DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Cestrian Capital Research, Inc., its employees, agents or affiliates, including the author of this note, or related persons, may have a position in any stocks, security, or financial instrument referenced in this note. Any opinions, analyses, or probabilities expressed in this note are those of the author as of the note’s date of publication and are subject to change without notice. Companies referenced in this note or their employees or affiliates may be customers of Cestrian Capital Research, Inc. Cestrian Capital Research, Inc. values both its independence and transparency and does not believe that this presents a material potential conflict of interest or impacts the content of its research or publications.

Never Revisit Past Glories?

If, like us, you are in the business of investment research, then you are going to get a lot wrong. Stands to reason. Core part of the job. All that. We never mind taking brickbats for being wrong, usually, we’re wrong less often than we’re right, and that’s pretty much where the bar is in our line of work. And we’re happy to say when we got it right, with the rider that what often comes after right is, wrong.

We made some righteous calls on MongoDB (NASDAQ:MDB) in the last year or so. A ‘Buy’ call in December 2022 and again in March 2023, and a ‘Sell’ call in June. Here’s how those ideas fared vs. the S&P 500.

Prior Cestrian Capital Research MDB Ratings

Our Luck Held! (Cestrian Capital Research, Seeking Alpha)

As is typical with highly-strung software names, the company put in a big correction from the market’s July high to the October lows – a drop from around $440 to $320; since which time the name is back up to $392. So the question is, did we hit peak tech stock excitement already, or is there more upside to come?

Let’s first take a look at the company fundamentals.

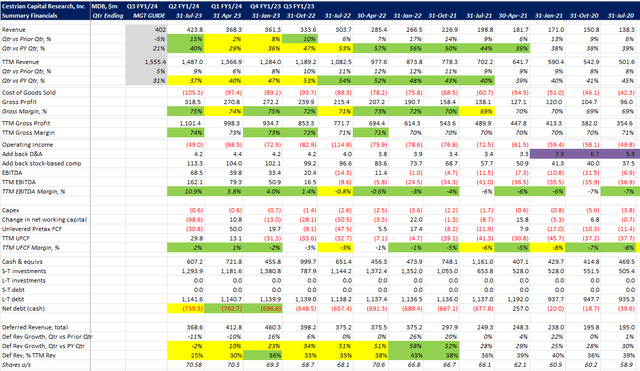

MongoDB’s Financial Analysis

MongoDB Fundamental Analysis (Company SEC filings, YCharts.com, Cestrian Analysis)

The company’s Q2 of FY1/24 was excellent. Revenue growth accelerated to +40% for the quarter vs. the same quarter last year. The company’s Q3 guide looks light, as it implies the fastest slowdown in growth (-5% vs. the prior quarter) that the company has experienced since at least 2018; we know of no particular macro nor company-specific reason why the quarter would be quite that brutal. We anticipate a beat, perhaps only a modest beat, but a beat nonetheless.

Gross margins once again hit record highs of 75% in the quarter and 74% on a TTM basis. TTM EBITDA margins are close to 11% now, and even allowing for the poor working capital management this company exhibits, cash flow is now positive on a TTM basis and has been so for two successive quarters. That may not sound like a big deal, but it is a big deal – the moment these types of software companies go from cash consumptive to cash generative is often an a-ha moment for latecomer investors in such names (and let’s not forget, it is late money that ultimately bids these stocks up so that smart-money early accumulators can then sell at large gains).

The balance sheet is strong enough with $760m of net cash. Fortress it isn’t, but it’s enough to keep the wolf from the door.

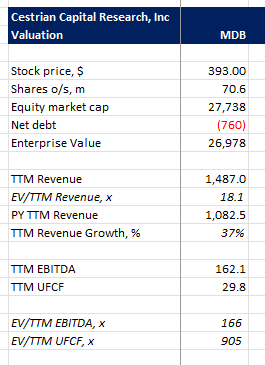

Valuation?

MongoDB’s Valuation Multiples

MongoDB Valuation Multiples (Company SEC filings, Ycharts.com, Cestrian Analysis)

Tough to look anyone in the eye and say, load up on this thing on the basis of fundamentals. 18x TTM revenue for a company that has TTM revenue growth of 37% but is telling the market that TTM growth will drop to 31% next quarter? Not so compelling as a buyer. The thing is, as all investors in high-growth software companies know, stocks like this are always “too expensive” and so very often the multiples have to get truly silly before one should dump the names and walk away, and this isn’t yet silly, it’s just expensive.

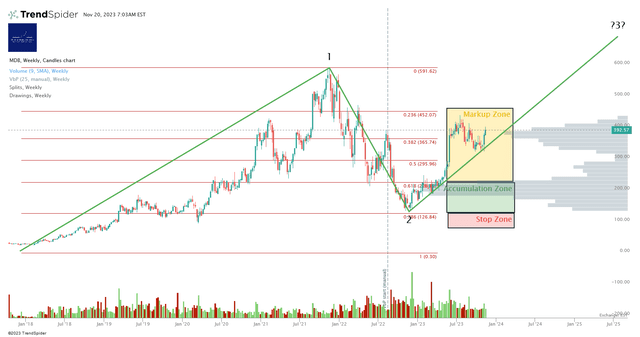

Perhaps the answer lies in the stock chart – certainly, the logic of our Buy and Sell calls above was technical rather than fundamental.

MongoDB’s Technical Analysis

You can open a full-page version of this chart, here.

MDB Stock Chart (Cestrian Capital Research, TrendSpider)

We chart this one using a slightly unusual method. We start the count at a notional 0 per share; clearly, the stock hasn’t ever traded there but for these huge corrections it happens more often than not that the stock finds support at the .786 Fibonacci retrace of the move from that notional zero to the all-time high – that’s the case with MDB stock as you can see. Projecting from the Wave 2 low we might expect a Wave 3 – that’s the current larger-degree move up currently underway – to terminate at somewhere between $592 (a whisker above the all-time high) to a too-difficult-to-contemplate-right-now $1093 (that’s the 1.618 extension of the prior Wave 1 which peaked in November 2021.

Wave Three targets always look silly when you draw them, because to happen the stock has to become the subject of overemotional buying – those late buyers again – which from the depths of Wave 2 misery is plainly impossible to imagine, and once the stocks start to reach the prior Wave 1 highs, one’s own emotions are saying, well, this thing is looking expensive now. This is why we have stock charts of course, to take the emotion out of it.

We believe the current bull market is set to continue. For how long? Well, our base case is that the Nasdaq peaks sometime mid/late next year in the range QQQ420-QQQ460/share. Our bull case? This is our bull case.

And our view on MDB stock hinges on this. If indeed we have a moonshot in the Nasdaq, which is certainly a possibility in our view, then can MDB reach $1000 before rolling over and selling off hard? Sure. Can you plan on that happening? Unwise in our view. If there is a solid if unspectacular up-market in 2024, can MDB reach all-time highs (it’s currently around 2/3 of that price, so a 50%-ish rise from here is needed to recapture the highs)? Probably, as long as it has time to get there and the company doesn’t in fact see growth fall off a cliff as they are guiding.

MongoDB’s Stock Rating

So how to rate this? Well, a label is one thing but we’ll explain how we think about it in staff personal accounts.

- Fundamentals are good, not great. There’s not much in the way of revenue visibility in the business model – deferred revenue is low at just 25% of TTM revenue, and that proportion is falling, i.e., the business model is becoming more contingent, not more certain. There’s no comfort in remaining performance obligation (the total order book, whether already invoiced or not) either, which sits at $482m as of 31 July this year – that’s less than a third of TTM recognized revenue. Cash flow margins are poor vs. other software companies in its class, and the balance sheet is good but unspectacular, meaning that if the company has to acquire its way out of trouble it will have to raise equity (or dilutive convertible debt) to do so.

- The valuation is punchy as noted above.

- The stock chart doesn’t scream buy as it did in Q4 2022/Q1 2023.

In staff personal accounts we took very handsome and quick gains, in the 50% range, earlier this year, and we have not looked back. We have no plans to buy back into the stock because whilst it’s true that the technical upside to $600, $1000, is truly possible, we can think of better uses for capital than this.

So, rating? Buy? No. Sell? No, because with appropriate risk management in place, it’s reasonable for current shareholders to want to ride this up the curve if they can. Hold? That will do it. (Or you could adopt the rating used in our staff personal accounts which is, Do Nothing!).

Any questions, comments, objections, whatever, hit us up in comments below. We read them all and endeavor to answer quickly.

Cestrian Capital Research, Inc – 20 November 2023.

Read the full article here