Daseke (NASDAQ:DSKE) recently noted a beneficial outlook with regards to the growing demand in the building materials sector. Management also announced further acquisition of tractors and lower maintenance costs, which may bring significant FCF margin growth in the coming years. I did find risks with regard to competition, transformation, restructuring, and total amount of debt, however DSKE does look undervalued.

Daseke

With fleets of trailers that exceed ten thousand units and more than 4 thousand tractors in its ownership, Daseke is a North American company that offers solutions for loading and transportation, specifically specialized in the end markets of certain industries.

The company’s operations extend to Canada and Mexico. In addition to providing cargo services, Daseke also offers the planning of logistics systems for its clients and various storage options. During 2022, the company provided services to more than 4,500 clients, some of them are part of the Fortune 500 list. In the same year, the concentration of income from the top ten clients did not exceed 27% of annual income.

Operations are divided into two reportable segments: truck solution and specialty solutions. The truck solution segment provides logistics operations that only involve trucks, while the specialty solutions segment responds to trips that need to be made with specialized vehicles due to the type of cargo. Logistics and storage services are folded into each of the segments.

Daseke combines a fleet of vehicles under its ownership with trips of light assets, contracted to third parties or with rented transportation. The last type of operation represented more than 50% of the company’s activities in the last year.

In my view, the benefit of the combined business model is to be able to respond to the schedule needs of its clients as well as to have a diversified number of options to designate transportation according to route and types of cargo.

Shareholders May Need To Follow The Total Amount Of Debt

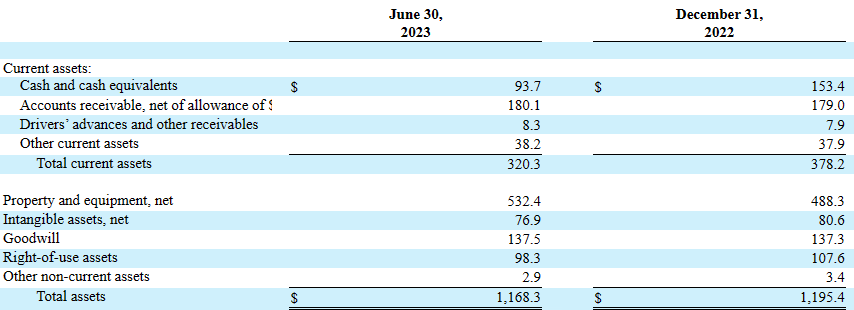

As of June 30, 2023, DSKE reported cash and cash equivalents worth $93.7 million, accounts receivable of $180.1 million, and drivers’ advances and other receivables close to $8.3 million. Total current assets are equal to $320.3 million, more than 1x the total amount of current liabilities. Therefore, the current ratio appears stable.

Also, with property and equipment of $532.4 million, which is the largest asset reported, DSKE reported goodwill of about $137.5 million and total assets close to $1.168 billion. The asset/liability ratio is larger than 1x. In sum, I believe that DSKE appears to have a solid balance sheet.

Source: 10-Q

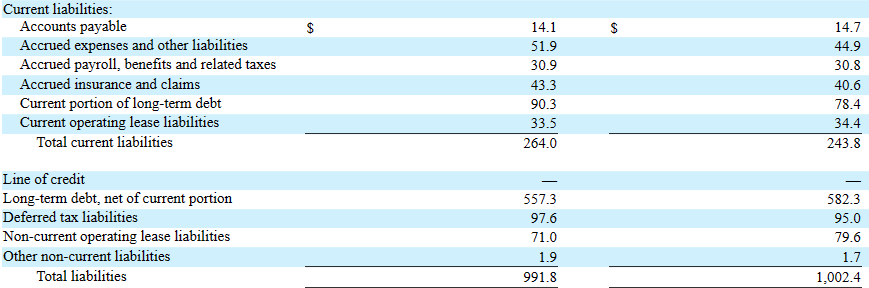

I am really not concerned about the list of total liabilities, however investors may want to have a close look at the balance sheet, which does not seem that small. With accounts payable worth $14.1 million, accrued expenses and other liabilities of $51.9 million, and accrued payroll, benefits, and related taxes close to $30.9 million, current portion of long-term debt stood at $90.3 million.

Long-term debt stands at $557.3 million, which is a bit below what the company reported in the past. Further reduction in the long term debt will most likely bring the interest of investors. Total liabilities stand at close to $991.8 million.

Source: 10-Q

DSKE Is Paying Interest Rate Close To 8.39% and 4.75%. So, The WACC May Not Be Far From These Figures

I studied a bit the terms of the Term Loan Agreement signed by JPMorgan Chase (JPM), which appears to be the largest financing institution offering debt facilities to DSKE. The debt agreement includes a rate of close to LIBOR plus 4.00% per annum among other conditions. DSKE also reported an ABL Facility including debt with 8% interest rate. With these figures, I think that the cost of capital in any financial model may not be far from 7%-13%.

The terms of the Replacement Term Loans are governed by a $400.0 million term loan facility (the Term Loan Facility) evidenced by a Term Loan Agreement dated as of February 27, 2017 (as amended, restated, supplemented or otherwise modified from time to time, the Term Loan Agreement), among the Company, the Term Loan Borrower, JPMorgan Chase Bank, N.A. The Replacement Term Loans are, at the Company’s election from time to time, comprised of alternate base rate loans (an ABR Borrowing) or adjusted LIBOR loans, with the applicable margins of interest being an alternate base rate (subject to a 1.75% floor) plus 3.00% per annum and LIBOR (subject to a 0.75% floor) plus 4.00% per annum. As of December 31, 2022 and 2021, the interest rate on the Term Loan Facility was 8.39% and 4.75%, respectively. At December 31, 2022, the interest rate on the ABL Facility was 8.00%. Source: 10-k

The Outlook Given For The Years 2023 And 2024 Includes Resurgence Of Wind Demand From The Back-half Of 2023 to 2024

I believe that the first part of the year 2023 included certain deceleration, which was noted in the last quarterly report. Having said that, it appears quite beneficial that management expects a surge in demand in 2024 and 2023. I believe that the following words are a must-read for shareholders.

We expect load availability to remain tight but stable, and absent a deceleration in the wider economy, we expect freight rates to be stifled in the near-term as capacity continues its slow exit from the industry. Further, we expect current conditions to persist for the remainder of the third quarter, followed by a more gradual fourth-quarter slowdown, typical of the seasonality in our prior years. We have seen some demand degradation in the building materials complex served by our Northwest flatbed operations, and we are expecting a shift in the resurgence of wind demand from the back-half of 2023 to 2024. Source: 10-Q

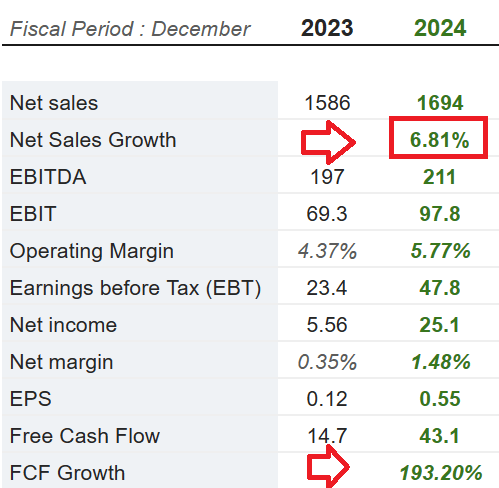

Market analysts indicated beneficial figures for the year 2024, including net sales growth, operating margin growth, and FCF growth. I did use some of these figures in my DCF model, so I invite readers to have a look at the figures of other investment analysts.

Source: Marketscreener.com

Transformation That Started In 2023 Will Most Likely Bring FCF Margin Growth

Within the framework of the inflationary behavior of the market in the last year, the company is carrying out restructuring in its business model with the main objective of achieving a reduction in the cost structure.

Daseke is carrying out the restructuring of its business model, accompanied by the open acquisition strategy and the proposal to combine the dual model of assets under its ownership along with leased assets to fulfill operations. I believe that synergies, integration, and opportunistic expansion into incremental services will most likely bring FCF growth in the coming years. The restructuring plan appears to be under execution in 2022, but also in 2023.

The Company internally announced a phased integration and restructuring plan. Our goal is to drive synergies and improve profitability through cost reduction, network optimization and commercial initiatives which will be facilitated by the continued integration of our operating companies into a subset of our highest-performing platform companies. We believe these measures will unite teams across the Company around a culture of close coordination and continuous improvement, providing for opportunistic expansion into incremental services, geographies, and industrial end markets. Source: 10-Q

Source: 10-Q

Investments In Company Tractors And Lower Maintenance Costs Announced May Bring FCF Margin Growth

In the most recent quarterly report, DSKE noted recent organic investments in tractors, and promised lower maintenance costs. As a result, I believe that we may see an improvement in the FCF margin in the coming years, which could enhance the valuation of the stock.

We continue to make organic investments in company tractors, which support our asset-right strategy and maintain a low average age of fleet, thereby reducing maintenance costs. Source: 10-Q

Financial Model

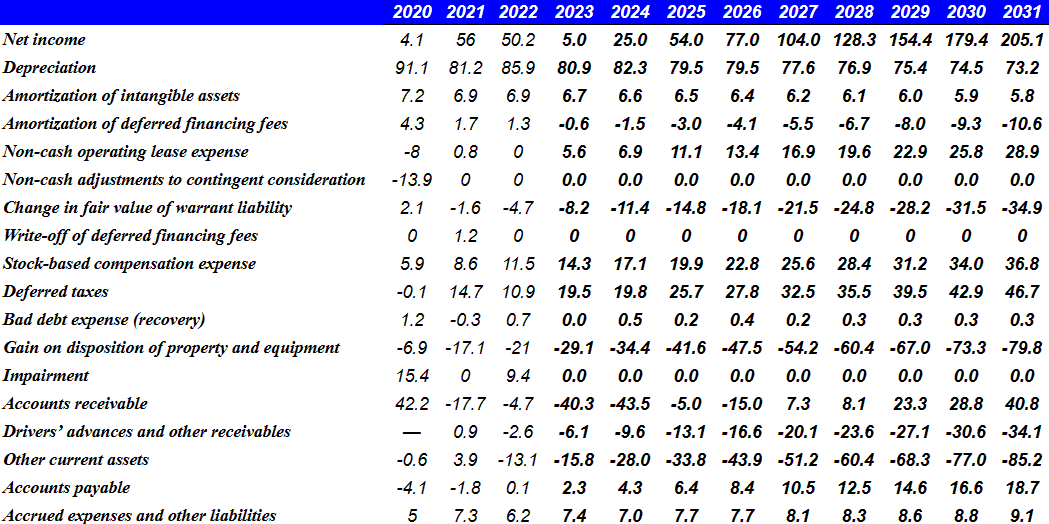

My cash flow model includes forecasts about future cash flow statements from 2023 to 2031. I assumed net income growth, D&A growth, and conservative FCF growth.

I did assume no non-cash adjustments to contingent consideration, write-off of deferred financing fees, bad debt expenses, and impairments because I believe that they are extraordinary events.

My assumptions include 2031 net income close to $205 million, depreciation of $73 million, amortization of intangible assets worth $5 million, and amortization of deferred financing fees close to -$11 million.

Besides, with 2031 non-cash operating lease expense of about $28 million, 2031 change in fair value of warrant liability close to -$35 million, and stock-based compensation expense of $36 million, I assumed changes in accounts receivable of about $40 million.

Finally, with changes in accounts payable worth $18 million and accrued expenses and other liabilities of about $9 million, I obtained 2031 CFO of about $220 million. If we also assume 2031 purchases of property and equipment worth -$44 million, 2031 FCF would be close to $177 million.

Source: DCF Model

Source: DCF Model

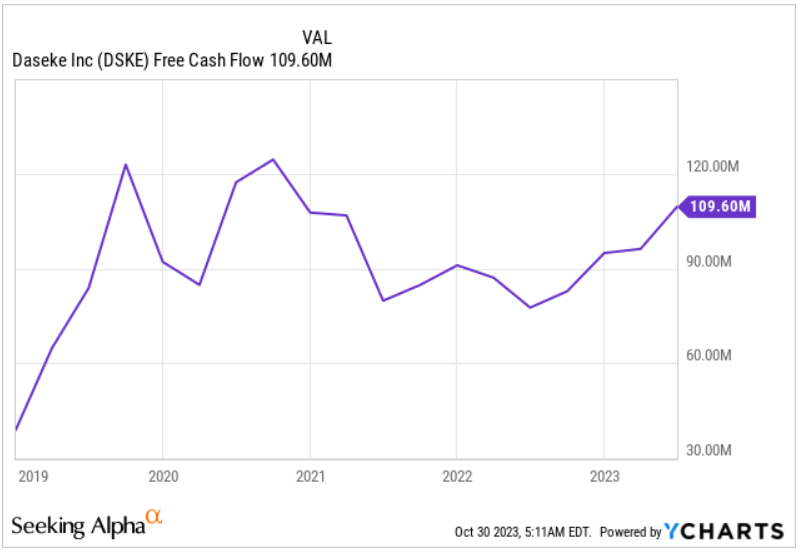

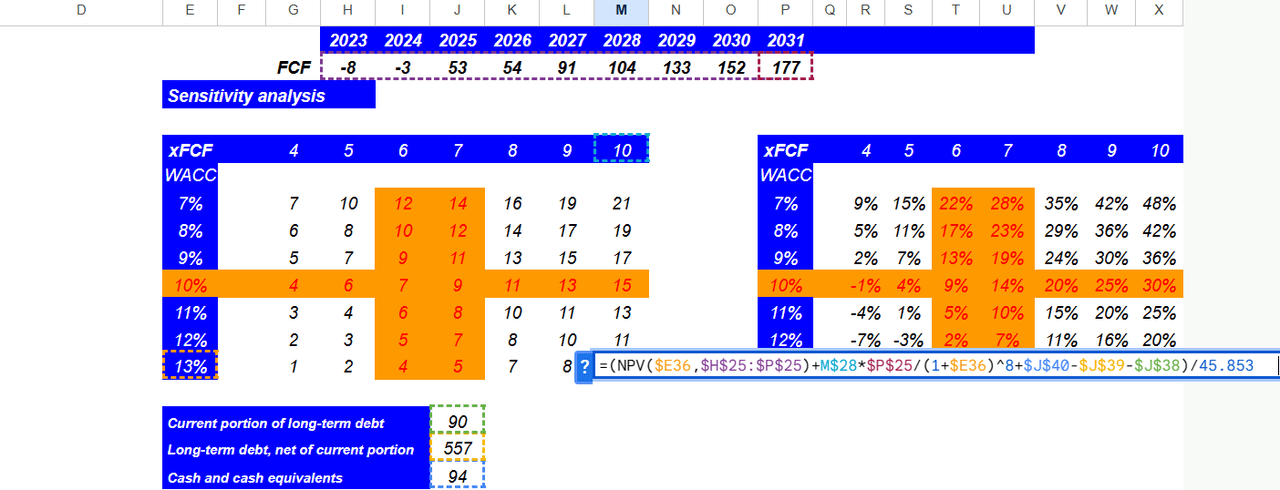

With the previous assumptions, I obtained FCF between -$8 million and $177 million, which I believe are conservative figures in line with the previous FCF numbers.

Source: Ycharts

Also, with a WACC between 7% and 13.1% and a FCF multiple between 4x and 10x, the implied valuation resulted in a fair price of $1-$21 with a median forecast close to $7-$9. The internal rate of return forecasted was a maximum of 48% with a median IRR of 9%-14%.

Source: DCF Model

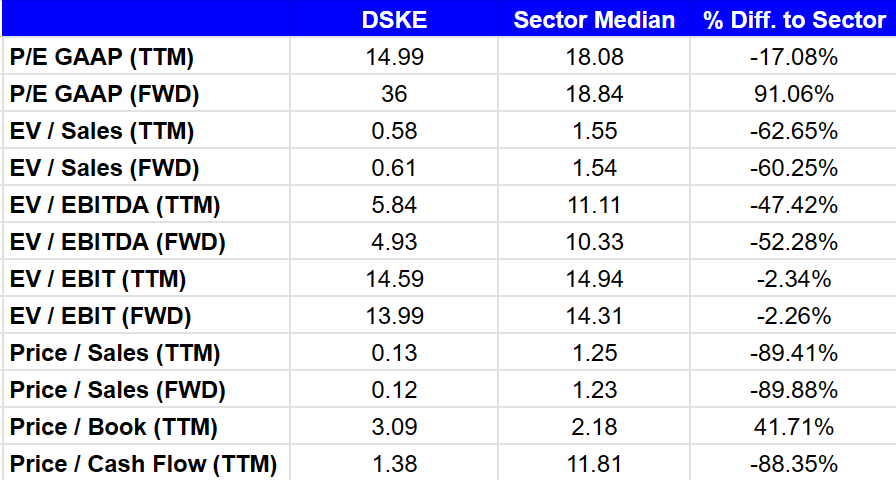

For the assessment of the exit multiple, I took a look at the valuation of the sector and the valuation of DSKE. I really believe that the company is undervalued considering that the sector median includes price / fwd sales of 1.23x and price / ttm cash flow of 11.81x.

Source: SA

Competitors

Since Daseke transports with open-top trucks, the competition is in a certain sense less than in the traditional market, since it is necessary to obtain a series of permits for the transportation of specific loads, and the conditions for entering the market are higher. Wit that, there are a large number of participants, to a lesser extent with fleets of national scope and with great fragmentation with regard to regional markets. Likewise, the infrastructure developments of some of its clients generate indirect competition for the company.

Risks

The concentration of its clients on specific markets means a risk insofar as the dependence it implies on the activity of these markets. Cases such as the one in 2020 with the suspension of commercial aviation activity can translate into a pause in many airline operations.

On the other hand, the company reports that it has not yet been able to establish clear forecasts on the current results in relation to growing inflation. We must say that the restructuring plan also entails risks, in the possible impacts that exist on future business integrations. These factors add to the volatility that the company’s share price has experienced in recent years.

Conclusion

Daseke communicated a transformation period that started in 2022, and is continuing in 2023. The company recently noted further acquisition of tractors and lower maintenance costs, which may bring lower FCF margin in the coming years. Also, considering the beneficial words about the demand for the incoming year 2023, DSKE may become even more followed by the investment community. Yes, I did identify several risks coming from competition, the total amount of debt, or integration, however DSKE does look undervalued right now.