Armada Hoffler Properties (NYSE:AHH) is a vertically integrated REIT that owns and operates a variety of real estate assets in southern half of east coast that include mixed-use, retail, multi-familiy residence and office properties. The company also has a side business that consists of offering services related to construction and development as well as fee-based consulting services. At the current valuation, the company offers an interesting opportunity for long-term investors with income focus who feel comfortable with REITs in general.

Across its entire portfolio (including residential, retail, office and mixed-use properties) the company enjoys a combined occupancy rate of 97% which is difficult to achieve for a real estate company especially if there are office spaces in the mix. We’ve seen sharp drops in occupancy rates of offices since the COVID pandemic of 2020 and investors have been abandoning office REITs across the board because of that.

Occupancy rates (Armada Hoffler)

Most of the company’s properties are classified as Class-A properties which refers to those buildings that are either newly built or newly updated, in central locations with desirable amenities and modern class-of-art facilities. These types of buildings tend to command higher rents, better quality tenants, longer contracts, better occupancy rates and higher profit margins overall.

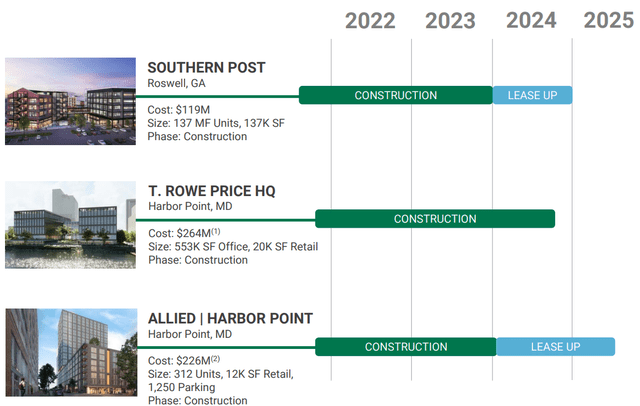

Since the company is vertically integrated, it is involved in not only managing properties but also in developing new projects either alone or in partnership with other companies. For example, the company is currently involved in 3 large projects including Southern Post in Roswell (Georgia) that is going to finish later this year and be renting early next year. The company is also in a 50-50 joint venture with T. Rowe Price (TROW) to build this company’s new headquarters in Harbor Point which will be finished later next year and house 553k square-feet of office space and 20k square-feet of retail space. The building will be occupied as soon as it is finished. The company is also in another joint venture where it is the 90% partner to build Allied/Harbor Point project that will finish up this year and start leasing up next year. Some of these development projects are very large and costly but many of them already have occupants lined up as soon as they are finished while others are joint ventures which includes the occupants themselves so the company doesn’t even have to put 100% of the development money upfront in those cases.

Ongoing Development Projects (Armada Hoffler )

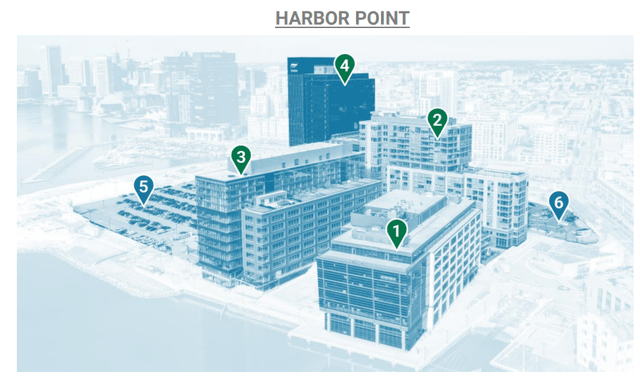

The company’s properties often seem to be clustered in certain areas. For example in Harbor Point the company already owns 4 buildings in the same area where it is building a new HQ for T. Row Price which is also close to the company’s other development project Allied/Harbor Point. There are certain advantages and disadvantages about having several properties clustered in the same area. The biggest advantage is that these properties can complement each other since each building has a different use (such as office, retail, residence) and they can create a synergy in a region. Second, the company can get better tax deals from local authorities by investing so much in a specific area. Third, quality attracts quality and if the company puts several Class A buildings in one section, it will attract high quality tenants which can add up over time. If there are many high-quality tenants in an area other high-quality tenants might want to be located there too. Also it may be easier to manage properties that are clustered in the same area from a logistics and operations perspective. There are some disadvantages to this approach too though. First, it may indicate that the company is not diversifying enough and if there is an adverse economic impact that affects one region specifically, this could have an oversized impact on the company. Second, (god forbid) if there was a disaster or an adverse event in one area, it could affect more than one property belonging to the company.

AHH’s Harbor Point Assets (Armada Hoffler)

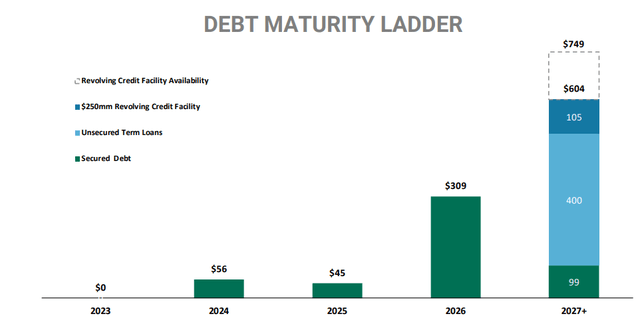

Speaking of risk, the company’s management is very conservative with how they approach debt management. The company’s property debt to EBITDA multiple is relatively low at 5.4x indicating that it could take the company less than 6 years to pay off all of its debt with existing income. Some of the company’s debt is on fixed rate while others on variable rate but the company uses hedging on 100% of its variable debt as part of its risk management to ensure that its debt servicing won’t get to levels that are out of control. The company effectively uses a number of instruments to hedge against rises in interest rates. Also, when we look at the company’s debt maturities, we see very little debt maturing until 2026. The majority of the company’s debt will be maturing in or after 2027 which gives it plenty of time to refinance or roll some of those debts.

Debt maturity calendar (Armada Hoffler)

The company’s properties are mostly located in mid-Atlantic region and Florida which enjoy good weather all year and a lot of business as well as touristic activity. This region also boasts a higher than average growth rate in both population and economic activity and lower taxes in general so the company finds itself located in areas that can generally be considered business friendly.

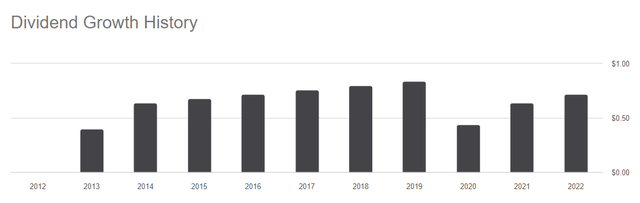

The company used to have a good dividend growth story up until 2020 which got disrupted by the effects of the global pandemic. After growing its dividends significantly for 6 years in a row the company had to cut its dividend by almost half in 2020. Since then it’s back to growing its dividends but the company is still below 2019 levels so it may take a year or two to get there. Earlier this year the company gave a small bump to the dividend, raising it from 19 cents to 19.5 cents but it’s still well below 2019’s quarterly rate of 22 cents. This is somewhat bothersome and those investors who like steady dividend growth might be turned off by this. The company’s management understands the value of growing dividends and they have every intention to keep growing dividends for as long as they can but sometimes external factors get in front of this and things get disrupted.

AHH Dividend History (Seeking Alpha)

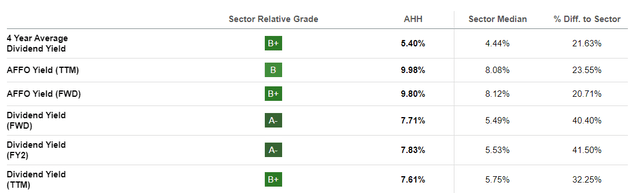

The company’s current dividend yield of 7.71% is significantly above the sector average of 5.49% so even though the company’s dividend growth has been disrupted it still offers a pretty nice yield for investors.

Dividend scorecard (Seeking Alpha)

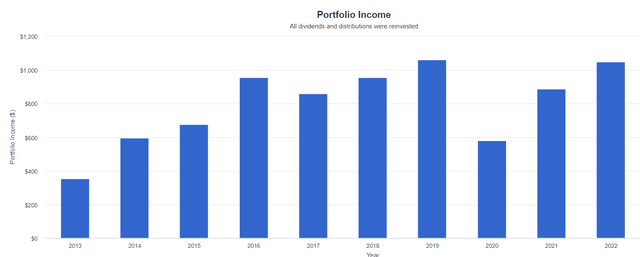

If you had bought $10k worth of AHH when the company became public in 2013 and held until now while reinvesting dividends, you would be generating about $1,050 per year in annual income which represents a yield of 10.5% against your original costs which shows that you can grow your income by reinvesting all or some of your dividends even if the company’s dividend growth gets disrupted.

Growth of AHH Income (Portfolio Visualizer)

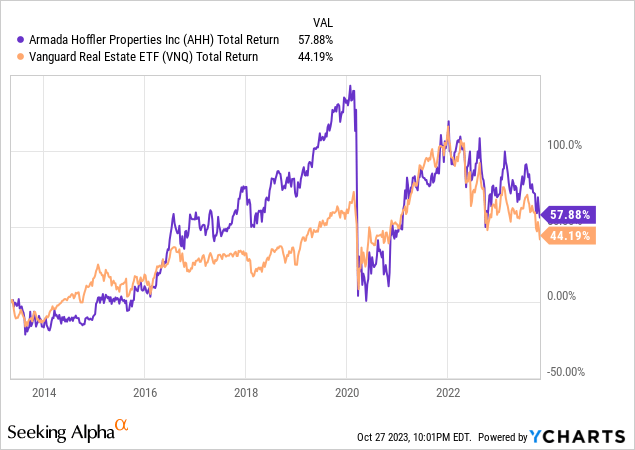

Since inception, the company has outperformed the REIT index (VNQ) but its annual average return of 5% is not that great either. The stock was doing really well until 2020 and its total return between 2013 and 2020 was close to 150% but it never fully recovered from the COVID crash. Some people will interpret this as a chronic problem and stay away from the stock while others will see this weakness as a buying opportunity.

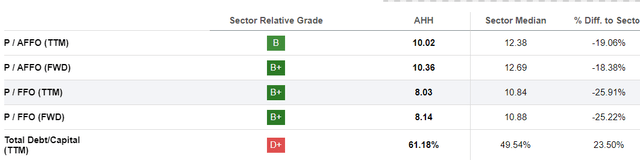

Speaking of opportunities, the company’s valuation looks decent as compared to sector average. The company’s trailing P/AFFO is 10 compared to sector average of 12 indicating a discount of almost 20%. On forward basis it’s 10.36 versus sector average of 12.69 which also indicates a 18% discount. On non-adjusted basis, the company’s P/FFO ratios are 8 for both trailing and forward basis, indicating a 25% discount against the sector average of 10.8.

AHH Valuation (Seeking Alpha)

The last 3 years have been very brutal for REITs across the board. First, the sector suffered a pretty steep drop due to COVID lockdowns and then as it was recovering from the effects of the pandemic, the sector got hit by interest rate hikes driven by high inflation. Historically it was always believed that REITs would serve as a good hedge against inflation because the sector is heavy in assets that tend to not only hold up their value but actually benefit from inflationary environments. It was also believed that a high inflationary environment would allow real estate companies to raise their rent prices liberally. While it may be true that real estate sector usually benefits from inflation, it is also true that this industry is interest-rate sensitive due to its capital intensive business which requires it to carry large amounts of debt. So REITs were not necessarily hurt by inflation itself but more by rising rates which was a byproduct of inflation.

For long term investors this probably creates a buying opportunity as long as they have a long term vision. Often times you see people buying a stock and start panicking or complaining within weeks if the stock didn’t have a rally and provide them with quick riches. Investment takes time and patience and very few investors seem to have long-term focus these days. Many investors just want to push a button and get rich and maybe they were conditioned to be that way because of the recent bull market of 2009-2021 which made a lot of people very wealthy very quickly. Still, investors should only invest their money into these types of stocks if they truly have a long term focus and patience that comes with it.

Read the full article here