One gold miner I have owned off and on during 2022-23, but yet to mention on Seeking Alpha is Alamos Gold (NYSE:AGI). The company has several operating mines in Canada and one in Mexico, with eyes toward new projects and growth initiatives on a number of its properties (including undeveloped assets in Oregon, USA and Turkey).

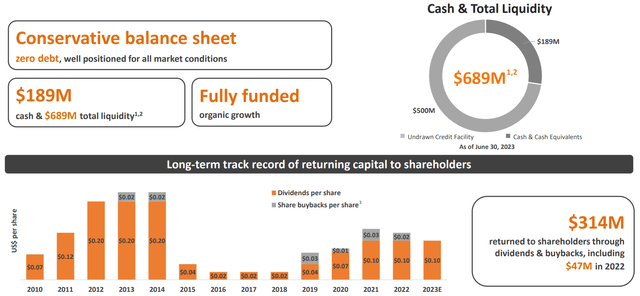

The company is expected to produce around 500,000 gold equivalent ounces in 2023, at AISC expense of roughly US$1175 per ounce. Even better news than its lower-than-average cost structure is the company held zero debt vs. $189 million in cash at the end of June, plus $535 million in current assets vs. $994 million in total liabilities. Per management, the company projects it will fund its drilling for new ore discoveries, while expanding operations by building out infrastructure at both existing mines and new ones, organically from future cash flow generation (using limited amounts of debt).

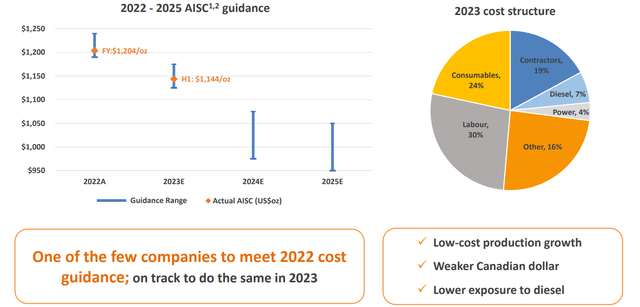

Perhaps the most intriguing part of the Alamos buy argument is its forecast for declining mining costs during 2023-25 vs. 2022. If precious metals continue confounding analysts (forecasting minimal to no gains for gold and silver next year) and rise markedly in price over the next 12-24 months, reported cash flow and income margins could jump faster than other miners, where operating costs have been climbing each year.

On top of this super-positive business setup (requiring no equity dilution and little debt issuance), Alamos has a long history of paying a regular cash dividend each year and buying back shares whenever the gold price is high.

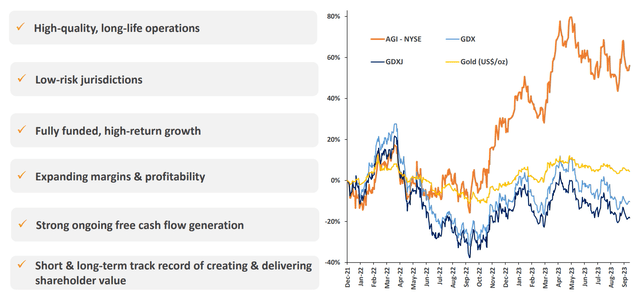

To me and others in the mining investment world, such a combination of low-risk jurisdiction assets, low operating costs, strong free cash flow generation, the return of shareholder capital, and an outlook for decent organic growth over time, are incredibly difficult to find. So, with a valuation on production and reserves that still makes sense for investors (on long-life 20+ years of proven reserves at current mining rates), its share price has proven an industry leader for gains during 2022-23.

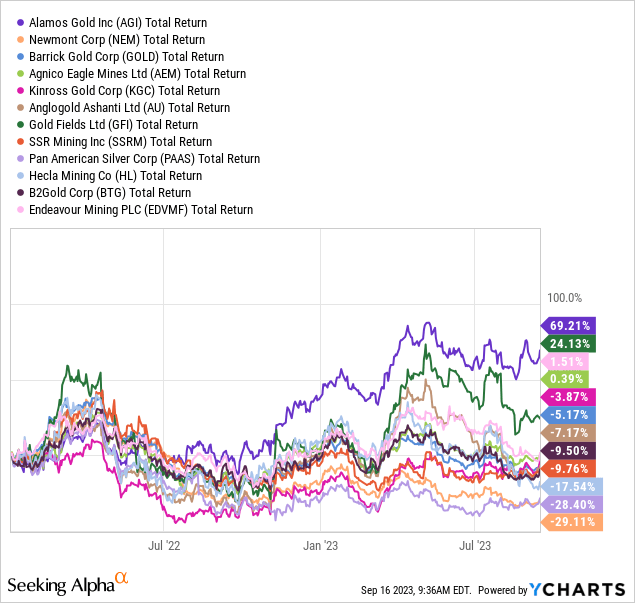

Below is total return performance graph from January 1st, 2022. My peer gold mining group includes Newmont (NEM), Barrick Gold (GOLD), Agnico Eagle (AEM), Kinross Gold (KGC), AngloGold Ashanti (AU), Gold Fields (GFI), SSR Mining (SSRM), Pan American Silver (PAAS), Hecla Mining (HL), B2Gold (BTG), and Endeavour Mining plc (OTCQX:EDVMF).

YCharts – Alamos Gold vs. Mining Peers, Total Returns, Since January 1st, 2022

The Business

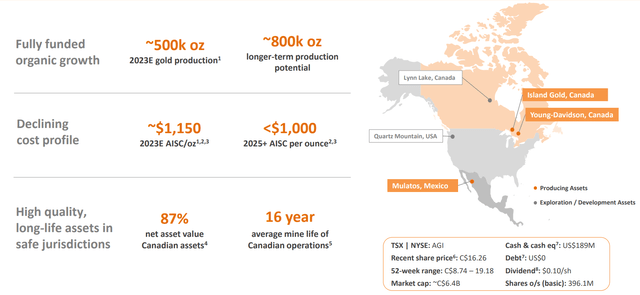

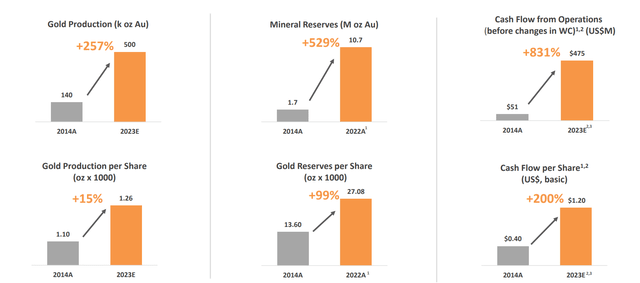

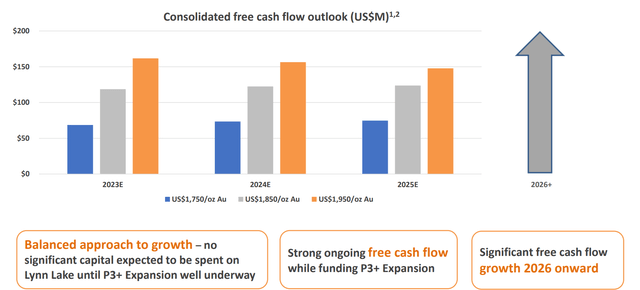

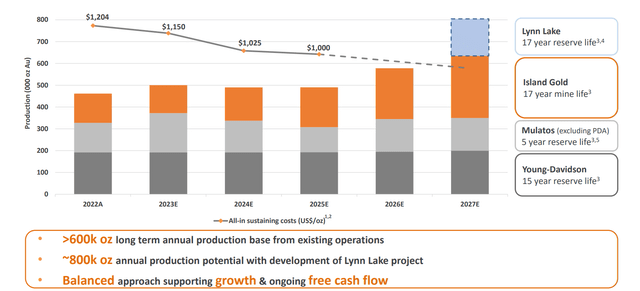

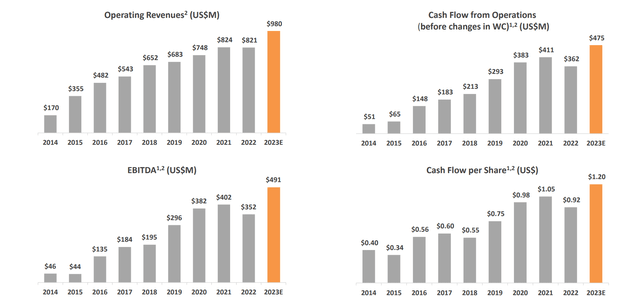

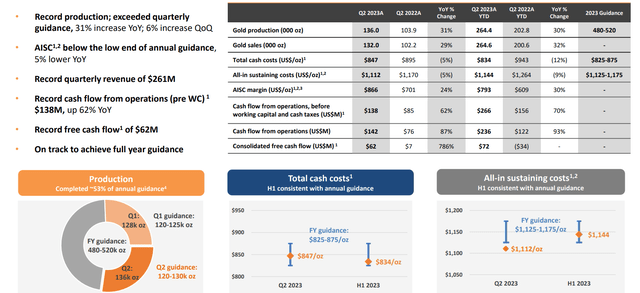

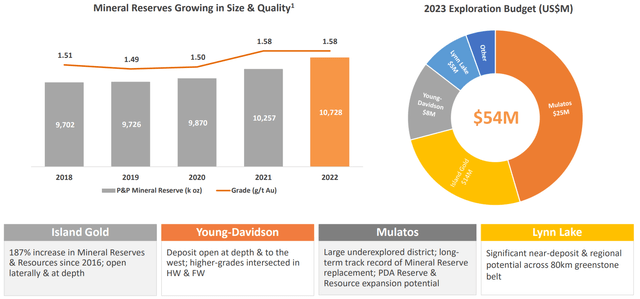

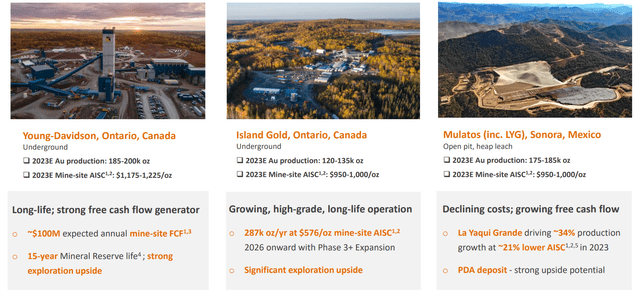

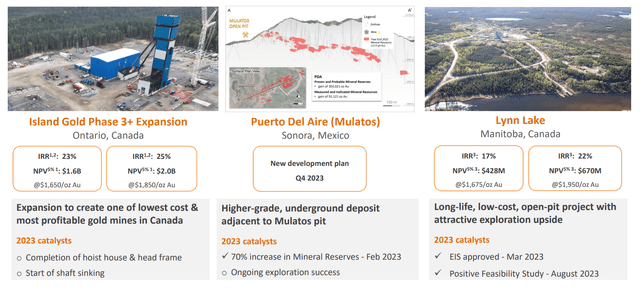

The September Investor Presentation linked here just released days ago gives a terrific overview of operations. I am adding the summary slides I like best for readers to contemplate. (You can find more detailed maps and projections for each mine on this presentation.)

Compared to a gold mining industry struggling to find new resources, where mined ounces aren’t growing at all, and costs continue to bump higher each year, Alamos stands out as a true success story.

Alamos Gold – September 2023 Investor Presentation

Alamos Gold – September 2023 Investor Presentation

Alamos Gold – September 2023 Investor Presentation

Alamos Gold – September 2023 Investor Presentation

Alamos Gold – September 2023 Investor Presentation

Alamos Gold – September 2023 Investor Presentation

Alamos Gold – September 2023 Investor Presentation

Alamos Gold – September 2023 Investor Presentation

Alamos Gold – September 2023 Investor Presentation

Alamos Gold – September 2023 Investor Presentation

Alamos Gold – September 2023 Investor Presentation

Alamos Gold – September 2023 Investor Presentation

Valuation Ideas

Looking forward, I do expect Alamos to remain an average to above-average investment gainer vs. the rest of the gold mining space into 2024. The valuation remains respectable on flat gold/silver metals pricing. So, any big jump in monetary metals during 2024 should support another excellent run for Alamos Gold shareholders.

I would say the stock looks more fully valued than other major mining enterprises in the precious metals sector. In term of a cheap valuation, you will need to look at Newmont or Barrick for a high North American asset weighting at a better valuation. Yet, Alamos’ higher valuation is well worth the price of admission. You are getting an A+ balance sheet, A+ operating mines for life of reserves and location, A+ cost structure per ounce produced, A+ management team, and a B+ growth outlook in one investment security.

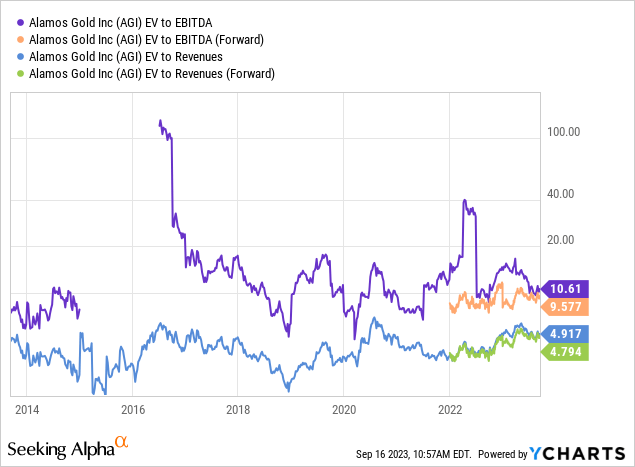

Below I have graphed the enterprise value (including debt and cash held) vs. basic EBITDA cash flow and revenues. My conclusion is shares are trading very close to 10-year averages.

YCharts – Alamos Gold, Enterprise Valuations, 10 Years

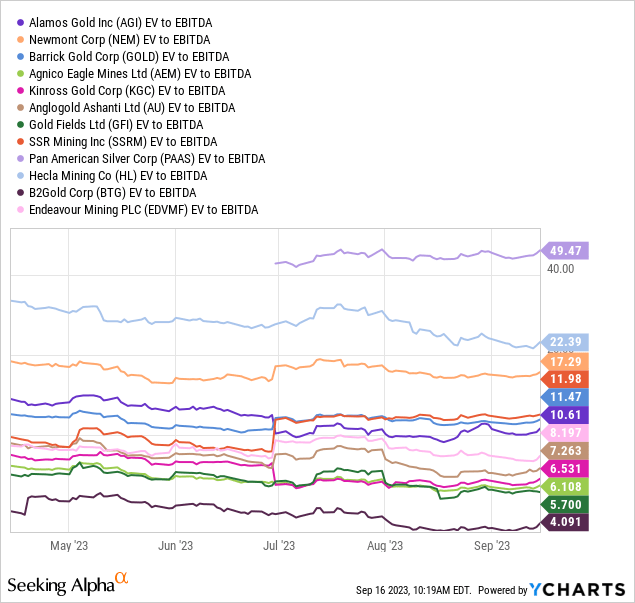

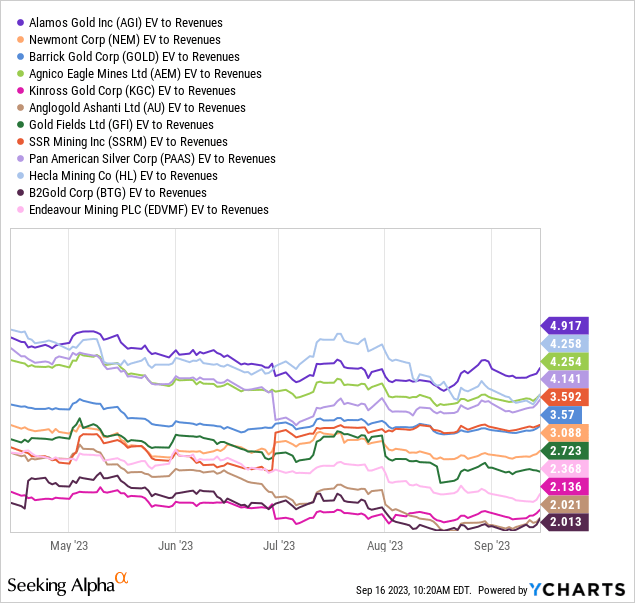

EV to EBITDA of 10.6x stands squarely in the middle of the pack vs. major gold mining peers. In terms of a “trailing” valuation, Alamos appears to be just as good a value as Newmont or Barrick (the difference being the two largest gold miners internationally are suffering from unusual cost increases and one-time issues in 2023). On my second chart, you can more clearly see the EV to Revenue calculation of 4.9x is well above average.

YCharts – Alamos Gold vs. Major Mining Peers, EV to EBITDA, 5 Months

YCharts – Alamos Gold vs. Major Mining Peers, EV to Revenues, 5 Months

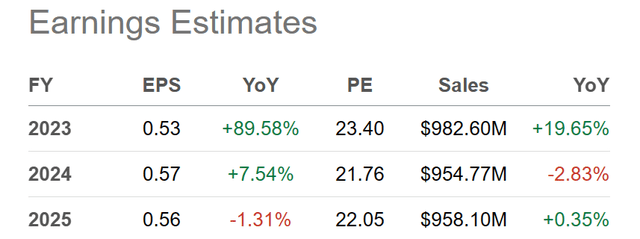

Another minor negative is limited growth is expected from Alamos over the next couple of years for EPS and sales (as production flatlines). Absent a material rise in gold prices in particular, the valuation appears stuck at a P/E in the low-20s (on $0.55 per share in earnings) and 5x sales just under $1 billion annually.

Seeking Alpha – Alamos Gold, Analyst Earnings & Sales Estimates for 2023-25, Made September 15th, 2023

Strong Technical Momentum

For sure, the winning point in the Alamos buy proposition revolves around its performance scoreboard. AGI has been a top precious metals investment over the last few years, plain and simple. If you prefer robust momentum in your investments, Alamos is a top gold mining prospect.

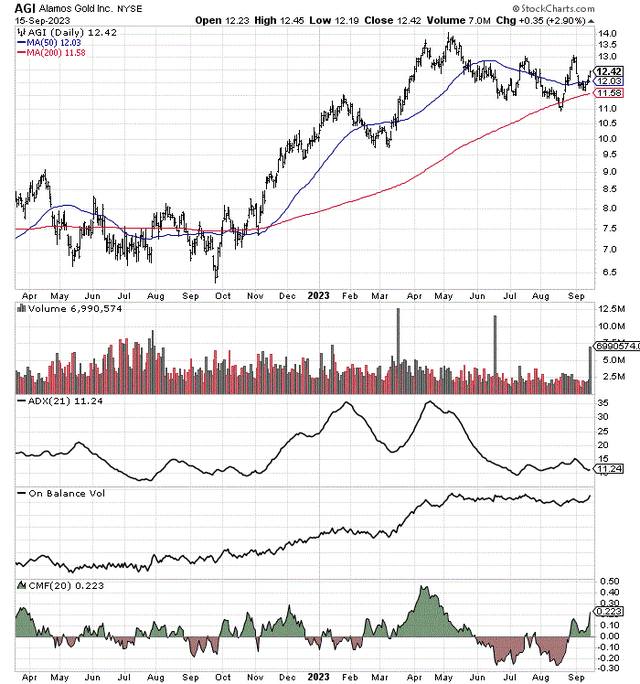

Below is a chart of 18-month changes in daily price and volume. Price has almost doubled its $6.30 low from last September. And, price is again above both the important 50-day and 200-day moving averages.

The 21-day Average Directional Index has been trading between a low 9-15 score for months. The last time such occurred was summer and fall 2022, which proved a terrific time to buy shares on the cheap. When the ADX is low something of a low-volatility balance between buyers/sellers, alongside a constructive basing pattern, are usually the readout.

On Balance Volume readings have been excellent over the whole period. And, the 20-day Chaikin Money Flow indicator has moved into a clear accumulation zone in recent weeks.

StockCharts.com – Alamos Gold, 18 Months of Daily Price & Volume Changes

Final Thoughts

An investment in Alamos may come down to your binary decision on where precious metals pricing is headed. If you are bearish on gold’s direction in particular, I understand if you want to pass on this investment idea.

However, using forward estimates of $2500 and $3000 gold prices in 2024-25 (all other operating variables remaining the same), sales, cash flow, and earnings should move dramatically higher.

For example, using management numbers from the above September presentation (including steady ounces produced, operating costs and taxes), extrapolated to higher price levels, $2500 gold should support EPS of $1.10 and $3000 gold $1.45.

Here are my projected share price ranges, depending on interest rates (investment valuation discount rates) and acceptable prevailing P/Es in the general stock market. At $2500 gold I would expect AGI to trade between $18-$25, and at $3000 gold between $25-$35.

So, considerable upside on investment still exists, assuming gold prices rise substantially in 2024 and 2025.

What’s the downside risk? At $1800 gold, EPS of $0.40 and a share projection of $9 to $10 seem fair to me. At $1600 gold (which is the lowest I can honestly see playing out vs. decades of relative pricing stats I run for underlying gold valuations), EPS of $0.15 alongside a share forecast of $6 to $8 is probable. At that gold price, company worth would become more of a function of price to sales and book value multiples, with a bullish long-term cyclical upturn outlook part of the price equation.

I rate Alamos Gold a Buy under $13, based largely on my upbeat forecast for rising gold prices over the next 12-24 months.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here