The sell-off in the precious metals sector – which I will argue vehemently is primarily an officially sanctioned, bullion bank market intervention with some help from momentum-based hedge fund algo programs – is startlingly similar to the September/October 2008 decline.

Incredibly, the financial markets, banking system and economic backdrop is also remarkably similar, except this time adverse variables that could lead to a system meltdown like 2008 are more powerful and likely will lead to more severe stock and credit market melt-down.

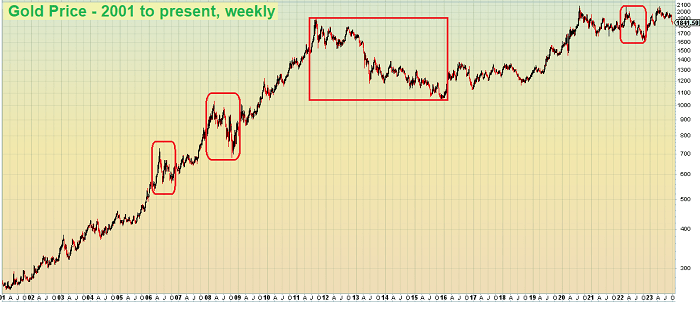

Despite the sharp decline in gold and silver over the past several weeks, relative to 2008 both metals are holding up remarkably well:

The chart above shows the price of gold from 2001 to present on a weekly basis. The price declines in 2006, 2008, late 2011 to late 2015 and early 2020 were much bigger on a percentage decline basis than has been experienced in the recent price decline.

To be sure, it’s impossible to know if there will be more pain in gold and silver or if a bottom is forming.

While the current condition of the economy, credit markets and banking system – all three of which are transitioning into a state of distress – is remarkably similar to 2008, there are factors helping to support the precious metals sector which are present now but not in 2008.

The most significant factor is the enormous demand for physical gold from eastern hemisphere Central Banks and investors. In fact, according to the World Gold Council [eastern] Central Bank gold buying hit a record high in the first half of 2023.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here