Ceragon Networks Ltd (NASDAQ:CRNT) has carved a niche in wireless backhaul solutions, a sector that should benefit from the advent of 5G. In my view, this positions CRNT’s diverse offerings, from voice services to IoT connectivity, to profit from secular tailwinds. CRNT’s recent financial data indicates a promising margin improvement. Additionally, details from their most recent earnings call suggest they are gearing up for new product launches, aligning with the anticipated global wireless backhaul market growth. However, the broader telecommunications industry has challenges, especially with consolidation. I believe CRNT’s relatively modest size might challenge navigating this landscape. Overall, based on my valuation analysis, CRNT’s fair value is around $161.3 million. Given this assessment, I think that its current market valuation doesn’t offer a particularly enticing investment proposition, leading me to maintain a neutral stance on CRNT.

Business Overview

Ceragon Networks operates in the Technology and Communications industry, with a niche in wireless backhaul solutions. These solutions are designed to aid cellular operators and various service providers in enhancing their networks, especially as we transition into the 5G era. The company’s portfolio includes voice, Machine-to-Machine (M2M) solutions, broadband, and IoT connectivity. Given the rapid digital transformation, such offerings are becoming increasingly essential. Interestingly, CRNT’s reach isn’t limited to just telecommunications; they also serve public safety and offshore drilling sectors. With operations from Asia-Pacific to the Americas and headquartered in Rosh Ha’Ayin, Israel, I believe CRNT’s global presence allows them to cater to a broad spectrum of market demands, positioning them for potential growth in the evolving tech landscape.

Between December 2022 and June 2023, the company experienced a subtle yet noteworthy growth in its total assets, increasing from $289.3M to $294.5M. This increment, albeit modest, offers a buffer against unpredictable market shifts. A pivotal aspect of the company’s recent financial trajectory is the remarkable recovery in net income, which transitioned from a $3.8M loss to a $4.1M profit in a mere six months. This upward shift, accentuated by a minor rise in total current assets from $210.7M to $215.8M, indicates enhanced operational efficiencies. It’s plausible that these efficiencies stem from well-executed cost-reduction strategies (more on this later). Also, CRNT’s cash flow dynamics corroborate this positive trend, with net cash from operating activities transitioning from a $4.9M deficit to a $6.7M surplus.

CRNT’s website.

Outlook and Promising Margin Expansion

During CRNT’s latest earnings call, the company discussed its upcoming product roadmap, highlighting its strategy to reduce BOM costs using ASIC advancements as 2024 approaches. Doron Arazi, the CEO of CRNT, underscored the company’s dedication to introducing a revamped version of select products. These innovations are designed to adeptly merge technological requirements with considerations of total cost of ownership (TCO). In my view, Arazi’s confirmation that these products are set for a commercial debut shortly enriches the company’s current offerings and signals a proactive approach to market demands. CRNT’s CEO also hinted that a next-generation chip with superior capacity features is scheduled for a 2024 launch. While Arazi anticipates that the revenue contribution from this chip might be limited in its debut year, I believe CRNT’s competitive cost structure from the get-go is encouraging. This positions the product favorably in the market, and as sales volumes rise, there’s potential for even healthier gross margins.

Maximize Market Research (maximizemarketresearch.com)

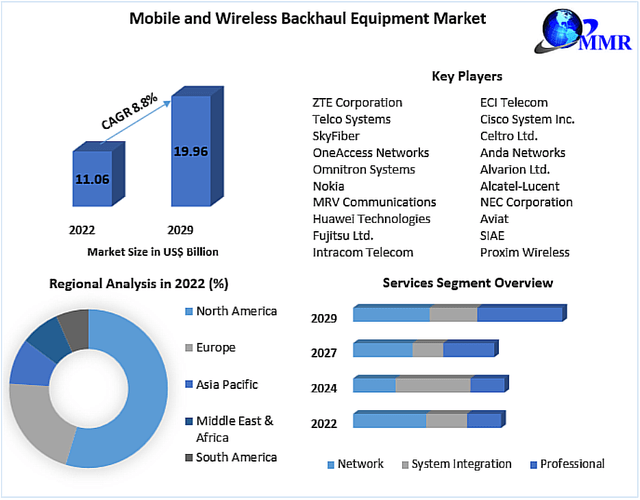

Furthermore, considering broader industry trends, the global wireless backhaul market shows positive momentum. Factors such as the surge in smartphone adoption, the rollout of 5G technology, and the rise in online media consumption drive this growth. These developments highlight an increasing demand for efficient data transportation solutions. In my view, the data underscores the market’s promising potential. It is anticipated to grow at a 12.5% CAGR from 2023 to 2028, with projections indicating a market valuation of approximately $71.77 billion by 2028. I believe that this growth trajectory aligns with CRNT’s strategy to benefit from this growing market.

CRNT’s website.

Unfortunately, the telecommunications sector is undergoing a marked transformation, characterized by a clear trend towards consolidation. Notable mergers, such as the union of T-Mobile (TMUS) and Sprint (S) in the U.S., highlight this shift. This case presents potential challenges for companies like CRNT. For instance, a significant concern is the possible loss of sales to longstanding customers, especially when they merge with companies that favor competitor products or have existing infrastructures that negate the need for further services. This uncertainty can pause new partnerships or product orders, impacting revenue and growth plans. Moreover, there’s a rising trend toward network-sharing agreements, where operators combine their infrastructure resources. While this may be financially beneficial for operators, it reduces the demand for network equipment, potentially impacting revenues for firms in this sector.

Valuation Analysis

In my view, we must rely on valuation multiples to assess CRNT’s valuation, since it’s unprofitable. For this, I believe that given the company’s business model, it’s reasonable to focus on the EV/Sales and EV/EBITDA metrics, which are often used for companies in the Technology sector. CRNT’s forward EV/Sales multiple stands at 0.59, significantly lower by approximately 77.59% compared to the sector median of 2.63. This situation suggests that the market values CRNT’s sales at a discount relative to its peers. Additionally, the forward EV/EBITDA multiple for CRNT is 6.22, which is also considerably lower by about 54.75% than the sector median of 13.76.

CRNT’s financial discipline is evident in its handling of operating expenses. The company has maintained its R&D costs at $7.6 million, representing 8.8% of revenue, down from 10.6% in the prior year. This shift implies that CRNT is achieving more with its R&D investments. Additionally, sales and marketing expenses have been streamlined to $9.4 million or 10.9% of revenue, a decrease from the previous year’s 12.8%. However, a slight uptick in General and Administrative expenses from 6.5% to 7.0% suggests the need for continued oversight.

Seeking Alpha plus author’s elaboration.

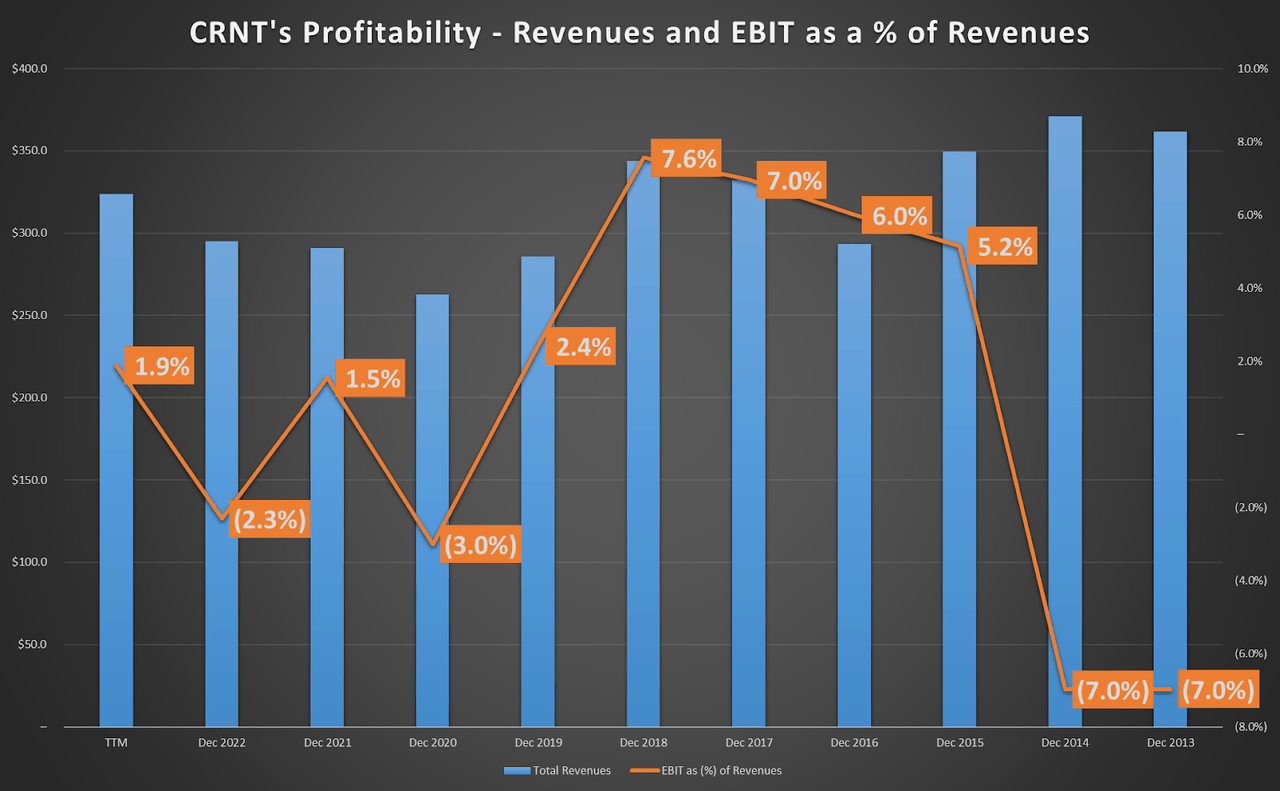

I believe CRNT’s forward-thinking approach is highlighted by its forecasted operating expenses, which range between $22 million and $23 million for the second half of 2023. This would result in an annualized figure of up to $92 million, marking an improvement from the average of $95.9 million since 2013. For context, CRNT’s EBIT margins have hovered around 1.1% since 2013, with a recent uptick to 1.9% in the TTM, suggesting a positive trajectory influenced by operational enhancements. The initial signs of margin expansion and a respectable CAGR of 6.0% in revenues since 2020 suggest CRNT is close to achieving profitability.

TradingView.

Given its ongoing margin improvements, I think it’s reasonable for CRNT’s EBIT margin to stabilize at 2.5% of annual run rate revenues of $350 million. Hence, considering the sector’s median EV/EBIT ratio of around 18, I derive an annual EBIT run rate of $8.75 million. Using a conservative EV/EBIT multiple of 15, CRNT’s enterprise value is estimated at $131.3 million. After accounting for cash and debt adjustments, the implied fair value is $161.3 million. Thus, CRNT seems fairly priced compared to its market capitalization of $170 million. While CRNT showcases promising business fundamentals, its current stock valuation doesn’t present a compelling buy opportunity, leading me to give it a neutral rating.

Conclusions

Overall, CRNT offers a diverse portfolio that seems well-suited to meet the demands of an increasingly digital world. The company’s recent financial milestones and forward-thinking product initiatives suggest the potential for margin improvement. Plus, I believe the expected growth of the global wireless backhaul market underscores these opportunities. However, the ongoing trend of consolidation in the telecommunications sector presents challenges. And, given CRNT’s current lack of profitability, these challenges warrant careful consideration. Thus, based on my valuation assessment, CRNT appears to be trading close to its intrinsic value, leading me to maintain a neutral stance on the stock. The reason for this is the balance between the company’s growth prospects and the inherent risks in the sector.

Read the full article here