Introduction

Bioceres Crop Solutions Corp. (NASDAQ:BIOX), an industry stalwart in the agricultural landscape, recently unveiled fiscal Q4 EPS coming in at -$0.06 and revenue figures registering at $104.70M. By marking a slight year-over-year decline of 0.99%, the company still managed to surpass market expectations by a notable $2.26M. Parsing these numbers, I uncovered a tapestry of corporate strategies and diversification endeavors.

Central to Bioceres’ offerings is the HB4 technology – a novel solution that has garnered attention not just for its innovative nature, but also for its potential resilience against pressing climatic adversities. Layering in the firm’s expansive set of partnerships and the accompanying regulatory approvals, the data suggests a company that, despite some headwinds, has positioned itself adeptly in a dynamic and challenging market space.

The Good News First

In the complex landscape of crop productivity, Bioceres Crop Solutions Corp. stands out with its multifaceted approach, addressing a broad array of agricultural demands. Tracing back the company’s structure, its operations distinctly bifurcate into three primary segments, each serving a unique purpose.

The “Seed and Integrated Products” division, for instance, acts as the backbone to enhance both crop health and yield. It achieves this through an intricate balance of seed traits, germplasms, and seed treatment methodologies. Parallelly, the “Crop Protection” segment dives into a more protective role, deploying tools like Rizoderma, alongside an assortment of herbicides and insecticides, to shield crops from potential adversities.

Taking a closer look, Bioceres’ HB4 seed technology emerges as a pivotal solution, especially when considering regions like Argentina where drought has become a frequent antagonist. Unfortunately, due to the drought, recent data indicates that farmers should expect to experience the worst soybean harvest in almost a quarter of a century

Fortunately, investors of Bioceres will recall that back in late June of ’22 the U.S. Food and Drug Administration (FDA) cast its meticulous eye over the safety and regulatory particulars of the firm’s drought-tolerant HB4 Wheat, and the results pointed to a definitive end.

Now, some context here is important.

The commercial trajectory of HB4 Wheat in the American market is intertwined with a nod of approval from the U.S. Department of Agriculture (USDA). But before that, the absence of a need for a premarket review or an FDA approval for this wheat variant speaks volumes about its regulatory standing.

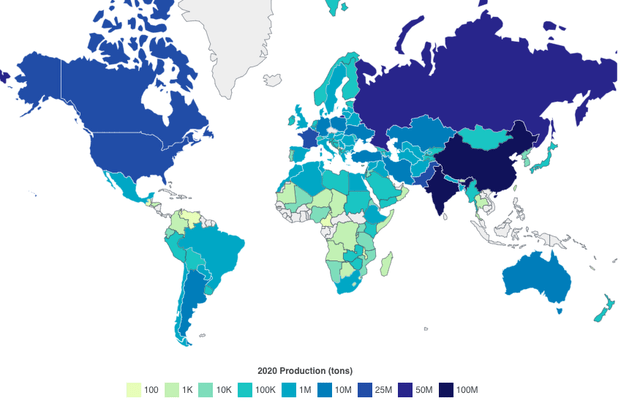

To provide a wider lens on this matter, let’s consider the U.S.’s stature in the wheat marketplace. Positioned as the world’s fourth-largest producer (trailing Russia, India and China) and the third-ranking exporter, the U.S. undeniably sits at a pivotal junction in global wheat trade.

Wheat production by country (tons) (World Population Review)

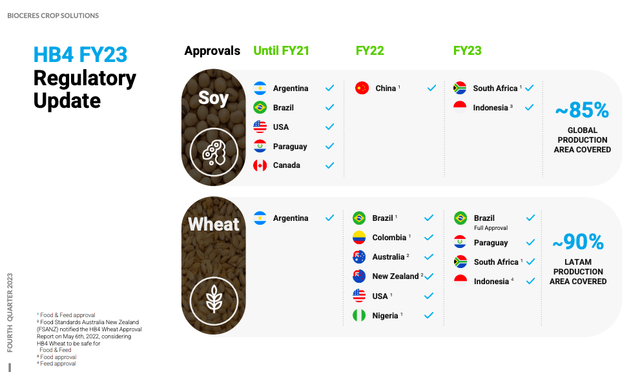

In other words, the FDA’s green light, in this context, acquires added weight when you factor in that HB4 Wheat has already secured approvals in key markets like Brazil, Colombia, Australia, and New Zealand.

Bioceres Investor Presentation

And let’s not bypass Argentina (Bioceres’ home turf), where HB4 Wheat isn’t just a concept; it’s a commercially authorized reality with five unique varieties already in the cultivation mix.

But to truly understand the HB4 technology’s unique proposition, investors need to take a closer look into its functional implications. In regions grappling with water constraints, the technology has demonstrated an ability to bolster wheat yields by an average of 20%, and in some regions over 40%.

For those acquainted with the dynamics of double-cropping systems and their water management intricacies, such a boost is far from trivial. Extend this perspective to no-till farming practices that incorporate HB4 Soy-Wheat rotations, and we’re looking at a significant carbon sequestration potential – an estimated 1,650 kg per hectare per year.

Bioceres Investor Presentation

This not only presents an agricultural breakthrough but also draws a stark contrast to the environmental footprint of traditional soy monocultures.

But the real narrative twist emerges when investors sift through the company’s recent performance metrics.

Bioceres Investor Presentation

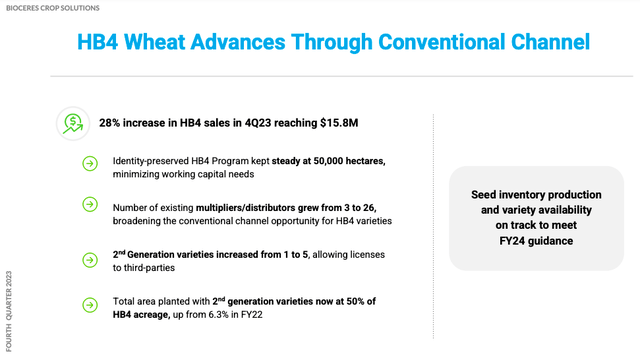

While Argentina’s agricultural sector witnessed a staggering 35% drop in wheat acreage as a result of the relentless drought, Bioceres responded not with retreat, but with adaptation. A significant pivot was observed in their HB4 wheat sales, registering a 28% uptick, rising from $12.2 million to $15.8 million within a quarter.

Expanding Borders

Following Brazil’s regulatory green light, Bioceres undertook an ambitious transition to a broadened base of multipliers and distributors. This strategic shift, which realized an eight-fold surge, has allowed the company to not only streamline inventory costs but also solidify its market stance-keeping them on track for their financial outlook for 2024.

Diving deeper into the specifics of their product portfolio, there’s been an evident shift in their HB4 wheat’s genetic makeup. More than half of its acreage now harnesses the prowess of second-generation varieties. This is particularly noteworthy when you contrast it against last year’s mere 6% footprint.

The ramifications?

This expansive diversification looks poised to make Bioceres an attractive partner for seed companies eyeing licensing opportunities.

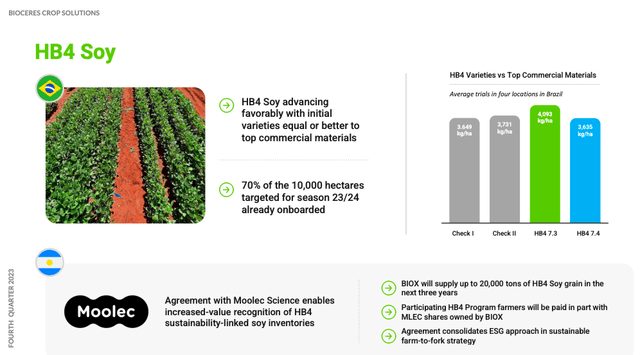

The narrative of success extends to their HB4 soy operations in Brazil. These operations have garnered significant traction, notably with the introduction of high-yield varieties conceived in tandem with TMG. Such strides in innovation echo their upcoming endeavors-Bioceres has blueprints to introduce the cultivation of these varieties across the first 1,000 hectares in the United States, a venture set in collaboration with GDM.

Bolstering their operations further, an alliance with Moolec Science has been carved out, setting the stage for a 20,000-ton supply of ESG-aligned HB4 soy-an initiative that has a financial imprint of around $12 million.

From a macro vantage point, regulatory winds have been favorable. With Brazil and Paraguay’s approvals in their dossier, Bioceres can now tap into approximately 90% of the LATAM wheat hectares-a marked stride from the prior fiscal. This momentum is catalyzed further with Indonesia’s recent endorsement for HB4 wheats.

Their corporate partnerships too speak volumes of their industry stature. An alliance with Corteva Seed Applied Technologies, underscored by the revolutionary MBI-306 biological insecticide, is set to potentially double their European market operations. This move further cements Bioceres’ position in the echelons of biological seed care solution providers.

Projecting forward, the company’s roadmap is dotted with prospective growth corridors. ProFarm’s anticipated revenue surge, married to the expanded biostimulant lineup and the MBI-306’s entry into the U.S. and Brazil markets, casts a positive shadow on future profitability matrices. Other operational milestones in the offing encompass the Moolec pact, the inauguration of a novel Brazilian facility, and potential resurgence from Argentina’s climatic adversities-each of these poised to invigorate domains like micro-beaded fertilizer offerings.

Seeking Alpha

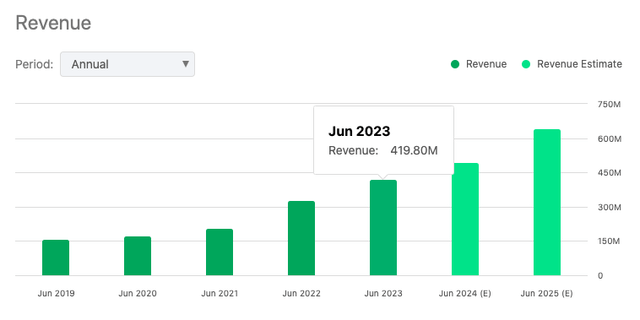

To put their fiscal health into perspective, the full-year comparable revenue hovers at a commendable $420 million-a 25% uptick from the preceding fiscal year, even against the backdrop of meteorological challenges in pivotal markets. Fiscally speaking, there’s been a gross margin evolution from 40% to 44% in fiscal ’23, with the gross profit trajectory surpassing sales growth.

Performance

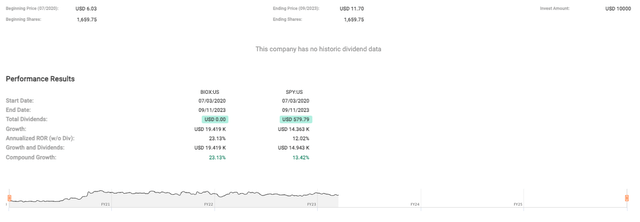

On the performance front, BIOX has made some significant strides within the last few years (see data below) with its stock price growing by a nearly two-fold increase.

Fast Graphs

To put this into further perspective, by juxtaposing BIOX’s performance with the S&P 500 Index, its growth, excluding dividends, is pegged at a compelling 23.13%, outshining the benchmark’s 12.02% by a wide margin.

Seeking Alpha

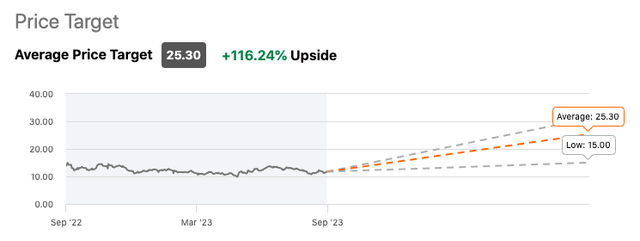

And, as far as Wall Street is concerned, it’s exceptionally bullish on the stock as indicated by coverage from 5 analysts who have an average “Strong Buy” rating on the stock with sights set on anticipation for the shares to more than double.

Let’s Talk Growth… and debt

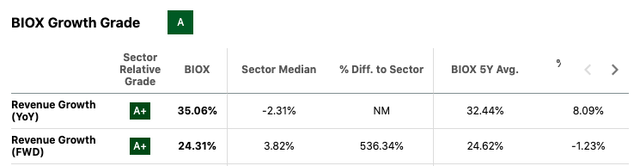

To start, Bioceres’ Growth Grade, sitting at an “A,” indicates the company is outpacing many of its peers within its sector. The higher than average Revenue Growth for the firm, both in terms of Year-on-Year (YoY) and Forward (FWD) rates, at 35.06% and 24.31% respectively, reflects the company’s strong ability to drive top-line growth. It’s particularly impressive to note that the YoY revenue growth outpaced its own five-year average, hinting at an acceleration in its growth momentum.

Seeking Alpha

Now, let’s talk about the elephant in the room. Operating Cash Flow’s “D” grade is a red flag with a -38.83% YoY growth, suggesting, without context, that there may be underlying operational issues.

Seeking Alpha

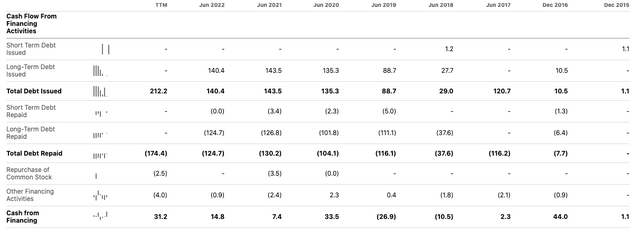

On that note, yes, the company has leaned heavily on debt as its primary financing mechanism with fairly substantial figures in “Long-Term Debt Issued’ showing the company’s aggressive borrowing behavior.

Seeking Alpha

However, they’ve also been diligent in repaying this debt, suggesting a healthy and sustainable tactical approach to financing – borrowing when necessary, but also being responsible about managing the debt load.

Seeking Alpha

The exponential growth in Working Capital and CAPEX, with YoY rates of 183.27% and 141.69%, respectively, reflect Bioceres heavy-handed investing in its operations, which explains the aforementioned dip in operating cash flow which is normal for a company in an aggressive expansion mode.

Valuation

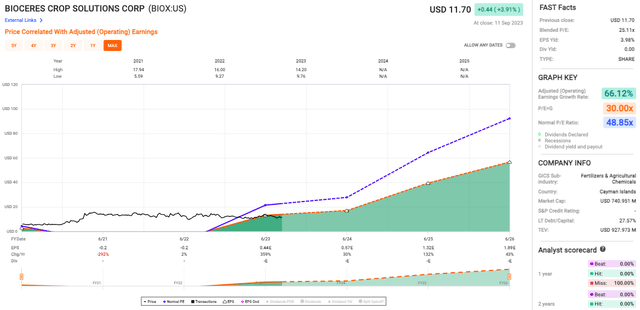

Bioceres’ phenomenal Adjusted (Operating) Earnings Growth Rate of 66.12% (see chart below) is nothing short of remarkable and further underscores the message that the firm is prudently managing its finances by indicating a healthy operational efficiency.

In other words, this growth rate outpaces many of its contemporaries and suggests that the company is leveraging its assets, technology, and operations in ways that are translating into tangible financial results.

Fast Graphs

One key facet that investors shouldn’t overlook is the Blended P/E of 25.11x which demonstrates that Bioceres, despite its operational successes, might be undervalued and suggests that the market might not be fully recognizing its intrinsic value. The potential for upside becomes even more apparent when we juxtapose the P/E with the P/E=G of 30.00x.

Risks & Headwinds

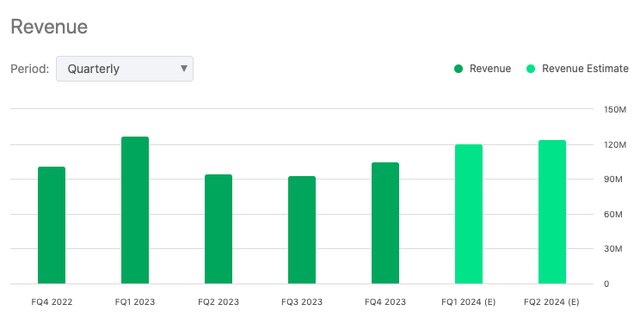

Up until this point, the overall picture has been good, and I hate to rain on the parade, but the recent financial data shows that the company’s revenue trajectory has remained relatively static, especially when benchmarked against the prior year.

Seeking Alpha

Even more indicative of the company’s fiscal posture is the 9% contraction on a pro forma basis. To add a layer of context, this revenue pattern persists when examining the fourth quarter figures, underscoring consistent revenue challenges.

Turning to Bioceres’ engagement with Marrone Bio Innovations, rebranded as ProFarm, there’s a significant subplot unfolding. According to management, the acquisition of ProFarm, which wasn’t in an optimum financial state at the point of purchase, has posed integration challenges for Bioceres. While there was a discernible optimism regarding ProFarm’s future direction, current sales figures might suggest there’s more ground to cover for the company to tap into its full potential.

Lastly, further insights can be gleaned from the performance of Bioceres’ Seed and Integrated products sector. Marginal contractions have been evident when juxtaposed against prior comparable periods. And while the company’s financial statements do highlight a positive shift in SG&A expenses, this is somewhat overshadowed by other operational costs identified within the quarter. These combined financial components, when factored with sub-optimal joint venture results, have resulted in an EBITDA decline of approximately $1.4 million on a year-over-year basis.

Rating: Buy

Based on the data, it seems evident that Bioceres showcases robust operational capacities and has forged noteworthy strategic alliances. A significant emblem of their prowess is the rollout of their HB4 technology, which has found particular resonance in locales battling severe water shortages. Even in the face of these unpredictable weather patterns, their revenue arc has persisted in an upward direction.

That said, their meticulous handling of debt, coupled with substantial cash flow directed at operations, paints the picture of a company with a calculated growth roadmap. On the topic of their recent ProFarm acquisition, it’s worth mentioning to potential investors the importance of closely monitoring the transition, given some static revenue figures and potential integration hiccups.

But overall, I believe there’s some undervaluation at play, suggesting there’s potential for stock appreciation. As with any investment, risks linger in the shadows; yet, given the compelling growth prospects and the firm’s innovative prowess, investors might consider this a compelling addition to a forward-looking portfolio.

Read the full article here