Introduction

Engaging in the asset management and custody banks industry Diamond Hill Investment Group Inc (NASDAQ:DHIL) has been quite good at growing their client base over the years. Just looking at the total asset growth over the last 10 years it has displayed a 16.35% annual growth rate. This is quite impressive and goes to show that the broad approach that DHIL applies to their business is paying off very well, meaning that they cater to a broad set of customers and clients.

The dividend rate of the business is solid and I think the rise in interest rates is short-lived and should start to go down in late 2024 potentially. This would likely send a bullish signal to the markets and net DHIL and other asset management companies’ strong returns. The company already has an ROE of nearly 30% and I think this alone makes the potential shareholder returns quite appealing. This concludes me rating DHIL a buy right now.

Company Structure

DHIL is an independent investment management firm known for its commitment to delivering exceptional investment advisory and fund administration services to a diverse clientele. With a comprehensive range of offerings spanning equities, fixed income, mutual funds, and corporate credits, DHIL caters to the unique needs and objectives of a broad spectrum of investors.

What sets DHIL apart is its steadfast adherence to a valuation-driven investment approach, characterized by a deliberate focus on long-term perspectives. Unlike some other asset managers that exclusively target high-net-worth individuals, this has over the years been a major benefit to the company as it has helped them drive stronger asset and deposit growth ultimately.

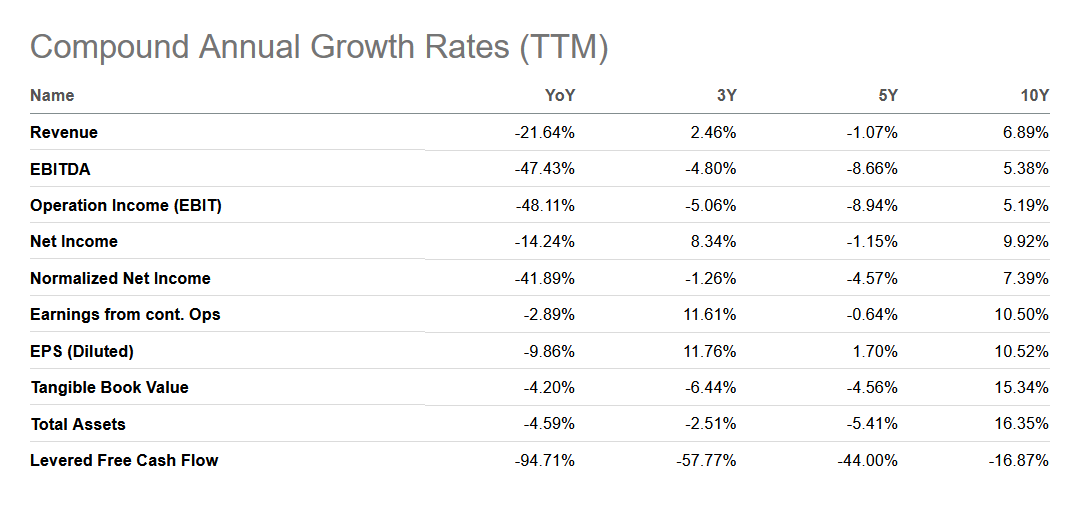

Growth Rates (Seeking Alpha)

Just like the markets can show some bad years now and again, I think it’s important to look at the bigger picture with companies like DHIL for example. When looking at the numbers above I think it is clear that DHIL has been a great performer of the last decade and this has fueled the dividend very well in my opinion. They have managed to very well capitalize on the market conditions and drive EPS growth when interest rates were lower and market momentum high. I think the last 12 months are a bump in the road and not something that will derail the business practices and cause DHIL to post significantly lower results going forward.

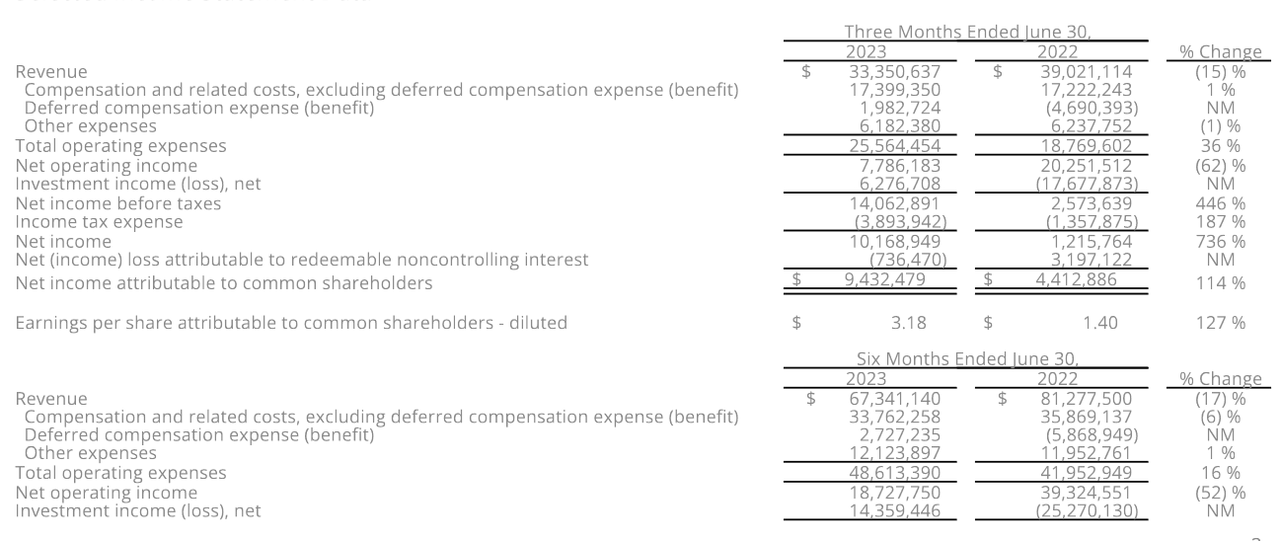

Income Statement (Earnings Report)

Looking at the last report from the company some parts were struggling, but ultimately I think the quarter was very solid and DHIL proved that they can weather market volatility very well. The EPS more than doubled which was thanks to the rising interest rates and the fact that DHIL can charge their clients a higher premium. But this of course also affects the inflows for the business. The AUM saw a decline on a YoY basis, but DHIL still has strong margins with the ROA for example at over 20% right now using the TTM numbers. This just goes to show the efficiency of the business and how well they have set themselves up to deliver strong earnings.

Earnings Transcript

From the last report, the CEO of DHIL Heather Brilliant had the following to share with investors.

-

“While our 2Q revenue and operating margin were impacted by lower average assets under management and advisement during the quarter, strong markets and improved long-term performance helped deliver improvement by quarter end. Our efforts to diversify are showing promise as we continue to see inflows in fixed income, which unfortunately were offset by equity out outflows”.

I think this has been the secret to the success of DHIL over the years, diversifying the business and not being reliant on one source of income for the business. If the next few quarters showcase similar strong resilience in the bottom line and margin retention I think that DHIL could potentially be a strong buy even. The fixed income inflows for the last quarter were $134 million which is a very strong amount and should help mitigate some of the volatility that the markets are exhibiting right now I think.

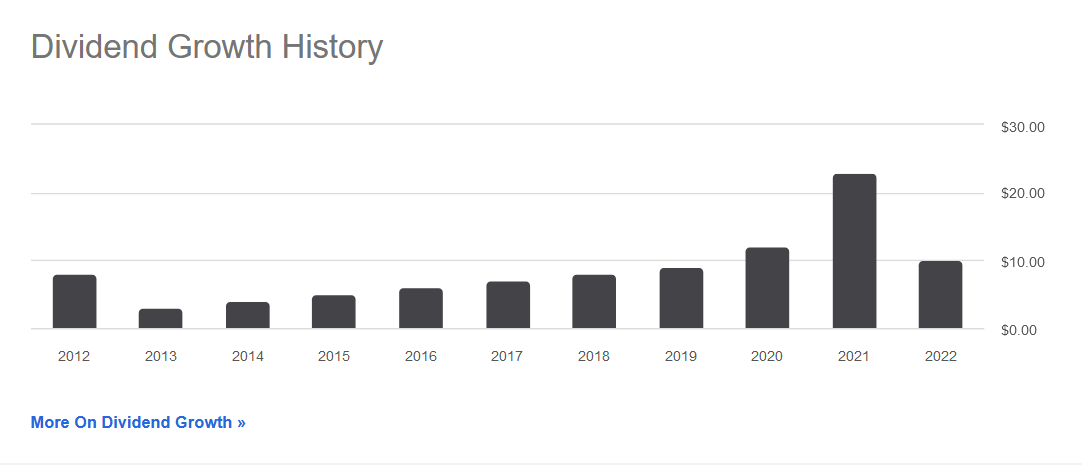

Dividend History (Seeking Alpha)

The company has a history of raising the dividend very well and going back the last 10 years for DHIL we can see a clear increase for the business. I think that this will continue and the market uncertainties right now are a reason for the lack of growth. I would rather see the management post new increases when the market conditions improve and for them to also be buying back shares during these times as well.

Shares Outstanding (Seeking Alpha)

Looking back at the shares for DHIL they have been reducing at a very steady level as DHIL aims to maximize the shareholder returns. I think that buying back shares now seems like a fair idea as the p/e for the business is quite in line with the rest of the business and it therefore exhibits less of a premium to be bought at.

Risk Associated

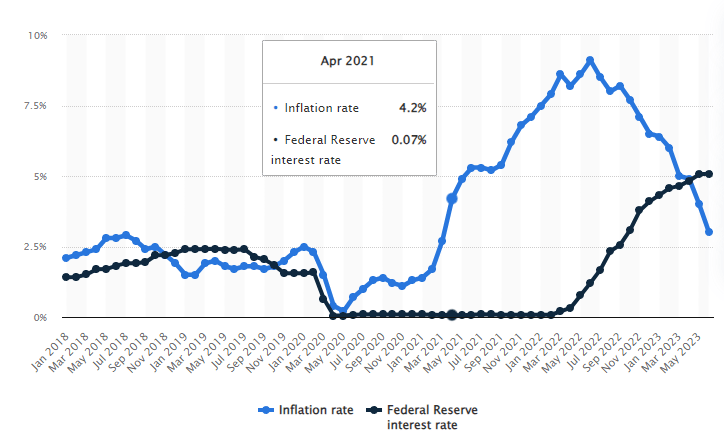

At present, one of the primary concerns surrounding DHIL revolves around the Federal Reserve’s tightening monetary policies. The prospect of further interest rate hikes could potentially impact the performance of DHIL’s investments, potentially leading to capital outflows as investors explore alternative shelter options. However, amidst these concerns, DHIL has demonstrated a robust balance sheet and readily available capital during challenging periods.

Inflation Rate (Statista)

This resilience in the face of economic headwinds suggests that DHIL may still hold substantial long-term potential, with short-term challenges representing temporary obstacles. While the Federal Reserve’s actions may introduce uncertainty into the investment landscape, DHIL’s ability to weather economic fluctuations and maintain a solid financial foundation could ultimately position the company to capitalize on opportunities as they arise.

Investor Takeaway

DHIL has been a solid performer over the last 10 years as the asset base and the EPS have both been growing at a double-digit rate annually for the last decade at least. I think that DHIL exhibits a solid buy right now as the share price has seen a decline over the last 12 months. With a yield approaching 4% quite quickly too I think investors will do very well with DHIL over the coming decades. This brings me to rate the company a buy right now.

Read the full article here