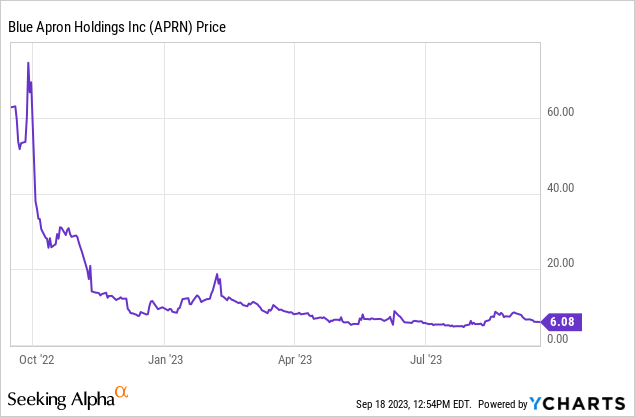

Though 2023 has been unkind to many small-cap companies, laggard Blue Apron (NYSE:APRN) has been able to turn its recent weaknesses around. Under the helm of new leadership, the company has executed a difficult turnaround plan that included shrinking its asset base, reducing its workforce, and raising prices. So far, the results are promising.

Year to date, shares of Blue Apron have declined more than 30%, as investors continue to express concerns over Blue Apron’s declining order trajectory and its ability to survive as a much smaller company. That being said, shares bottomed in early August and have largely rallied since the company’s early August earnings report.

Earlier this year, I upgraded my viewpoint on Blue Apron from a prior bearish view to neutral, citing hope from the company’s sale of its distribution centers to FreshRealm. As a reminder here, Blue Apron is getting out of the manufacturing game, instead selling its production centers to a third party (FreshRealm) in exchange for an immediate infusion of cash to Blue Apron to fund operations and customer acquisitions, and a long-term exclusivity agreement wherein FreshRealm is the sole supplier of Blue Apron meal kits. Though this move may reduce Blue Apron’s ability to achieve economies of scale over the long run, it’s the best way for the company to focus on regaining its customer base and surviving in the near term.

Blue Apron’s latest Q2 updates, which I’ll cover in broader detail in the next sections, provide ample evidence that this strategy seems to be working out. This being said, given a plethora of operational risks going forward, I’m not yet keen enough on this stock to fully commit to buying a position in it. In spite of all the hope raised in the prior few quarters, we still have to watch out for the following question marks:

- Can Blue Apron still turn a profit with the FreshRealm model? Once opex cuts are in place and the company has a few quarters under its belt using its third-party producer, it remains to be seen whether the company is capable of turning a profit and staunching its cash flow bleeding.

- Will price increases alienate more customers than we originally expected? The company boosted prices on its meal kits by roughly $2 per shipment, which has helped to slow revenue declines and improve gross margins. It remains to be seen, however, how elastic customer demand is and if Blue Apron will end up shedding a good chunk of its customer base as a result of these price increases.

All in all, I think Blue Apron remains a “watch and wait” stock. While there are promising business levers at play, execution remains a huge question mark: especially as macro concerns still loom over the economy, including new drivers such as the resumption of student loans that threaten to pinch consumer spending.

Revenue declines moderate, driven by price increases

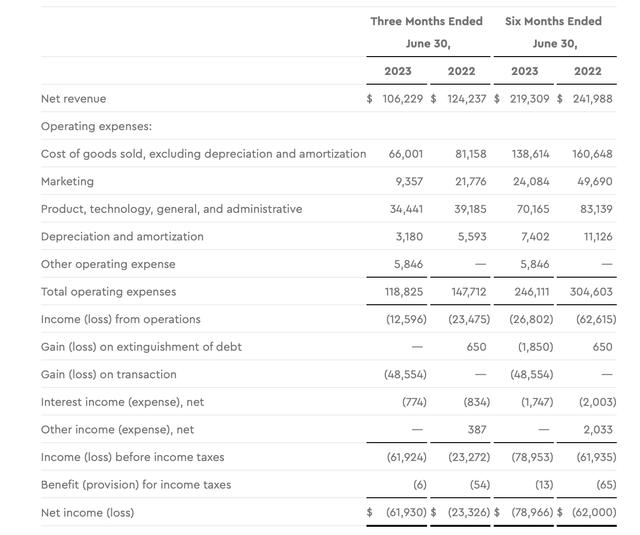

Let’s now discuss some of Blue Apron’s latest quarterly trends in greater detail. The Q2 earnings summary is shown below:

Blue Apron Q2 results (Blue Apron Q2 earnings release)

Blue Apron’s revenue declined -14% y/y to $106.2 million in the quarter. Note that there was a tough compare versus a one-time, $10.0 million bulk sale to an enterprise customer in the second quarter of last year; excluding $10 million from the prior-year revenue base, Blue Apron’s decline would have been only -7% y/y, which is closer in line to Q1’s -4% y/y decline.

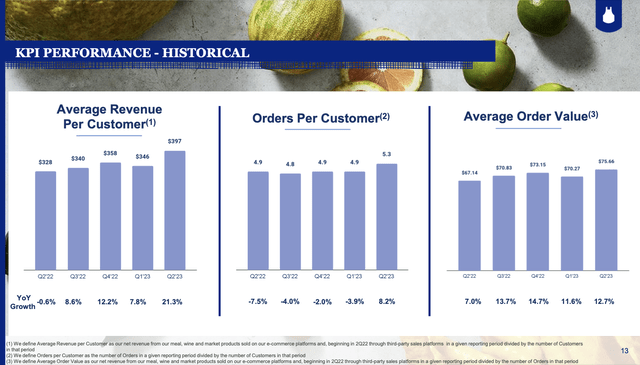

The key customer metrics are shown in the chart below. Average revenue per customer increased 21% y/y to $397 (also up 15% sequentially).

Blue Apron Q2 key metrics (Blue Apron Q2 earnings release)

This was driven by both an increase in order frequency (+8% y/y to 5.3 orders per customer), as well as price increases, which boosted average order value by 13% y/y to $75.66.

Active customers, meanwhile, fell -24% y/y to 267k.

This may be the new reality that Blue Apron can thrive in: a smaller, but more loyal and price insensitive customer base that can make up for lower absolute orders by increasing order frequency and value. And now that the problem of scaling to meet demand falls on FreshRealm, I think this gives Blue Apron a good platform from which to stabilize its business and chase incremental growth opportunities.

Note that order declines and customer attrition was coupled with a -57% y/y reduction in marketing spend (-36% sequentially).

Here is helpful commentary from CEO Linda Findley’s remarks on the Q2 earnings call, highlighting the company’s marketing strategy going forward:

At the start of the year, under the leadership of our new Chief Revenue Officer, we implemented an improved testing program. The goal is that every marketing dollar we invest delivers on our targeted payback period, while also attracting the right customer. With over six months of testing under our belt, we have identified what we believe is the right formula to move to more effectively target the next dollar and all of this is paying off.

In Q2, we saw significant improvement in payback periods at levels far less than our one-year target and efficiencies better than Q1. Cost per acquisition also improved by 30%, while conversion rates improved by 25% year-over-year during the second quarter. In addition, our average weekly retention is the strongest it’s been in five quarters, even with the recently implemented price increase.

We were able to make consistent and repeatable improvements while continuing to leverage our strong brand. Given our success so far and as we capitalize on our new asset-light model, we are increasing marketing slightly in the second half of the year. We plan to stay within our targeted one-year payback period and expect our investments to come to fruition in 2024.”

Cost cuts and breakeven FCF is promising

Though Blue Apron is still suffering from top-line declines, we note that costs are going down faster – on par with the company’s strategy of improving efficiency at a much reduced scale.

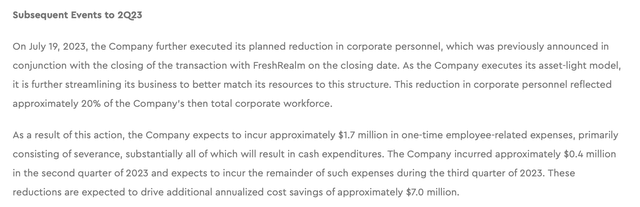

In July, as shown in the snapshot in Blue Apron’s Q2 earnings release below, the company is slashing 20% of its headcount – which should help sequential operating margins going forward.

Blue Apron Q2 opex update (Blue Apron Q2 earnings release)

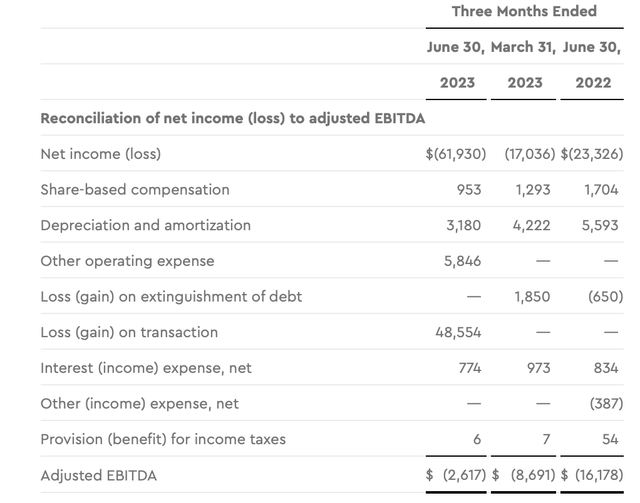

Already, the company’s price increases and new operational model have benefited the bottom line. Gross margins improved to 320bps y/y, which helped the company slim down adjusted EBITDA losses to just -$2.6 million (a -2% adjusted EBITDA margin) versus a -7% margin in the year-ago period.

Blue Apron adjusted EBITDA (Blue Apron Q2 earnings release)

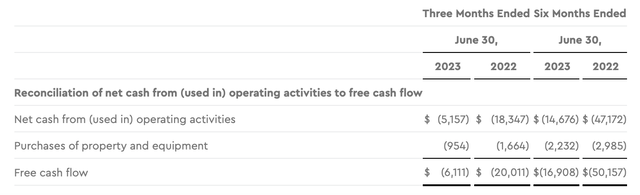

YTD cash burn is also down to -$16.9 million (or an -8% FCF margin), versus a -20% margin in the year-ago period.

Blue Apron FCF (Blue Apron Q2 earnings release)

Thanks to the sale of its distribution centers to FreshRealm, the company is also now debt-free and has $30.0 million of net cash on its balance sheet.

Key takeaways

With a diminishing cost base plus potential revenue upside from price increases once we lap tougher compares, it’s not completely a doom-and-gloom story for Blue Apron – yet at the same time, the company has yet to prove that it can operate profitably at a smaller scale. Keep an eye out on this stock, but don’t rush in to buy just yet.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here