Baytex Energy (NYSE:BTE) has acquired Ranger Oil (ROCC). The deal cost $2.4 billion (roughly) for about 162K acres. This comes out to be roughly $15K an acre. Meanwhile, there are competitors out there paying $50K or more for decent Eagle Ford acreage while extolling all the infrastructure and midstream assets they are getting for paying that much. Baytex got all that while paying a rock bottom price.

More importantly, the market values acreage that the company controls. Baytex previously was an investor in acreage in the Eagle Ford that Marathon (MRO) operated. The market tended to discount the value of this acreage. But that is likely to change now that management has a sizable position that it operates with a large working interest. This fits the market idea of what acreage should be like.

Rising oil prices are improving the deal considerably because more cash now from higher oil prices is worth a lot more than cash down the road. Finances could improve faster than originally guided as a result.

More importantly, the additional acreage gives the company much needed light oil production with which it can count on the cash flow during cyclical industry downturns. Oftentimes, the heavy oil pricing discount to light oil widens during downturns. This necessitates the shutting down of production to lessen negative cash flows until prices begin to recover. Baytex can afford those shutting down periods if it has a cash flow source from a more premium product.

The whole situation is likely to result in a higher corporate valuation for Baytex because the heavy oil business (upon which the company is founded) is not considered as valuable as the light oil business. The profitability of the heavy oil business is far more volatile due to the discount issues of heavy oil. Reshaping the company as a more traditional light oil producer is likely to produce a higher market valuation for the company.

The current quarter will not mean much going forward, as the acquisition of Ranger oil was material to the company. There are now far more shares outstanding, and production is going to be taking a large jump with the production mix now weighted heavily towards light oil with a lot of Eagle Ford production as part of that light oil production. This Canadian company stands to get more than half of its cash flow from the Eagle Ford business in the future.

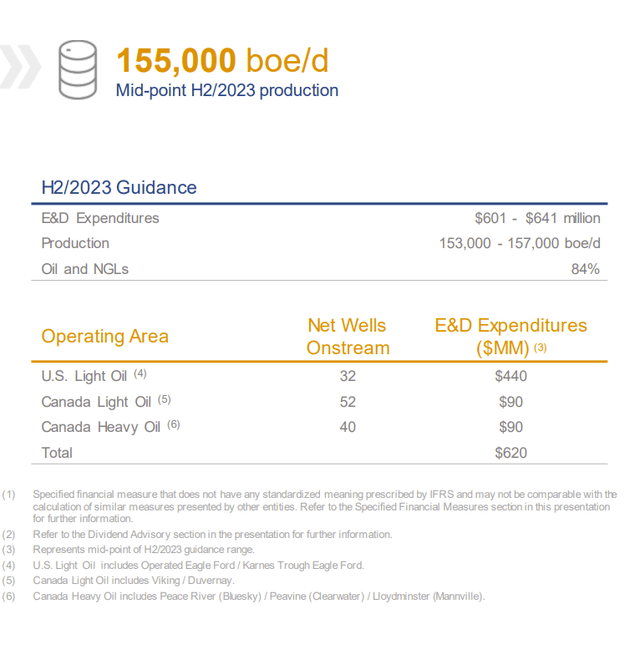

Baytex Energy Production Guidance (Baytex Energy July 2023, Corporate Presentation)

Baytex Energy Post Merger Production Guidance (Baytex Energy Corporate Presentation October 2023)

Production is about to take a big jump from the previous guidance in the 80K BOED range to the guidance shown above. That jump is entirely due to high margin Eagle Ford oil.

What the market appears to not expect is the effect of the profitability of the Eagle Ford acreage combined with rising oil prices. The Eagle Ford is one of the more profitable basins in North America. Rising oil prices are “icing on the cake” and a welcome variance from acquisition assumptions.

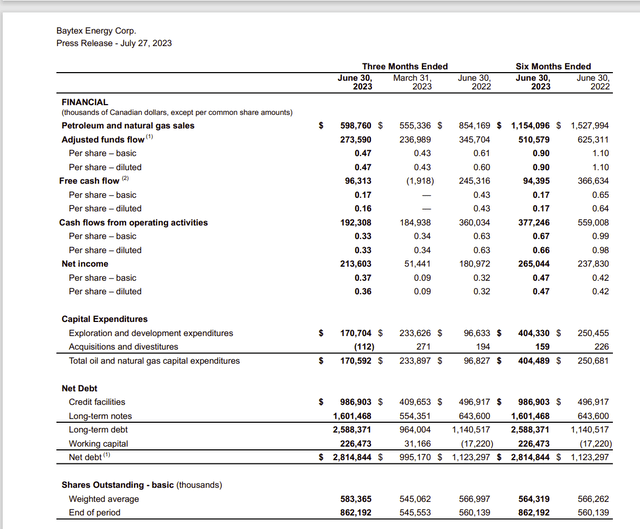

Baytex Energy Summary Of Operations And Earnings Second Quarter 2023 (Baytex Energy Second Quarter 2023, Earnings Press Release)

Now, light oil earnings are less volatile than heavy oil earnings. Therefore, during current times, heavy oil can earn a very good return. But much of the legacy oil business (not including Clearwater) may not make any positive cash flow during a cyclical downturn. The result is that the Eagle Ford is likely, on average, to contribute more than half of the company cash flow throughout the business cycle.

Note that the shares outstanding did not double. Therefore, there is a good chance that this transaction was accretive enough for investors to see a greater free cash flow per share as well as more cash flow from operating activities if oil prices remain in the same range as the second quarter. Since oil prices are rising and most shareholders check right after an acquisition, management could look like geniuses due to the rising oil prices.

Should oil prices stay strong and rise higher, it would be a good question as to the results because heavy oil profitability often exceeds light oil profitability during the peak periods of the boom part of the business cycle. The low-cost Clearwater Play further “muddies the waters”. Overall, it does look like management has a “win-win” situation where shareholders will benefit no matter the outcome.

The other consideration is that the cash flow per share annualized is approximately one-third of the stock price. Given that the acquisition was likely accretive under a wide variety of industry scenarios, that valuation is extremely cheap for a company that is likely to show positive comparisons for at least a year (and has excellent organic growth prospects).

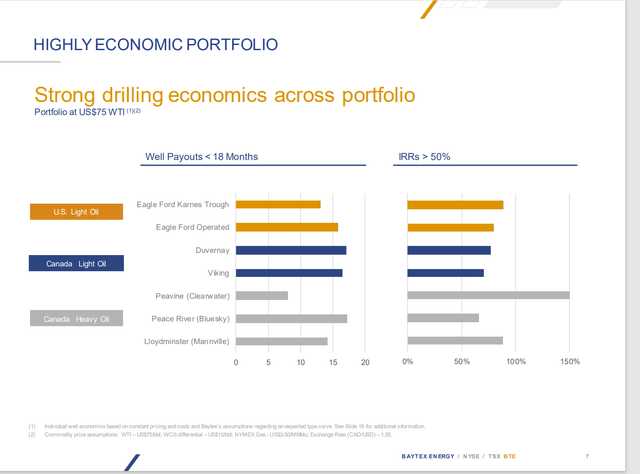

Baytex Energy Payback Periods By Acreage Locatio (Baytex Energy Corporate Presentation October 2023)

In the current industry environment, the heavy oil Clearwater Play is the fastest payback and the most profitable acreage. Throughout the business cycle, the most profitable acreage is likely to be the Eagle Ford operated by Marathon followed by the rest of the Eagle Ford.

What makes things even better is that the assumption for the chart above is a WTI oil price of $75. Oil is actually considerably above that price at the current time, which will raise the ROI significantly of any wells coming on production now.

As a side issue, there could be upside potential to the acquired acreage, as Marathon is one of the best operators in the business. Baytex could use the knowledge gained through the Marathon partnership to improve the payback period on its operated acreage. Should that happen, there appears to be considerable profitability potential, shown by an improving payback period.

The other heavy oil properties have higher breakeven points than the light oil plays (as a rule) or the Clearwater Play. So, while they are often more profitable or as profitable in the current environment, they have to be considered high cost during any downturn because the discount to light oil can widen which can cause the breakeven price based upon WTI pricing to rise.

Debt Considerations

Baytex is a Canadian company that reports in Canadian dollars.

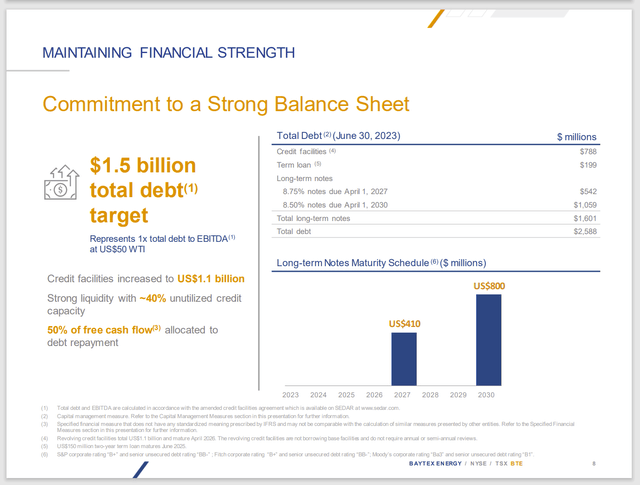

Baytex Energy Debt Structure Detail (Baytex Energy Corporate Presentation October 2023)

That makes the debt structure very interesting. In the accounting world, for reporting purposes, everything has to be reported in the Canadian dollars that the company uses for annual and quarterly reporting.

But there appears to be enough Eagle Ford production to properly service the debt with United States dollars earned. Therefore, the only gain that will matter is the “net” conversion of United States dollars to Canadian dollars after the servicing of the debt from Eagle Ford earnings happens. That may differ from gains and losses reported due to timing issues. We will have to see how this actually works out.

The company may also hedge any actual interest rate risk as well as currency conversion risk. These kinds of hedges are not usually on the balance sheet. But they certainly can influence profits reported when they settle.

On the other hand, it appears that the debt ratio will be low enough that the company can go shopping for another bargain if it chooses to do so. There are a lot of sellers out there that were hoping to “make a killing”. Instead, they ran into the 2015-2020 period, which began with an oil price crash and ended with a pandemic. There was not a lot of encouraging news in-between, either. At this point, there are a lot of disappointed sellers that want out. This company appears to be in the right place at the right time with a decent balance sheet.

Summary

Baytex Energy began as a Canadian heavy oil company. That is no longer the case.

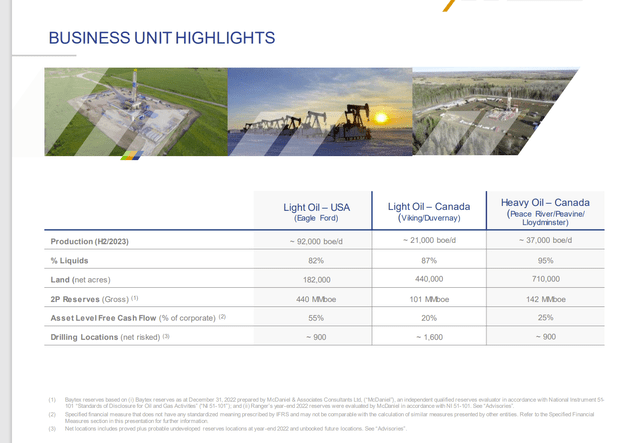

Baytex Energy Business Unit Summary (Baytex Energy Corporate Presentation October 2023)

The majority of production (and likely earnings as well) will come from the Eagle Ford, which produces mostly Light Oil. This company now has the majority of its business in the United States, as shown above. It also has a NYSE listing.

Even though it is organized in Canada, the company could become recognized as a United States company and acquire valuations similar to other United States companies. Canadian companies often trade at a discount to the United States competition. That discount could well disappear in a case like this.

Furthermore, the company has a strong presence in the emerging low cost (and extremely profitable) Clearwater Play. That could turn the company into a market favorite at some point. Nothing succeeds like a lot of cash profits, and Clearwater appears to be able to generate those cash profits in the future.

The company clearly has a lot of upside potential and not much downside. It is probably a strong buy consideration due to the exposure to some very profitable plays and the low market valuation of the stock. Baytex is going to be a very different company in the future than it was in the past. But management is clearly growing in areas that it has a lot of experience with. That does limit downside risk considerably.

Read the full article here