt is fixed at a 3.75% rate with a weighted-average term of 3.7 years, enough to ride out this rate cycle and refinance favorably.

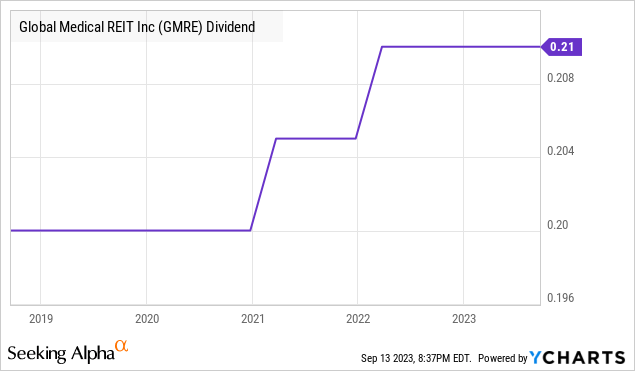

With almost ~96% of its debt due in 2026, the REIT remains in a comfortable liquidity position in the current interest rate cycle. The GMRE-A preferred shares present a safer opportunity for investors seeking steady, well-covered income for the foreseeable future. This preferred offers a 7.4% yield until redemption, which is unlikely to happen soon in this interest-rate environment.

-

Global Medical REIT, 7.50% Series A Cumulative Redeemable Perpetual Preferred Stock (GMRE.PR.A).

During 1H 2023, GMRE spent $16.7 million on interest expenses and $2.9 million towards the preferred dividend, which were adequately covered by the REIT’s $33.6 million in net cash from operating activities. A growing common dividend is a boon for the investors of GMRE’s cumulative preferreds.

Medical Office Buildings offer the dual benefits of convenience to patients and medical practitioners and will see growing adoption in the years ahead. Investors can lock in a 7.4% yield from this high-quality medical REIT that caters to a recession-resistant tenant base.

Conclusion

The best part of being an income investor is the luxury of not caring to find the bear market bottom or worrying about market corrections. Dividends are powerful yet highly misunderstood and underutilized, as investors are generally impatient and aim for the fences with speculative plays.

Let’s examine the power of dividends with an example. A $10,000 investment in Altria Group, Inc. (MO) made ten years ago, assuming no reinvestment, would have paid you $9,432 in dividends to date, and you would be sitting on an equity position worth $14,447. Most importantly, you will have the same number of shares as you did ten years ago. Source.

Portfolio Visualizer

These ten years have been challenging for the big tobacco firm. There have been tight regulations, pricey acquisitions that became bitter disappointments, social stigma, and heavy investments into growth segments. Despite all this, MO delivered its growing dividends like clockwork.

Billionaire Ken Fisher says don’t miss the new bull market by sitting on the sidelines, and I agree with the approach. However, my investment goals differ from those of the hedge fund manager, so I am buying discounted dividend payers to lock in big yields for the foreseeable future.

This article discusses two solid dividends from the REIT camp, poised to make it worth your time (and money). With up to 12% yields, you can collect large paychecks to utilize as you see fit and cruise through the uncertainties and the market noise.

Read the full article here