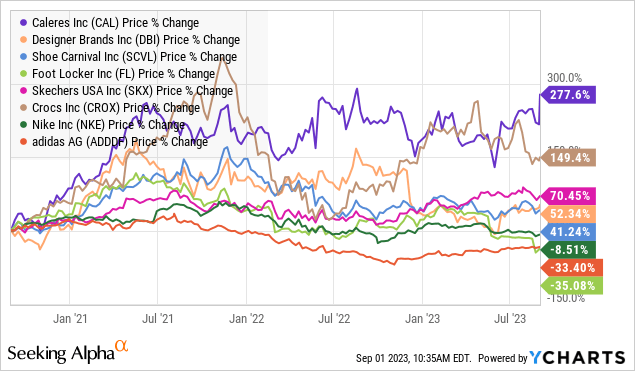

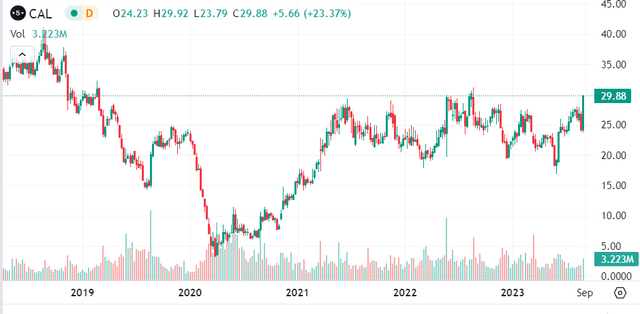

Caleres, Inc. (NYSE:CAL) has quietly emerged as an outperformer in the footwear segment of the market, with shares up more than 30% this year to a 52-week-high. The “Famous Footwear” retailer with a diversified portfolio of in-house brands has been an exception in the industry compared to larger players struggling with the challenging consumer spending environment.

Indeed, since 2020 CAL has climbed nearly 300% while names like Foot Locker, Inc. (FL), and even Nike, Inc. (NKE) are down over the period. The story here is impressive operating and financial trends, with data suggesting Caleres has captured market share in key categories.

The company’s latest earnings beat expectations while management offered positive guidance for the rest of the year. In our view, CAL is a quality small-cap that deserves to be on more investors’ radars. We expect continued earnings momentum as a catalyst for the stock into 2024.

CAL Q2 Earnings Recap

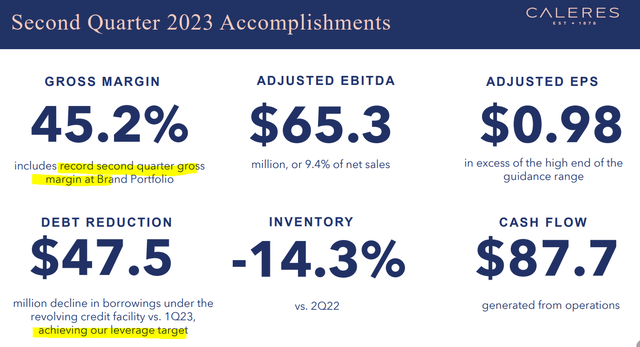

CAL reported a Q2 non-GAAP EPS of $0.98, coming in $0.10 ahead of the consensus. While revenue of $696 million, declined by -6% y/y, the results are seen as overall better than expected given what management is calling a “choppy macro environment.” Comparable sales at Famous Footwear were down by -4.3%, but that compares to a -9.4% drop from Foot Locker this past quarter as an industry benchmark.

Caleres is benefiting from the strength of its brand portfolio, with fashion names like “Allen Edmonds,” and “Vionic” sneakers seeing sequential gains in quarterly sales. That side of the business achieved a record gross margin and represents a growth runway amid a positive response by customers to recent style launches.

Company IR

The other important theme is an ongoing deleveraging. Caleres ended the quarter with $244 million in total debt, a level that declined by $47.5 million in Q2 and even $105 million over the past year. Considering the current balance sheet position of $47.1 million in cash and $240 million in adjusted EBITDA over the past year, a net leverage ratio under 1x is a positive in the company’s investment profile.

Keep in mind that Caleres distributes a quarterly dividend of $0.07 per share, which yields a modest 1.1%. The company has also been active with buybacks, repurchasing approximately $14 million in shares in the first half of the year, with 5.6 million remaining under the current authorization.

In terms of guidance, management is targeting full-year comparable sales to be modestly lower, down in the -3% to -5% range from 2022. The adjusted EPS forecast between $4.10 and $4.30, at the midpoint, represents a -7% decline compared to $4.52 last year. Again, facing some of the macro pressures, but otherwise resilient.

Looking ahead, the expectation is for growth to rebound and earnings to accelerate into 2024 as the ongoing strength in the brand portfolio and direct-to-consumer operation supports even higher margins.

Company IR

CAL Stock Price Forecast

The attraction of Caleres is its unique position on this side of “discount shoes” and value brands. The company’s network of 955 retail locations including 861 Famous Footwear stores offer affordable prices that are increasingly seen as a good option for a large segment of the market.

In an environment of high interest rates and broader consumer spending pressures, it makes sense to us that Caleres is capturing the impact of consumers substituting away from more premium labels.

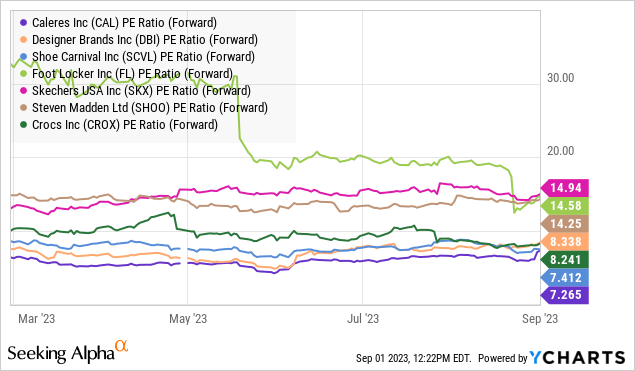

At the end of the day, the key point here is that the strategy and financial execution are working. What we like about CAL is that shares continue to be priced at a discount to peers. Based on the 2023 consensus EPS which is in line with management guidance for the year, CAL is trading at a forward PE of around 7.25x, which is below names like Designer Brands Inc. (DBI) at 8.3x, and even Shoe Carnival (SCVL) at 7.4x.

We bring both of these names up as DBI and SCVL likely represent the closest comps to CAL’s business model, yet have been delivering weaker results. DBI reported comparable sales falling by -10% in its last report. SCVL guided earnings lower. The case we make is that CAL deserves a premium given its more positive outlook and firming financial position.

Final Thoughts

We rate Caleres, Inc. as a buy with a price target of $36.00 representing a 9x multiple on the current consensus EPS for 2023. In our view, a combination of an ongoing balance sheet deleveraging, strength in the brand portfolio, and room for margins to climb can support a structurally higher valuation multiple for the company. With shares approaching their highest level since early 2019, the setup here is for the run to continue.

Covering some of the risks, weaker-than-expected results would likely open the door for renewed volatility in the stock. While we believe there is a defensive aspect to this segment of discount shoes, the company remains exposed to volatile macro conditions.

A sharp deterioration in consumer spending could pressure demand and force a reassessment of the outlook. Monitoring points over the next few quarters include the evolution of the gross margin and underlying cash flow trends.

Seeking Alpha

Read the full article here