The future is not just about startups but stay-ups; anyone can start but it takes those who can stand the test of time to stay relevant.”― Bernard Kelvin Clive

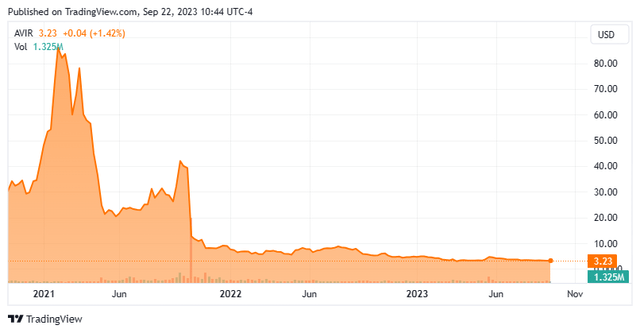

Today, we put Atea Pharmaceuticals, Inc. (NASDAQ:AVIR) in the spotlight for the first time. This small biotech is deep in ‘Busted IPO’ territory and hoping its late stage Covid treatment candidate is still relevant as the pandemic has faded from the headlines. The stock is selling for substantially less than the $5.75 a share takeover offer it received in May of this year and rejected it should be noted. An analysis follows below.

Seeking Alpha

Company Overview:

This clinical stage biotech firm is headquartered in Boston, MA. The company is focused on developing and commercializing antiviral therapeutics for patients suffering from viral infections. The stock currently trades for just north three bucks a share and sports an approximate market capitalization of $265 million.

August Company Presentation

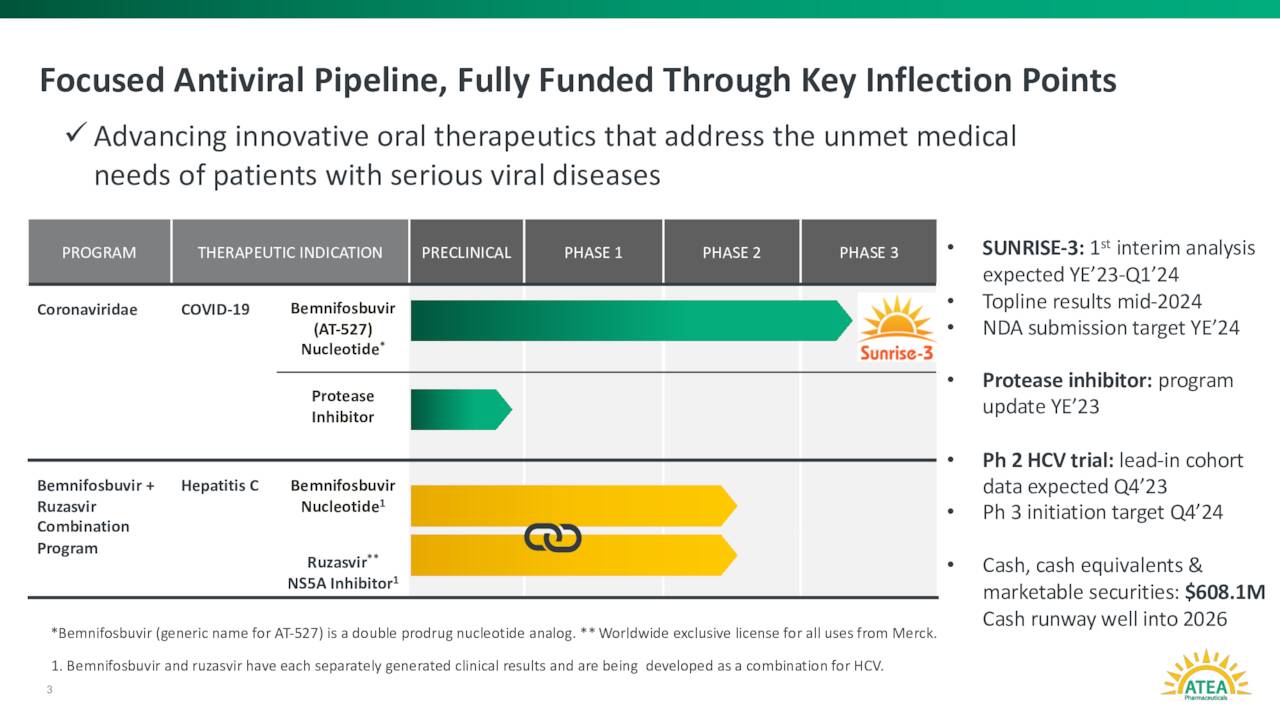

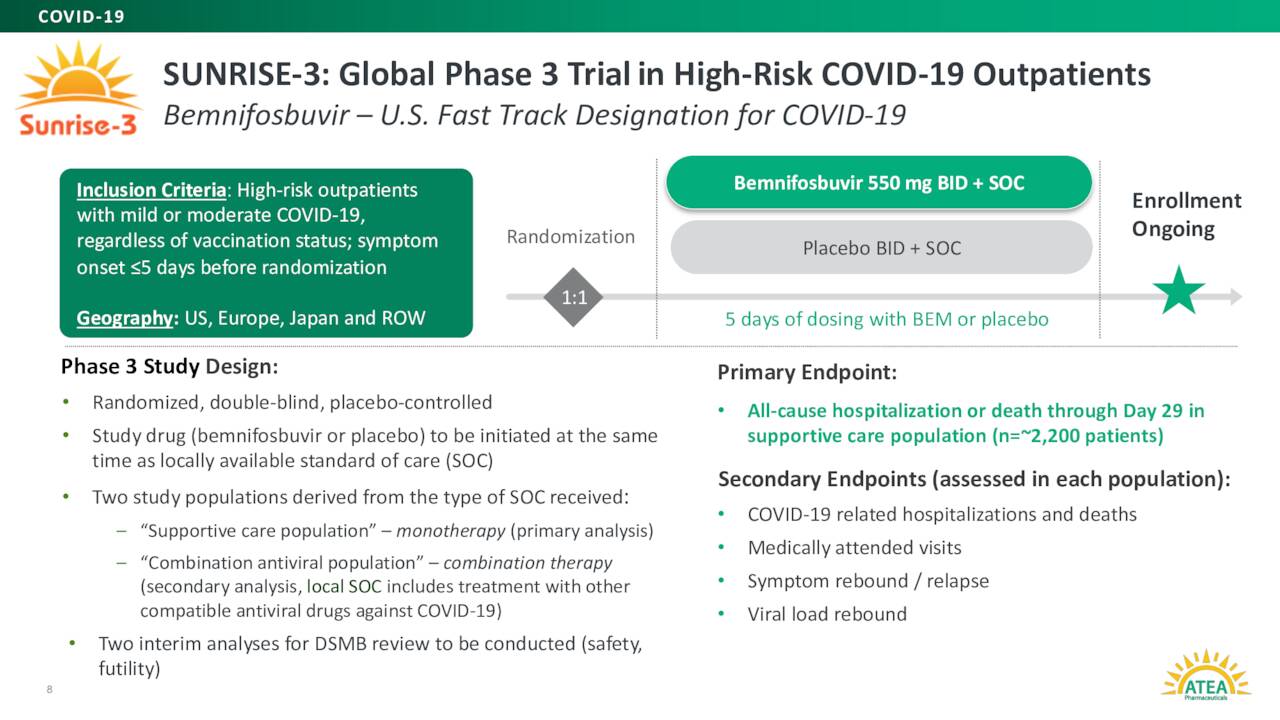

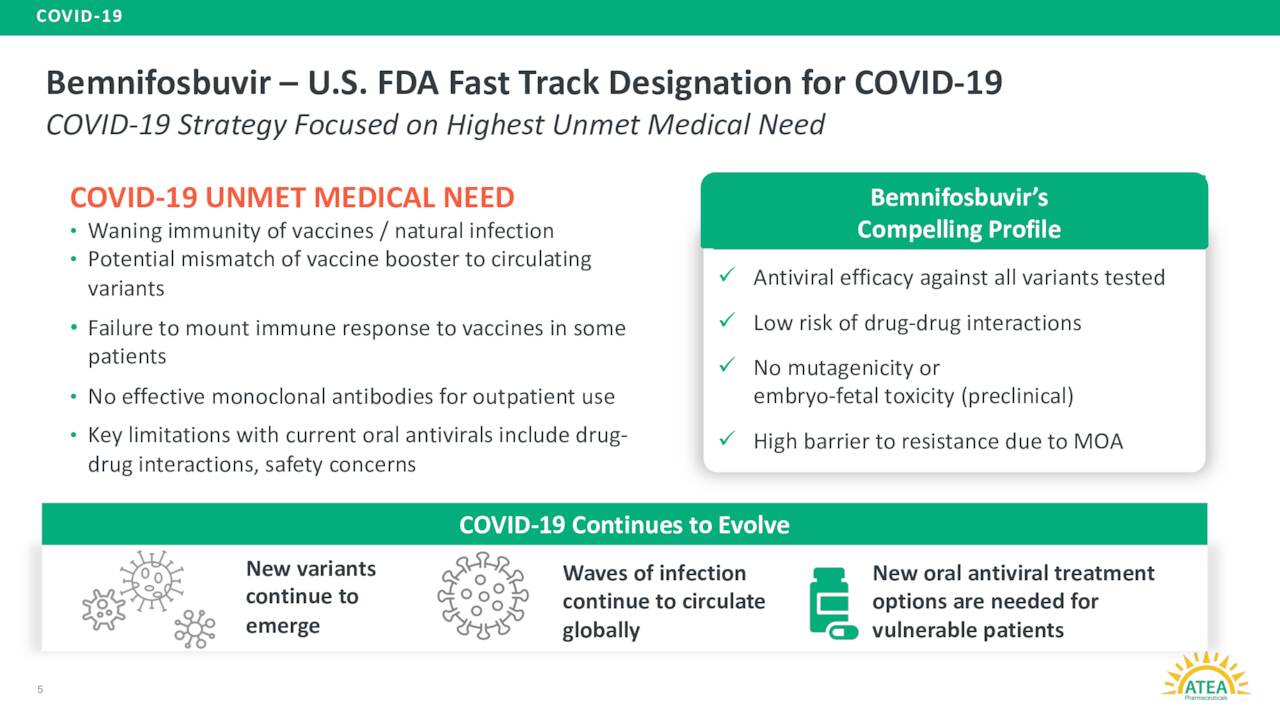

Atea Pharmaceuticals’ lead product candidate is dubbed AT-527. It is an oral antiviral candidate. This candidate is also known as Bemnifosbuvir and is designed to inhibit viral replication by impairing viral RNA polymerase, a key component in the replication machinery of enveloped positive single-stranded RNA viruses, such as Covid19. AT-527 is currently in a Phase III study ‘SUNRISE-3’ evaluating it for the treatment of patients with COVID-19.

August Company Presentation

An interim analysis from this key study is scheduled for around the end of the year. Top line results from SUNRISE-3 anticipated mid-2024. If all goes to plan, management has stated it plans to file an NDA for AT-527 by the end of 2024. This is a widespread study, and the company is targeting approximately 330 testing sites across 30 countries. SUNRISE-3 is also focused on high-risk patients. The trial’s primary endpoint is all cause hospitalization or death through Day 29. Some 2,200 patients have been enrolled in the study’s monotherapy cohort.

Back in October of 2021, this candidate failed to meet the primary endpoint in a Phase 2 trial evaluated it to treat certain patients with COVID-19. This news caused a huge sell-off in the stock.

August Company Presentation

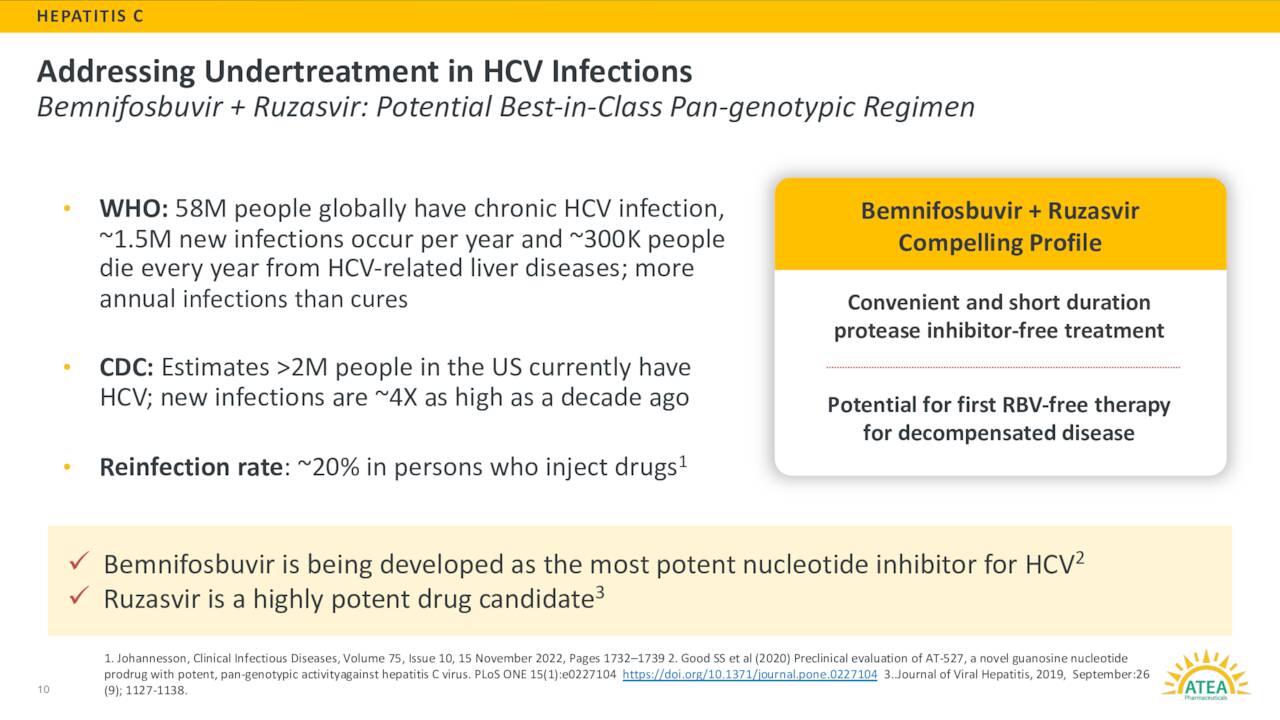

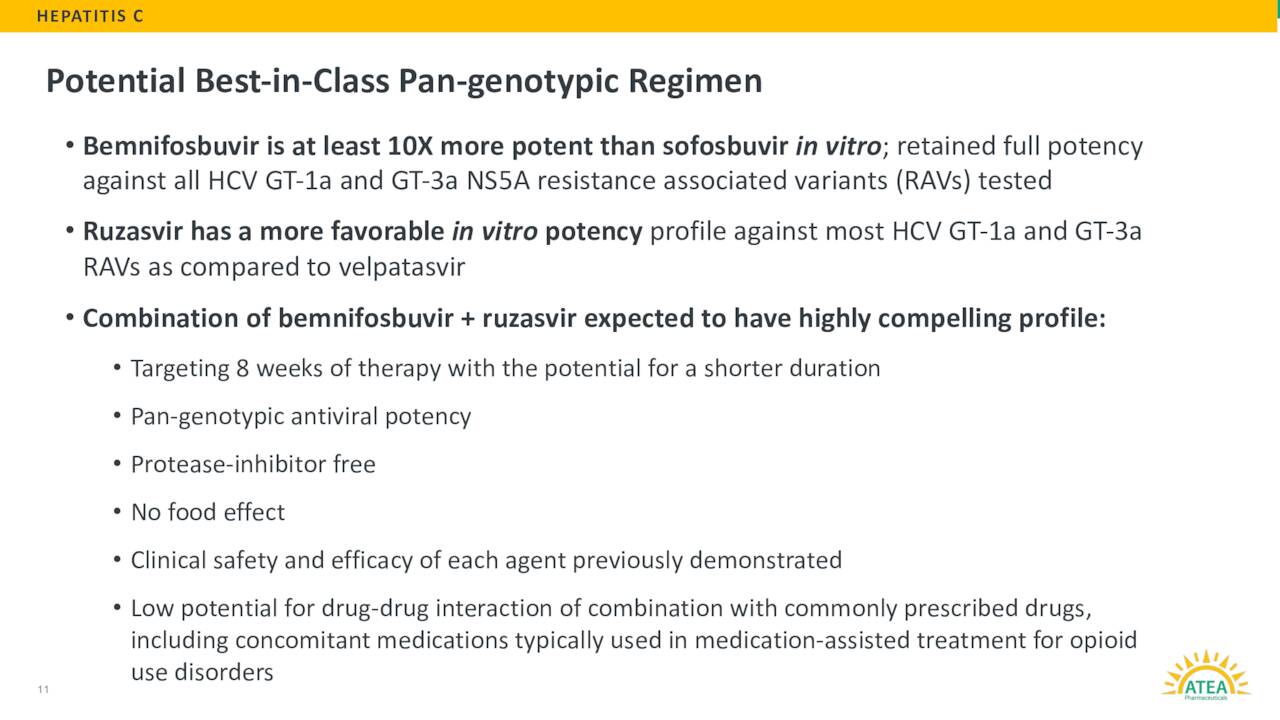

Now Atea Pharmaceuticals is also evaluating a combination of bemnifosbuvir and ruzasvir as a potential treatment for HCV. They began dosing the first of roughly 60 patients in a Phase 2 study around this indication in June of this year. Interim results should be out from this trial near the close of 2023. The goal of this program is to offer a protease inhibitor with a shorter duration option for hepatitis C patients than the current standard of care with and without cirrhosis.

August Company Presentation

Analyst Commentary & Balance Sheet:

The company has been spurned by the analyst community. Only three analyst firms (Morgan Stanley, Leerink Partners and JPMorgan) have chimed in on the company this year. All have Hold or Neutral ratings on the stock. JPMorgan downgraded the shares on August 10th as it sees a ‘limited market opportunity‘ for AT-527 to treat Covid-19.

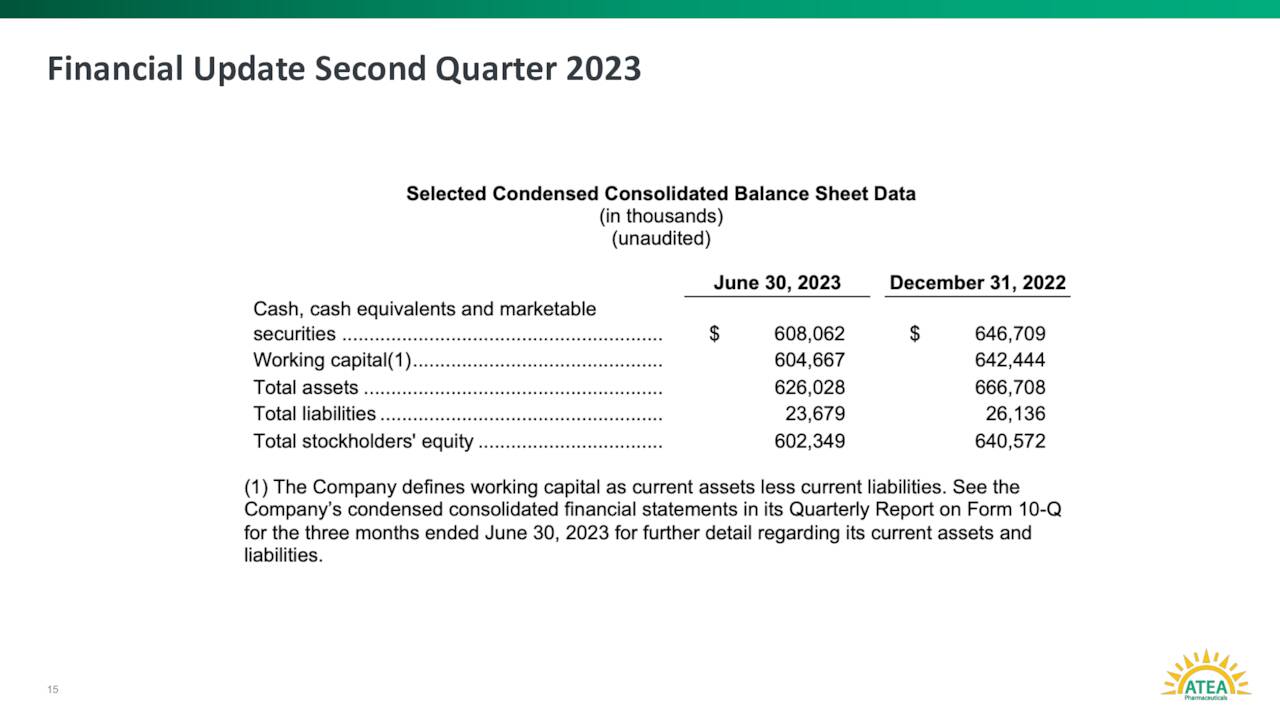

Approximately one out of every 40 shares of the stock’s outstanding float are currently held short. There has been no insider activity in the shares since the company came public. The company ended the second quarter with just under $610 million of cash and marketable securities on its balance sheet. Atea Pharmaceuticals burned through just less than $40 million worth of cash to fund all their operations in the first half of 2023. Management has said cash on hand provides Atea Pharmaceuticals of a cash runway well in to 2026.

August Company Presentation

Verdict:

The problem for Atea Pharmaceuticals and its shareholders is that its main efforts are around a candidate with likely a limited market as the Covid pandemic fades into memory. Now Bemnifosbuvir or AT-527 has been fast tracked by the FDA for Covid as the agency still sees unmet needs in the space, it should be noted. Bemnifosbuvir also has a high barrier to resistance thanks to its mechanism of action. This means it could deliver the same potency across all of the myriad variants of Covid. Given how often this virus mutates, that is a positive. If this candidate had been approved in 2021 or 2022, this story might have had a completely different ending.

August Company Presentation

Potential approval of AT-527 in 2025 thus doesn’t move the needle for me as far as making Atea Pharmaceuticals investable. Now, its cash balance does currently dwarf its current market capitalization, making additional downside unlikely for the time being. However, that cash will eventually be burned off in developmental efforts. Unless one believes a new takeover offer will emerge and management will consider it this time around, an investment in AVIR doesn’t seem to have much merit given the current uncertain market environment.

Irrelevance only creeps up on you if you let it.”― Stewart Stafford

Read the full article here