Introduction

I’ve been covering US lithium-ion battery recycling company American Battery Technology (NASDAQ:ABAT) on SA since early 2021 and I’ve written a total of six articles about it so far. The latest of them was in June 2023 and in it I said that the shift of focus away from the Fernley pilot plant to the McCarran and Tonopah Flats projects could boost the cash burn rate.

Since then, American Battery Technology has uplisted to NASDAQ, secured two government grants, and released its FY23 financial results. The market valuation of the company has decreased by over a third since my previous article but my rating on the stock remains a strong sell as the annual report revealed that the Fernley facility is still unfinished and no longer a priority, and that cash was down to just $2.3 million as of June. Let’s review.

Overview of the recent developments

If you aren’t familiar with the company or my earlier coverage, here’s a short description of the business. American Battery Technology was previously known as American Battery Metals Corp and in January 2020 it announced plans for a pilot plant in Fernley, Nevada for the recycling of lithium-ion battery metals, such as lithium, cobalt, and nickel. This facility was supposed to cost about $35 million and be up and running by the second half of 2020. American Battery Technology secured the funding for the construction in September 2021 following an $39.1 million equity offering. While the company calls it a pilot plant, the Fernley facility boasted commercial scale operation numbers as it was supposed to 20,000 metric tons of scrap materials and end-of-life batteries per year, thus booking revenues of about $160 million per year at an EBITDA margin of above 80%. In my view, this was a red flag as the margins sounded overoptimistic considering battery recycling majors like Li-Cycle (NYSE:LICY) aim for EBITDA margins of about 50%. The Fernley facility was then supposed to become operational in 2022 but the year came and went and in March 2023, American Battery Metals announced an agreement for the purchase of a 137,000 square foot commercial-scale battery recycling facility in McCarran. The latter was bought from Aqua Metals (NASDAQ: AQMS) and used to be a lead acid battery recycling plant before being damaged in a fire in December 2019.

American Battery Metals

Now, the Fernley facility is not even mentioned in the latest corporate presentation of American Battery Technology. Yet, there are three slides mentioning the Tonopah Flats early-stage lithium project in Nevada which cost just $8.2 million to acquire in FY23. There is also no mention of Fernley in the September 11 shareholder letter of American Battery Technology as the company seems to be focusing its resources on the McCarran facility. In the letter, the company said that it’s set to start feeding high-throughput quantities of battery materials in the coming weeks.

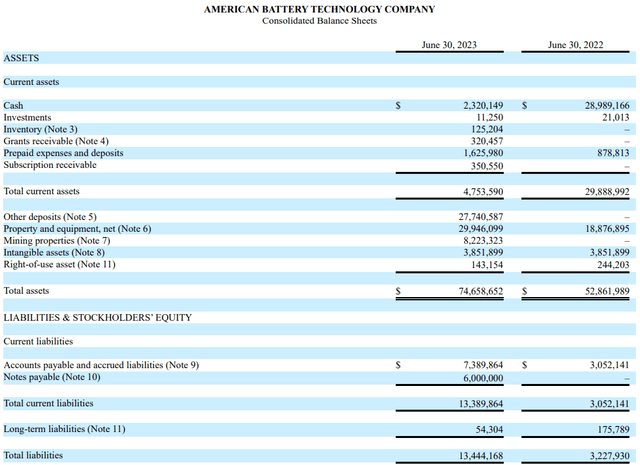

Other important milestones for American Battery Technology over the past few months include an uplisting to NASDAQ from the OTCQX on September 21 and securing a $57 million contract award from the U.S. Department of Energy (DOE) for a commercial-scale lithium hydroxide manufacturing facility in Tonopah in early September. In late September, American Battery Technology also received a contract grant award from the DOE for a $20 million project to scale, optimize, and commercialize next generation techniques techniques for lithium-ion battery recycling. Under the deal, DOE will provide $10 million in direct funding while the company and its project partners will contribute another $10 million worth of cost-share resources. While all of these sound like positive developments, I’m concerned that American Battery Technology was running out of cash at the end of FY23. You see, the FY23 financial report released on September 28 showed that the cash position was down by $10.3 million in Q4 alone and stood at just $2.3 million as of June 2023. The major changes in the asset base during Q4 FY23 included a $21.8 million quarter on quarter increase in other deposits and a $5.3 million boost in property and equipment. The other deposits seem to be linked with the McCarran facility as its acquisition was completed in August 2023. Considering operating expenses for FY23 were $21.6 million, this put American Battery Technology in a tough spot from a liquidity position. As of June, the company had a working capital deficiency of $8.6 million.

American Battery Technology

On August 31, American Battery Technology announced it inked a deal for $50 million in zero-coupon senior secured convertible notes. They mature in 2025 and can be converted into shares at 110% of the share price on August 28, which was $8.37. This means there could be significant stock dilution here if the share price moves above $9.21 (110% of $8.37).

Regarding the investment in property and equipment, it’s unclear how much of it was for McCarran and how much for Fernley. Regarding the latter, there are a few mentions in the annual report and I think the most important of them can be found on page 17:

The Company began construction before prioritizing the new location in McCarran, Nevada. The Company’s strategy is to construct multiple facilities and the Fernley location is expected to be a subsequent plant.

It seems that the Fernley plant could be mothballed for now.

Overall, I think it’s disappointing that the Fernley facility has been delayed indefinitely considering it was supposed to be operational over a year ago. In addition, there are no details about the margins of McCarran and there could be significant stock dilution here if the share price rises above $9.21 due to the convertible notes. In my view, the business of American Battery Technology isn’t worth much in its current state and I think that opening a short position seems viable as data from Fintel shows that the short borrow fee rate stands at 15.94% as of the time of writing. However, it could be best for risk-averse investors to avoid this stock as there are no call options available to hedge the risk here.

Looking at the upside risks, I think that the major one is that I could be underestimating the prospects of the McCarran facility. This new plant is expected to process over 20,000 metric tons of material per year, and it’s possible that the targeted revenues and EBITDA margins are close to those of the Fernley plant. Another risk here is that the prices of microcap stocks can increase significantly without clear catalysts.

Investor takeaway

The 80% EBITDA margin Fernley plant of American Battery Technology was delayed for several years, and it seems that it has been mothballed now. The balance sheet looked in a rough shape at the end of June and the company is now funding its business with convertible notes that could result in significant stock dilution. It seems that American Battery Technology is focusing on putting its McCarran facility into operation but given the history of delays at Fernley, I’m not optimistic about its prospects. While short-selling here seems viable, I think that risk-averse investors should avoid this stock.

Read the full article here