After a sharp reopening in the first quarter, the challenges of the Chinese economy have reasserted themselves, causing numerous economists to downgrade their expectations for the country’s economic growth. Numerous media publications have also chimed in on the matter as well.

We think that downside risks have opened relative to our 5% GDP (gross domestic product) expectation, and believe that the current approach of small, targeted stimulus is not enough to change the situation. However, we do feel that some of the recent measures on the property market could prove supportive.

China’s economy falls short of economists’ expectations

Before digging into the challenges that China is facing, let’s take a temperature check of where its economy is. In short, China has been surprising to the downside since June of this year, as evidenced by the Citi Economic Surprise Index chart. This chart shows how economic data has come in relative to economists’ expectations. A negative number means that the data has been softer than expected, and vice versa. As shown, the magnitude of the surprise for China this time around has recently been in line with previous shocks to the economy, including 2014 and 2015. Note that the COVID-19 experience is not a useful comparison given the scale of the shock that was experienced.

Source: LSEG Datastream, Citi, 7 September 2023

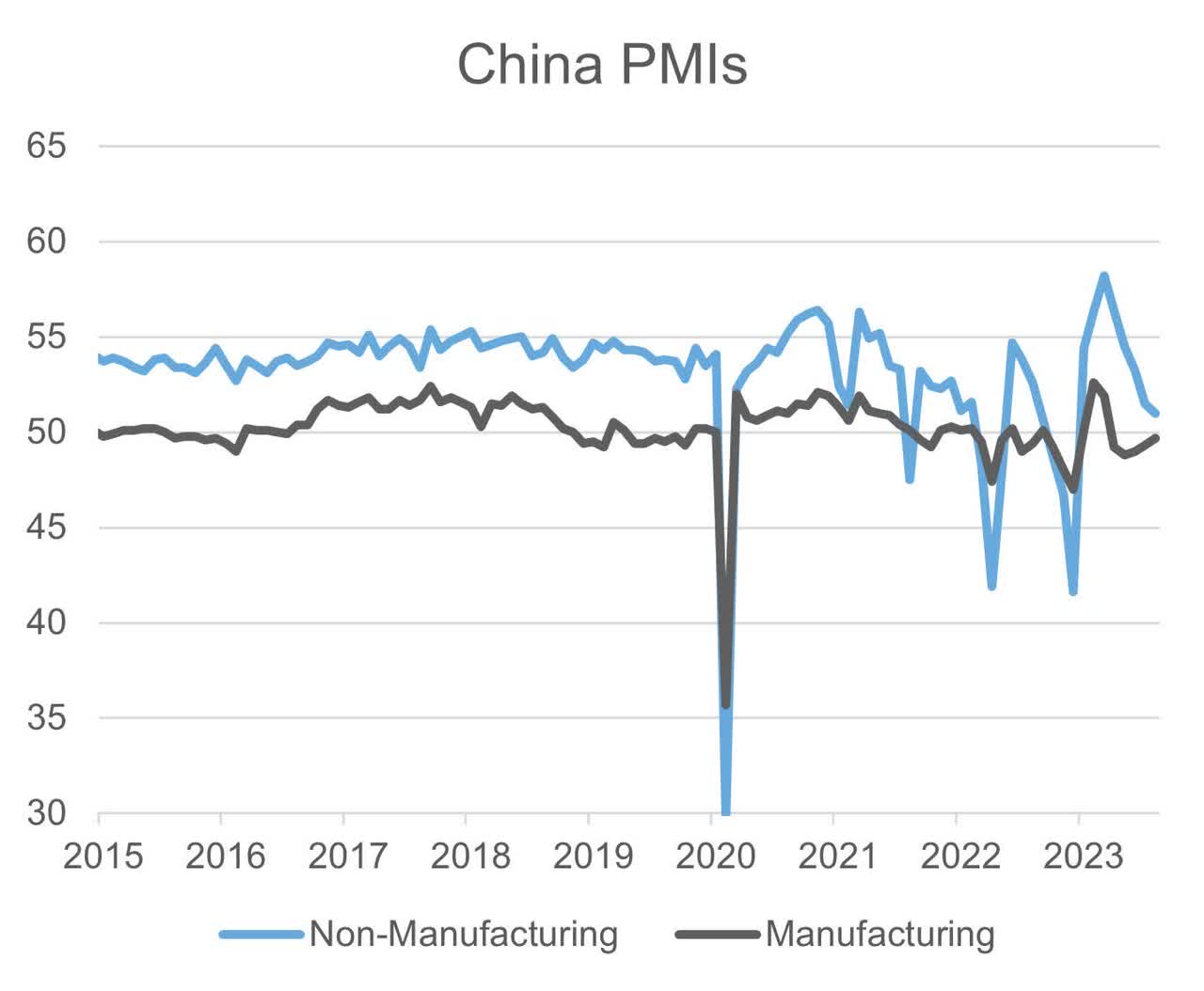

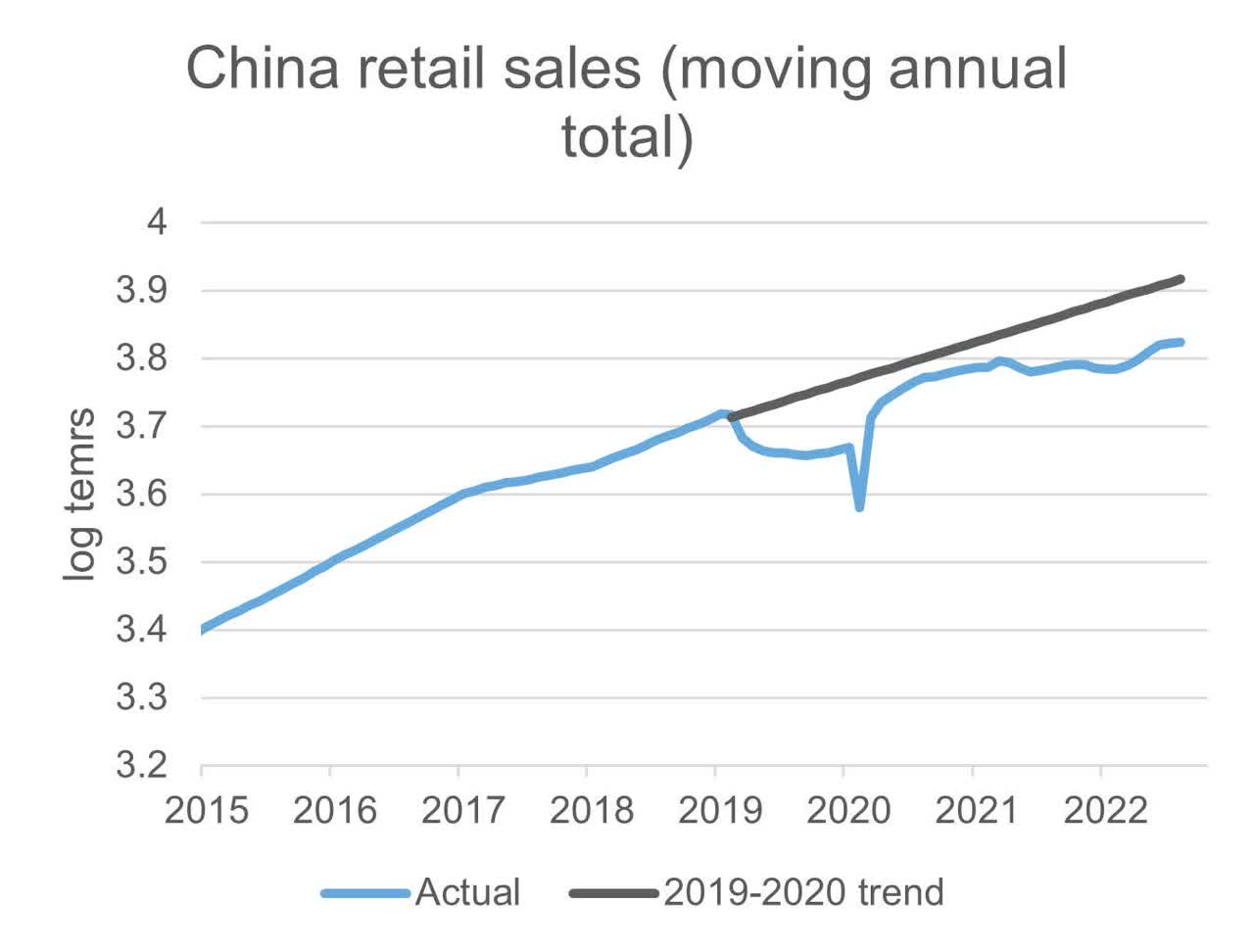

The expectation at the start of the year was that China would see a pickup in consumption and the services economy, as the population re-engaged with the economy post-lockdown. We did see this very early in 2023, with the services PMI (shown in the chart below) jumping to very elevated levels. However, it quickly fell as the reopening impulse faded quicker than many economists had expected. We also see this same dynamic playing out in consumer spending, with the recovery in retail sales starting to plateau.

Source: LSEG Datastream, 7 September 2023

Source: LSEG Datastream, Russell Investments, 7 September 2023

Consumer confidence needs a boost

In the near term, the key challenge China faces is that consumer confidence is soft and has led to a weaker spending impulse. One of the key reasons for the depressed confidence is that the property market is still struggling. Most of Chinese household wealth is tied up in real estate, and so the state of the real estate market has a big impact on consumer confidence.

Recently, we have seen some measures announced that could provide some support to the upper-tier cities (e.g., Shanghai, Beijing, and Guangzhou). Authorities have expanded the first home buyer category, which means that more households will have access to lower down payments and lower interest rates, which could improve demand in the near term. This could have an outsized impact on the total economy given that excess savings in China are unevenly distributed and largely with wealthier individuals. However, we expect the overall impact to still likely to be modest.

The challenge with local government debt

The bigger challenge that has been a key topic of debate within China is the level of local government debt. Effectively, the central government gave the local governments the ability to borrow money for infrastructure spending coming out of the Global Financial Crisis (GFC), and that has eventually led to extremely elevated debt levels.

Additionally, the slowdown in the real estate sector has weighed on land sales – which is one of the major revenue sources for these local governments. This means that the usual stimulus path is a bit more challenged right now, but that does not mean that a policy response has become constrained. The central government can provide debt-for-debt swaps with the local governments, as well as provide some of the fiscal spending themselves. This is even more so given China’s very elevated savings rate – effectively, the government would be sopping up elevated savings and recycling them into the real economy.

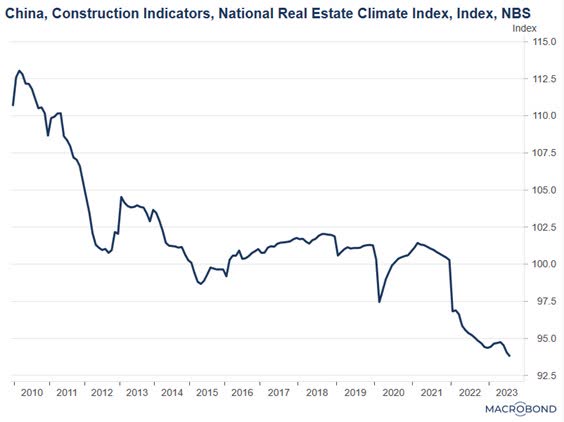

What’s behind China’s real estate woes?

Let’s focus on the real estate sector now. Developers continue to be under a lot of stress, as demand for new homes remains depressed and they are heavily indebted. This is unlikely to abate anytime soon, with more than $6 billion in bond payments due from developers over the next five months.

The Chinese authorities have continued to make piecemeal approaches to alleviate some of the liquidity issues with developers, and we expect that more efforts will be made at that – with one avenue being that state-owned developers will take on more assets of those indebted private developers. In particular, the fate of Country Garden (OTCPK:CTRYF, OTCPK:CTRYY), one of the larger developers operating in China, has been extended on the news that the company met its bond payments. However, there is likely to be more volatility in the near term given the payment profile that is due. Overall, property transaction volumes will be closely monitored by the market in the coming months.

Source: Macrb

The pain point for more stimulus is not here … yet

We don’t believe that we have reached the pain point – that is, the point at which the Chinese government is forced to do more stimulus – just yet. We think that we will need to see a bit more slowing in the economy, and some more softening in the labor market, to bring that stimulus forward. The situation with the labor market has become a bit more challenging to analyze as the youth unemployment rate (which was showing the extent of the challenges) is no longer being published, although we still have broader employment data that we can use.

Equity sentiment is oversold, but not at panic

Chinese equities continue to look quite cheap, with the MSCI China Index trading at forward earnings multiple of less than 10. This compares to the S&P 500 Index multiple of 19 times. Given the cyclical headwinds, but the potential for more meaningful stimulus, we think that caution should be applied in the short term.

Source: LSEG Datastream, Macrobond, Russell Investments, 5 September 2023

Our proprietary sentiment indicator for Chinese equities is showing that the Chinese market is oversold, but not yet at levels of panic/capitulation that would represent a strong opportunity. We will be closely monitoring this, as well as future stimulus announcements and economic data, in the coming months.

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the “FTSE RUSSELL” brand.

The Russell logo is a trademark and service mark of Russell Investments.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

UNI-12287

Original Post

Read the full article here