Although I am not one to talk because of how little time I dedicate to the outdoors, I do recognize that spending time outside and being active is healthy and recommended. One company that exists with the sole purpose of making that kind of active lifestyle easier and more enjoyable is Columbia Sportswear Company (NASDAQ:COLM). The firm focuses on the production and sale of lifestyle apparel, footwear, accessories, equipment, and other related offerings. But as its name suggests, it really is focused on such items centered around the idea of active living.

Almost a year ago, back in November of 2022, I found myself taking a bullish stance regarding the company. In the article that I had written about it at the time, I recognized that sales and profits we’re doing quite well. The stock did not look cheap compared to similar firms. But it was cheap on an absolute basis. This made me believe that further upside existed for investors from that point. Fast-forward to today, and the ‘buy’ rating on the stock has not exactly played out well.

While the S&P 500 is up 6.8%, shares of Columbia Sportswear have seen downside of 15.2%. Even though the stock has fallen in price, its trading multiple has gotten a bit higher. This is because of some disappointing financial results. For the current fiscal year, the company has come under further pressure from a fundamental perspective. And that causes me to be a bit more cautious. Of course, the picture could change. And any such change likely would come when earnings are announced in the coming days. But until we see something more concrete, I do believe that a ‘hold’ rating is appropriate for the business at this time.

Keep an eye out on earnings

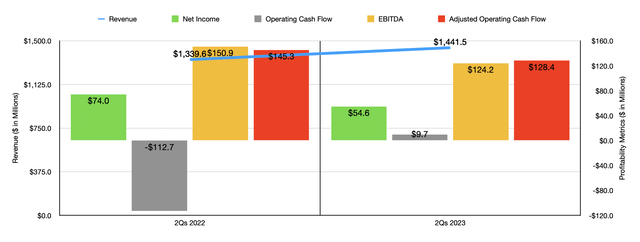

To be perfectly honest with you, things have not been going the best for Columbia Sportswear and its investors. As an example, we need only look at data covering the 2023 fiscal year so far. From a revenue perspective, things have actually gone quite nicely. Revenue in the first half of the year totaled $1.44 billion. That’s 7.6% above the $1.34 billion reported one year earlier. During this time, there were some weak spots for the company. For instance, revenue associated with the prAna brand dropped 18% year over year, while for Mountain Hardwear sales dropped 2%. This was more than offset, however, by the Columbia and SOREL brands, with sales up 10% and 7% year over year, respectively, while on a constant currency basis, they jumped 12% and 8% year over year, respectively.

Author – SEC EDGAR Data

Most of the strength for the company came, perhaps unsurprisingly, from the wholesale side. Revenue spiked 10% in the first half of this year compared to the same time last year. Management attributed this to earlier shipments of Fall 2023 international distributor and wholesale orders. Interestingly, the picture would have been even better. But management specified that the Columbia and SOREL brands were negatively impacted by what management called ‘challenging dynamics’ in the footwear market. Direct to consumer growth, meanwhile, was a more modest 5%.

So far, so good. The company also benefited from the fact that its gross profit margin remained unchanged year over year. But that didn’t stop net income from plunging from $74 million to $54.6 million. The problem seems to have been largely associated with selling, general, and administrative costs. These shot up from 43.3% of sales last year to 45.8% this year. Higher supply chain costs of $27.6 million, which stemmed from increased global distribution center costs thanks to high inventory levels, were the primary problem. However, Omnichannel expenses jumped $24.8 million year over year because of an increase in direct-to-consumer costs.

Author – SEC EDGAR Data

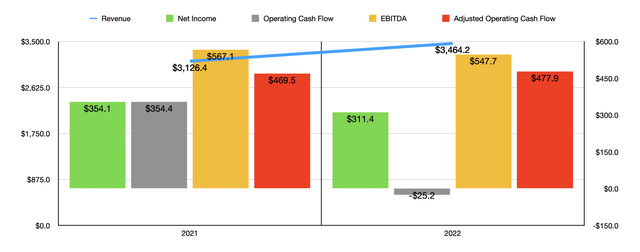

Other profitability metrics mostly followed suit. The big exception was operating cash flow. It went from negative $112.7 million to positive $9.7 million. But if we adjust for changes in working capital, we get a decline from $145.3 million to $128.4 million. Meanwhile, EBITDA for the business shrink from $150.9 million to $124.2 million. Interestingly, this year is not the first time that we saw attractive sales growth but weak bottom line results. If you look at the chart above, you can see financial data covering both 2021 and 2022. Three of the four profitability metrics shown in that chart worsened from one year to the next, while revenue increased nicely. So this is part of a larger trend for the enterprise.

Author – SEC EDGAR Data

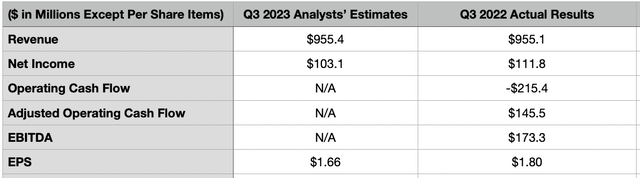

Of course, the picture can always change. And that’s why investors should be paying attention to when management reports financial results for the third quarter of the company’s 2023 fiscal year. This data should come out on October 26th. At present, analysts are forecasting revenue of $995.4 million. That would be higher than the $955.1 million reported one year earlier. Earnings per share, meanwhile, are expected to come in at $1.66. This could also be fitting considering recent performance. Last year, in the third quarter, the company generated profits of $1.80 per share. That translated to net income of $111.8 million. We should also be paying attention to other profitability metrics. For context, operating cash flow for the third quarter of 2022 came in at negative $215.8 million. On an adjusted basis, we are looking at $145.5 million. And finally, EBITDA at that time totaled $173.3 million.

In addition to financial performance for the most recent quarter, investors should also be paying attention to guidance provided by management. Revenue for 2023 is currently expected to come in at between $3.53 billion and $3.59 billion. But that’s actually a decrease compared to even earlier guidance that called for revenue of between $3.57 billion and $3.67 billion. Even so, that would represent a 2% to 3.5% increase in revenue year over year. Earnings per share were also downgraded when management reported results in the second quarter. Initial guidance called for earnings of between $5.15 per share and $5.40. That number has now been lowered to between $4.40 and $4.65. It would be interesting to see if the firm lowers guidance again. If so, that would be problematic.

Author – SEC EDGAR Data

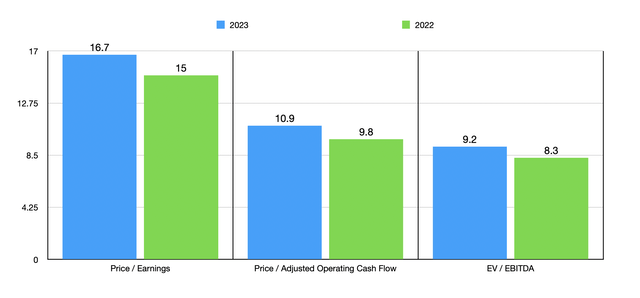

Even if we assume that management is correct, total net profits this year should be around $279.6 million if the company hits the midpoint of guidance. That would be down from the $311.4 million generated in 2022. Based on my own estimates, adjusted operating cash flow should be around $429.1 million, while EBITDA should be around $491.8 million. In the chart above, you can see how the company is priced on both a forward basis and using data from last year. The stock is not exactly the cheapest on the market. But I wouldn’t say it’s expensive by any means. Compared to similar firms as shown in the table below, the stock is about average. Four of the five companies ended up being cheaper than it from a price to earnings approach. This number drops to three of the five using the EV to EBITDA approach and to two of the five using the price to operating cash flow approach.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Columbia Sportswear Company | 16.7 | 10.9 | 9.2 |

| PVH Corp. (PVH) | 25.5 | 12.0 | 9.0 |

| Under Armour (UAA) | 8.5 | 36.5 | 7.6 |

| Hanesbrands (HBI) | 6.4 | 7.2 | 12.5 |

| Gildan Activewear (GIL) | 10.8 | 20.6 | 9.3 |

| Carter’s (CRI) | 12.8 | 6.6 | 8.0 |

Takeaway

Heading into earnings, the picture regarding Columbia Sportswear looks intriguing. At present, analysts don’t have that much hope for the company from a profitability perspective. And if the recent past is any indication of the future, that is a realistic way to think about things. Don’t get me wrong. My belief is that Columbia Sportswear is a solid company. In fact, the company has no debt on hand, and it enjoys $302.8 million in cash and cash equivalents. That puts it on sturdy footing. But with recent bottom line results and the expectation that the trend will continue, and when you consider how shares are priced compared to similar firms, I do believe that there are better prospects that can be had at this time.

Read the full article here