Ardmore Shipping Corporation (NYSE:ASC) recently noted a transformation phase that included the optimization of the schedules of its ships and the reduction in fuel costs. I believe that these efforts could bring FCF improvements in the coming years. Also, considering the initiatives with respect to sustainability and perhaps more attention from investors, I think that the cost of equity could also lower. Yes, there are risks coming from lack of adequate financing or failed refurbishment of used ships, however, I think that ASC is currently trading very undervalued.

Ardmore

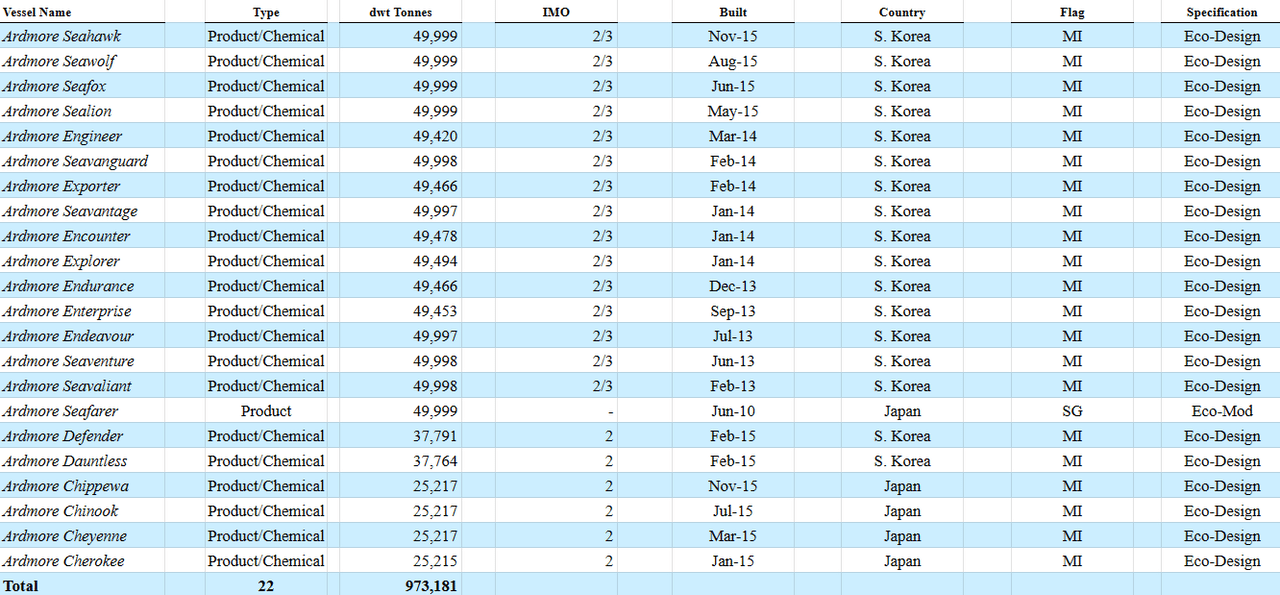

Ardmore is a company that offers international maritime transportation services, particularly oriented to the transportation of high-risk chemicals, sustainable fuels, and petroleum products in general. As of June 30, 2023, the company reported 22 vessels, mostly built around 2010 and 2015. Almost all vessels included an eco-design specification.

Source: 6-k

The company owns and operates its own transport fleet, and is currently considering a transformation strategy for the future oriented towards the creation of value for shareholders that has three development points: transition projects, technological transition, and transportation of sustainable fuels. The company aims to create long-term relationships with its customers.

This transformation plan is subject to forecasts on the growth of activity within the transportation market and the demand for the transportation of high-risk chemicals and sustainable products. In any case, at present and by far, the largest type of cargo that the company transports is petroleum products, so this transformation is expected to be carried out over the next few years in the long term.

Operations are concentrated in a single operating segment where the ships that the company currently has under its ownership operate. The income may be exclusively from the payment of customers to the company by virtue of cargo transportation, and the company distinguishes three types of payments in this regard. The payments accrued for transportation in cash, usually for short trips, the payments established from the arrangements for the duration of the trip, and ultimately the commercial agreements that are the least frequent and commit the fleet within the transportation with logistics established by third parties.

Balance Sheet

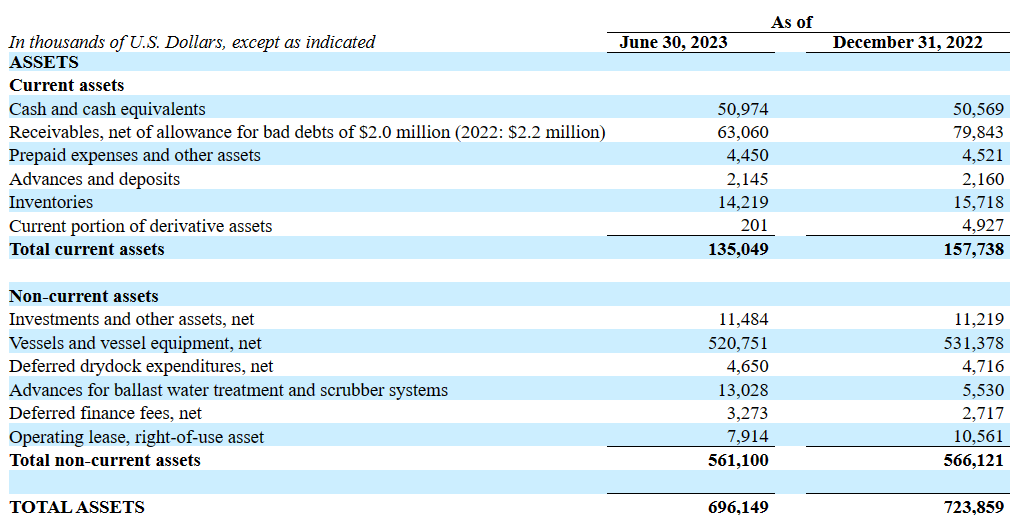

As of June 30, 2023, the company reported cash and cash equivalents worth $50 million, accounts receivables worth $63 million, and prepaid expenses and other assets of about $4 million.

Additionally, with inventories worth $14 million and total current assets of about $135 million, the current ratio stands at about 2x-3x. I really believe that management has sufficient liquidity to conduct its operations as well as to make further investments in capex.

Vessels and vessel equipment stood at close to $520 million, which is close to the current market capitalization. The fact that the book value of vessels is close to the market capitalization appears to indicate that the company stands a bit undervalued. With total non-current assets worth $561 million, the asset/liability ratio is not far from 3x-4x. In sum, I think that the balance sheet stands in a good position.

Source: 6-k

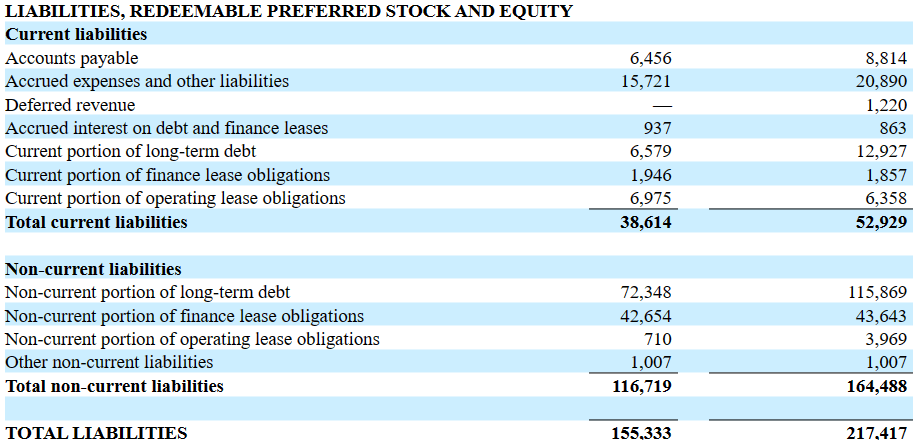

I am not really concerned about the total amount of liabilities and debt. In my view, the net leverage could increase to buy new vessels or finance further transformations. The current portion of long-term debt stands at close to $6 million, with the current portion of finance lease obligations worth $1 million and the current portion of operating lease obligations worth $6 million. Besides, with total current liabilities of about $38 million and non-current portion of long-term debt of $72 million, total liabilities were equal to $155 million.

Source: 6-k

The company recently signed financing agreements with banks, which are priced at the Secured Overnight Financing Rate. I included these assumptions in my financial model, so I believe that investors may want to read a bit about the financial terms obtained from financial institutions.

During the third quarter in 2022, we entered into new financing arrangements with ABN AMRO and CACIB and with Nordea/SEB. These new facilities are priced at the SOFR. Source: 6-k

On June 15, 2023, we amended our term loan agreement with ABN AMRO Bank NV and Credit Agricole Corporate and Investment Bank. The amendment converted 50% of the outstanding balance of the facility into a revolving credit facility with the remaining 50% of the outstanding balance continuing as a term loan facility. Source: 6-k

Recent Transformation Efforts Could Lead To FCF Margin And FCF Improvements

As mentioned previously, Ardmore’s strategy is currently focused on the three-stage transformation of its business model, and is particularly oriented towards future growth in the trade and use of sustainable fuels as well as vegetable oil. Transportation of this type requires a series of adaptations to the ships, and the company’s technology will be aimed at meeting the emerging needs of the industry based on this change in trend.

Regarding the internal operational arrangements, the objective is set on the reduction in general costs, the optimization of the schedules of its ships, the reduction in fuel costs for transportation, and the expansion of activities at a geographic level through the acquisition of ships as the capital allocation structure allows. In my view, these initiatives will most likely lead to improvements in the cash flow statement.

Sustainability Reports And Further Communications May Bring Investors Interested In Sustainability Industries

I really believe that the efforts made by management in terms of communicating sustainability initiatives could bring significant attention from new investors. In the last quarter, the company announced the publication of the 2022 Sustainability Report, which is a clear example of recent efforts made by the company.

On June 15, 2023, we published our 2022 Sustainability Report, highlighting our progress towards a more sustainable future. In 2022, we reached new heights in both operating performance and sustainability. We continue to believe that consistent superior operating performance is a key driver of long-term value in our business, and we are committed to driving our sustainability agenda forward. Source: 6-k

In this regard, it is worth noting that the Sustainable Finance Market is expected to grow at close to 22.4% CAGR from 2023 to 2032. Ardmore will most likely not see such an increase in net income growth, however, we may see certain improvements if sustainability efforts continue.

Sustainable Finance Market size was valued at USD 4.2 trillion in 2022 and is projected to register a CAGR of 22.4% between 2023 and 2032, driven by increasing impact investing efforts. Source: Sustainable Finance Market Size | Growth Statistics, 2023-2032

Financial Model

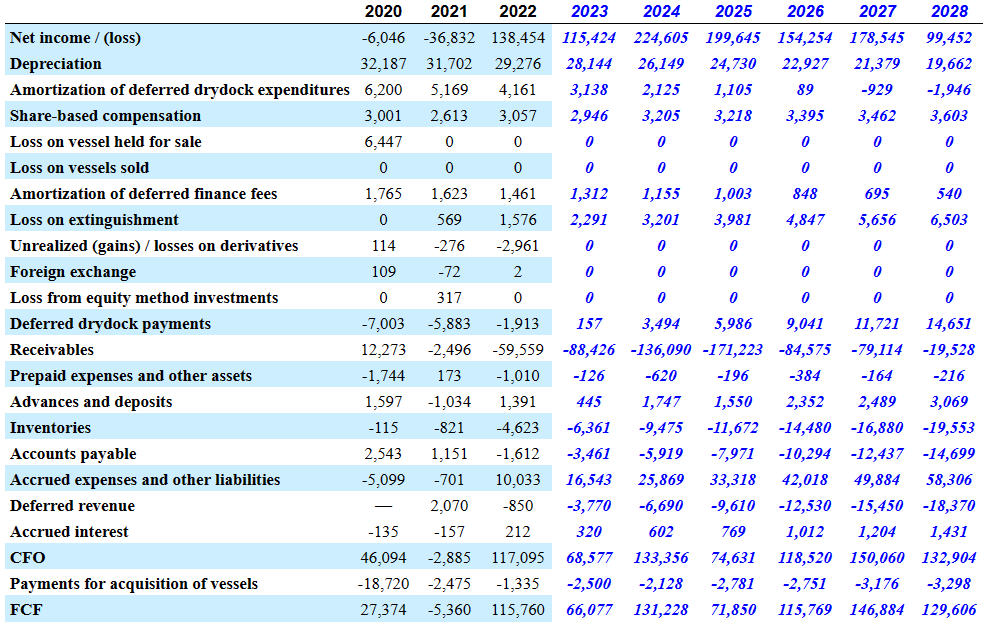

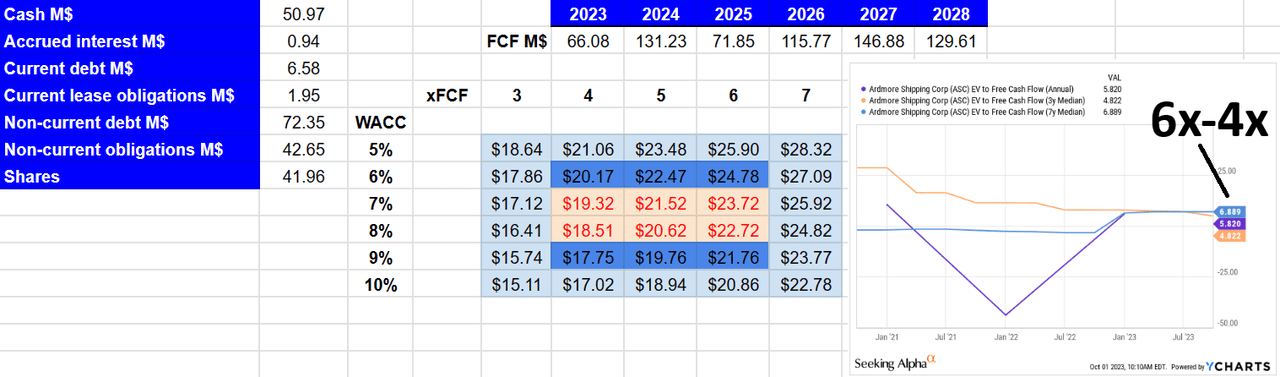

My financial model makes the following conservative forecasts. I expect net income to be close to $99 million, depreciation of $19 million, and amortization of deferred drydock expenditures worth -$2 million.

Besides, I included share-based compensation of $3 million, which is close to what the company reported in 2022. Additionally, without loss on vessel held for sale, loss on vessels sold, or amortization of deferred finance fees, I did include deferred drydock payments worth $14 million, with receivables of close to -$20 million, prepaid expenses and other assets of about -$1 million, and changes in inventories close to -$20 million.

If we also include changes in accounts payable of about -$15 million, accrued expenses and other liabilities worth $58 million, and deferred revenue of -$19 million, 2028 FCF would be close to $129 million.

Source: Cash Flow Expectations

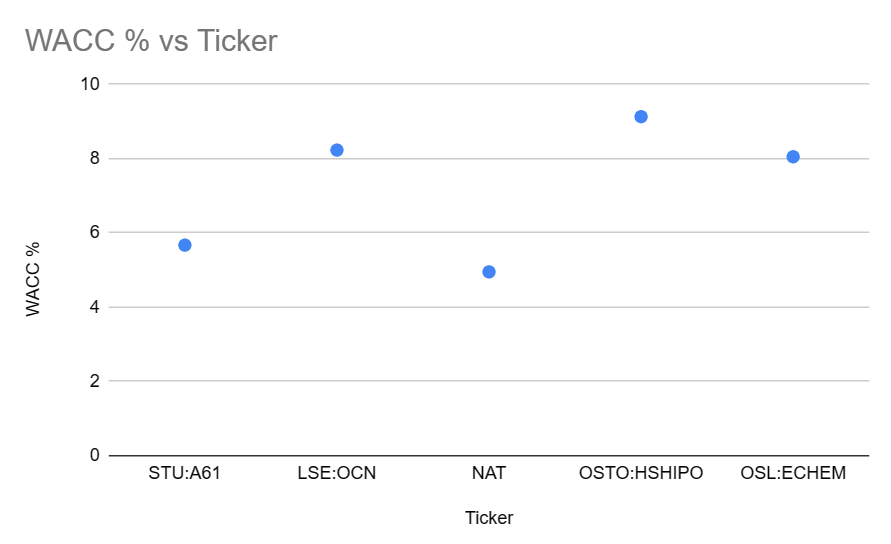

I checked the WACC of other peers and that of Ardmore. I do not think that the WACC may be far from 4.5% or 9.51%. With this in mind, I decided to run a sensitivity analysis with a cost of capital between 5% and 10%.

Source: Gurufocus

In the past, the company traded at about 6x-4x FCF, so I believe that the 2028 terminal EV/FCF multiple could range between 3x and 7x. Adding cash close to $51 million, and subtracting accrued interest, short term debt, current obligations, and long term debt, I obtained an implied valuation close to $15 and $28 per share.

Source: My Valuation Model

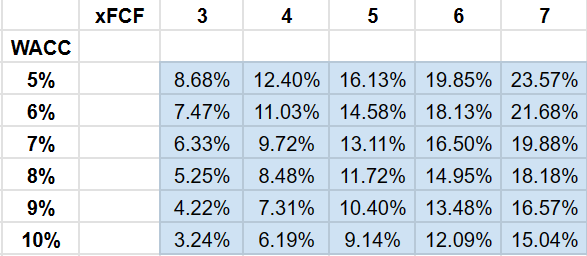

The calculation of the IRR also resulted many times in double digit figures for a WACC of more than 7% and more than 4x FCF. In sum, I think that the company remains significantly undervalued.

Source: My Valuation Model

Competitors

Competition within the maritime transport industry by ships is high, and is given by the companies that own and operate this type of service, as well as the structures of the large oil and fuel companies that have their own means of transport at the regional and international level. Furthermore, the participants have varied structures where we find public companies, state companies, and private companies participating in this market. The general cost strategy that keeps up the company is a key factor when it comes to the possible price offer for its customers.

Risks

Along with high competition, the maritime transport market is linked to the contracting of services and a great volatility in their price offer, which undoubtedly generates a risk for the operational activity of the company. This highlights the importance of the internal cost strategy that the company maintains and adds another series of factors such as the legal conditions in the ports where its ships dock and the risks inherent to international operations.

On the other hand, the company, in the form of a series of financial complications, can complicate future access to credit lines and financing. An example is the liquidity available for the mutation of its fleets or the acquisition of new ships, as well as the refurbishment of used ships. Ultimately, Ardmore reports a concentration on its clients, since the two main clients accounted for 10% of the company’s annual revenue each.

Conclusion

Ardmore is currently undertaking a period of transformation, which may bring significant operating performance improvements, and may enhance FCF growth. I also believe that efforts with regard to sustainability and communication may also bring visibility and new investors interested in sustainability investments. Even considering risks from lack of adequate financing, failed refurbishment of used ships, or failed international transport operations, I think that Ardmore is significantly undervalued.

Read the full article here