Co-authored by Treading Softly.

America has long been home to a long list of inventors or unique innovations. Becoming an entrepreneur holds a special place in American culture as a way to achieve the American Dream. Innovations of all sorts and kinds frequently crop up, from the mundane to the exquisite. If you’ve ever talked on a cell phone or turned on a light bulb, you’ve enjoyed some of America’s unique innovations.

We often like to imagine innovators and inventors as being extremely quirky or unusual individuals who view the world in a completely different light. Sometimes, the greatest innovations come from the simplest places. The man who invented and patented the intermittent wiper blade system had to fight the big automakers for years to be paid correctly for them using his intervention.

In modern days, most inventors who create companies for their startup projects receive funding through venture capital firms. These will be wealthy individuals who believe in the project and inject them with cash so they can also get a payoff if it succeeds down the line – a small amount of money now for a large payoff later.

When it comes to the market, you can invest in companies that do this sort of venture capital investing and receive strong income from them. Some of these companies will do it within the equity level; others will provide loans or capital with interest requirements so that they can help these startups start but also have a little bit more protection than just handing them money.

Today, I want to look at one opportunity that engages in this type of activity and has a management team that has demonstrated competence in being picky while also being successful with their investing.

Let’s dive in!

Be Picky, Get Paid Long Term

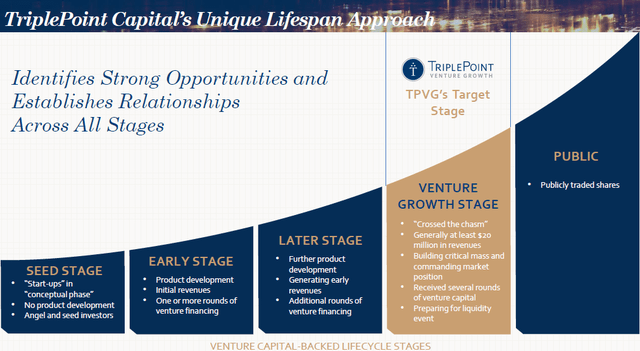

TriplePoint Venture Growth (NYSE:TPVG) is a BDC (Business Development Company), yielding 15%, that focuses on venture-backed companies. Typically, TPVG looks to lend to companies that are in the latter stages of the venture capital cycle. They are looking for investments that could see a liquidity event, like filing for a public IPO or being acquired by a larger competitor within 1-3 years. Source.

TPVG Q2 2023 Presentation

The venture capital sector saw several headwinds early in the year, including rising interest rates, poor IPO conditions, and the failure of Silicon Valley Bank, which was a popular bank among venture capitalists and startups. As a result, plans for going public were put on the back burner.

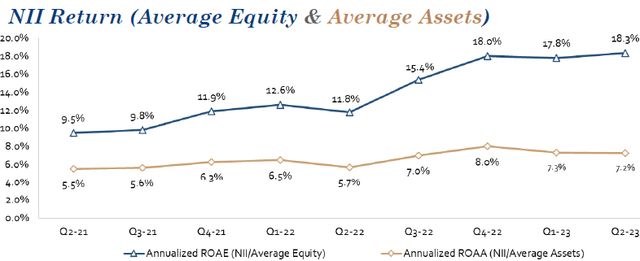

From an earnings perspective, TPVG has benefited. TPVG owns floating-rate loans and has predominantly fixed-rate debt. It has seen its return on average assets and return on average equity go up considerably over the past year.

TPVG Q2 2023 Presentation

On the other hand, many of these businesses started experiencing the strain of higher interest rates and the need to raise more capital at a time when venture capitalists weren’t eager to provide more cash.

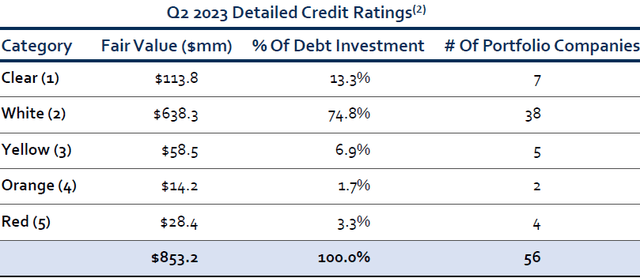

TPVG had a few portfolio companies file bankruptcy, and as a result, wrote down the fair value of the companies. While the majority of TPVG’s investments are doing well, six investments are in their “orange” and “red” categories, which suggests a risk of capital loss.

TPVG Q2 2023 Presentation

Management addressed these troubled companies during the earnings call:

“Although these credit developments impacted NAV this quarter with VanMoof and Health IQ representing approximately 70% of the NAV reduction, we expect some of these situations such as VanMoof, Luko and Underground to be resolved over the next 3 to 6 months, while the others have time for recovery as our teams manage through these situations.”

The VanMoof situation has seen some resolution, as the brand was bought out of bankruptcy. As a first-lien secured lender, TPVG will see some recovery from that. We will have to wait until earnings to learn how large the recovery was, as the acquisition price was not disclosed. Health IQ filed for Chapter 7 bankruptcy, which means that the assets will be liquidated.

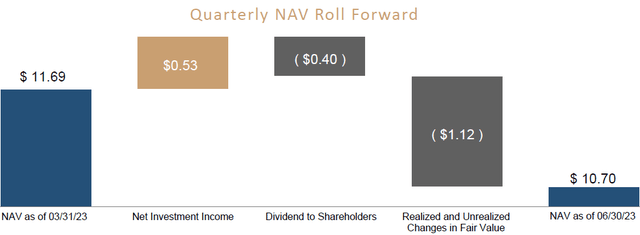

TPVG management will likely update on all of these situations at Q3 earnings in November. As these situations are resolved, TPVG will free up the recovered capital to reinvest elsewhere or reduce debt. Baked into TPVG’s current $10.70 book value are over $80 million in credit losses.

TPVG Q2 2023 Presentation

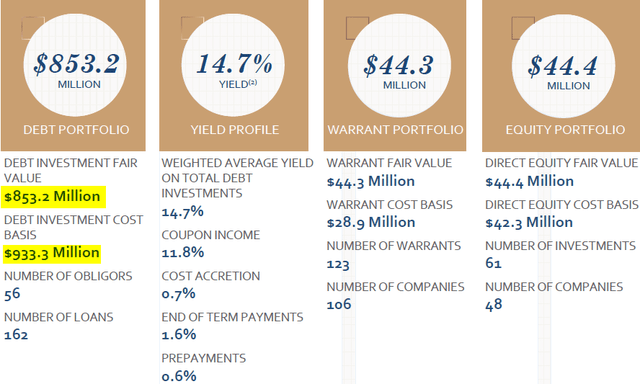

In the next couple of quarters, we will find out if realized losses are that large. However, that is not the entire story for TPVG; GAAP accounting rules treat the valuations unequally. Debt investments need to be written down in value when recovery is uncertain, and that is what TPVG did. However, TPVG also has a $44 million equity portfolio, and TPVG is not allowed to write up the value of its equity portfolio.

The BDC strategy is to provide a debt + equity investment. The logic is that lending to these startup companies is a risk, and some will fail, while others will thrive. The debt investment provides recurring interest income but will come with some credit losses. The equity investments can provide significant upside potential, a potential that can meet or exceed any credit losses.

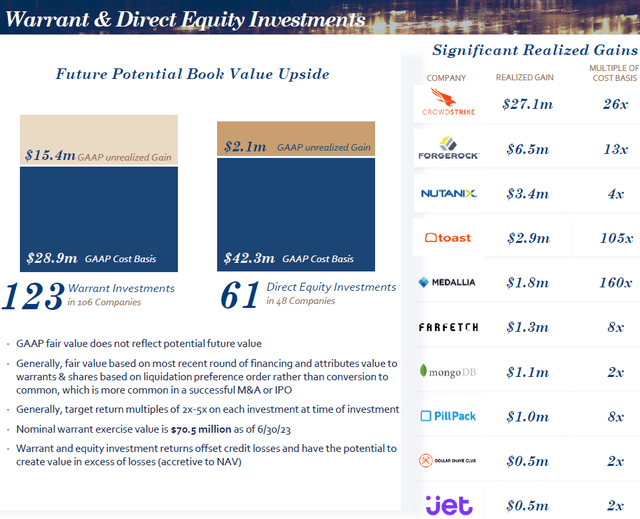

TPVG has a Warrant portfolio that is carried at $44.3 million but has a nominal exercise value of $70.5 million. Its equity portfolio is carried at $44.4 million, but TPVG has seen numerous equity positions get monetized anywhere from 2-160x their cost basis.

TPVG Q2 2023 Presentation

The entire business plan behind a BDC is that gains from these portfolios will help offset realized credit losses. Those gains generally don’t happen during the same quarter as credit losses.

TPVG has covered its dividend with NII (Net Investment Income), and NII, in excess of its dividend, increased NAV by $0.13 last quarter. The decline in NAV was entirely due to the write-down of distressed investments.

TPVG Q2 2023 Presentation

NII remains high and should continue to easily cover the dividend and be a positive for NAV. NII is a constant quarterly benefit, while large write-downs are a lumpy one-time loss.

TPVG will see its NAV recover as NII exceeds the dividend if any recoveries are larger than expected, and when some of their portfolio companies start to IPO again.

Right now, we have the opportunity to buy TPVG at a price that is only a slight premium to the last reported book value. I’m happy to buy and collect my double-digit yield while waiting for the impact of recent credit losses to fade and realize the benefits when TPVG starts seeing gains in its equity portfolio again.

Conclusion

With TPVG, We have a management team with a proven track record of creating value by being highly selective. Earlier this year, we saw major regional banking firms collapse because of their loan books and their assets not matching up in duration; this created an opportunity for companies like TPVG to step in and provide funding for startups but also caused some of those same startups to fail. As this works its way through their books, we can enjoy double-digit yields while other investors avoid them unnecessarily.

I strongly believe that America will continue to be a home of rapid innovation. New ideas are cropping up all the time, and companies are stepping up to solve problems that consumers have. Higher interest rates typically slow the investment in innovation but that will not last forever. Therefore, while others are avoiding this sector, I’m going to step in and lock in strong double-digit yields on the money that I’m investing because I know interest rates will fall again, and there will be an uptick once more innovation occurs.

When it comes to my retirement, I want to be able to help fuel innovation across America while earning a strong income from doing so. There’s nothing better than seeing a company succeed and also knowing that my money is going to be earning an outstanding return from them doing so. In essence, I’m helping fuel the American dream, and to me, there is nothing better than that.

That’s the beauty of my Income Method. That’s the beauty of income investing.

Read the full article here