We wrote about ADTRAN Holdings, Inc. (NASDAQ:ADTN) back in June of this year when we warned investors that a continuation of the established bearish trend was a clear possibility over the following months. Our premise played itself out with shares of Adtran losing almost 19% of their value over the past 6+ months. In fact, in real terms, when one takes into account the almost 12% return the S&P500 has delivered over the same timeframe, shareholders of Adtran have suffered a sizable opportunity cost in recent times.

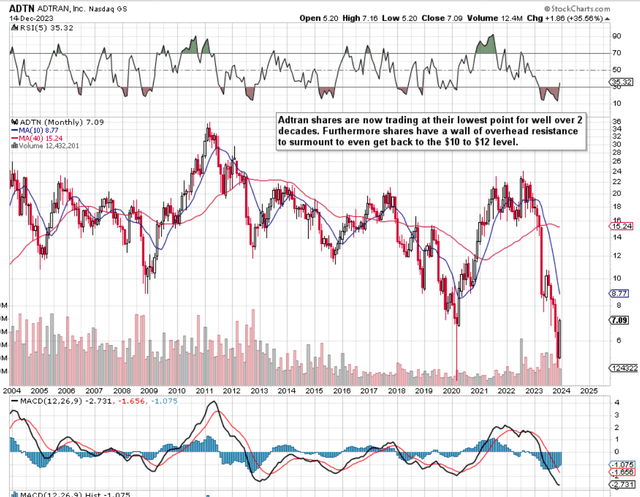

Technically, as we see on Adtran’s long-term chart below, shares are at their lowest point in more than two decades where no green shoots have been appearing concerning a potential long-term bottom. We state this because the long-term MACD histogram remains depressed despite shares bouncing off their lows of approximately $5 a share last month. Even if the long-term bottom is in, however, investors would do well in recognizing the significant amount of overhead resistance prevalent in Adtran at this stage. This goes back to our earlier point concerning the risk of a sizable ‘opportunity cost’ if one remains invested on the long side in Adtran. We state this because not only has management decided to remove the dividend (thus removing an earner for shareholders) but sustained inflation can also wreak havoc on long-term investments concerning ‘real’ gains over time.

ADTN Long-Term Technicals (Stockcharts.com)

Deep Cost-Cutting On the Way

Management decided to enact heavy cost-cutting measures after a disappointing Q3 earnings report where both the negative earnings print & top-line sales missed their estimates for the quarter. The significant cuts (which will affect the income statement over time) as well as the suspension mentioned above of the dividend will convert Adtran into a much smaller outfit which obvioulsy has ramifications for investors going forward. These cuts though will be done at a cost to shareholders as we learn from the balance sheet below.

Management reported $272.3 million in sales for the third quarter & negative operating earnings of -$24.9 million. Operating cash flow did come in positive in Q3 ($6.9 million) but was eaten up by capital spending ($13.6 million) and the last quarterly dividend payment of just over $7 million. We are always wary when a company’s balance sheet has to be deleveraged due to the absence of cash on hand or cash flow to make ends meet. On this, the CFO stated on the recent Q3 earnings call that annual savings of up to $90 million will come about due to a global headcount cull & a partial sale of owned property. Selling assets will affect Adtran’s book multiple and here is where investors need to be careful.

A popular calling card for value investors when stocks plummet is their book multiple in that investments in companies with low price-to-book ratios have historically performed well over the long term all things remaining equal. Given Adtran’s common equity at the end of Q3 came in at $684.9 million, the company’s trailing book multiple comes in presently at 0.815. Although this multiple may look attractive on the surface, the upcoming deleveraging of the balance sheet, the sizable amount of receivables & inventory ($600+ million combined) plus a possible impairment charge on the company’s sizable goodwill & intangible assets ($660+ million) bring risk & remain serious causes for concern in an asset-stripping environment. The fact that the recent writing off of $21 million of ‘end of life’ inventory demonstrates that the reported inventory number may continue to come under pressure going forward.

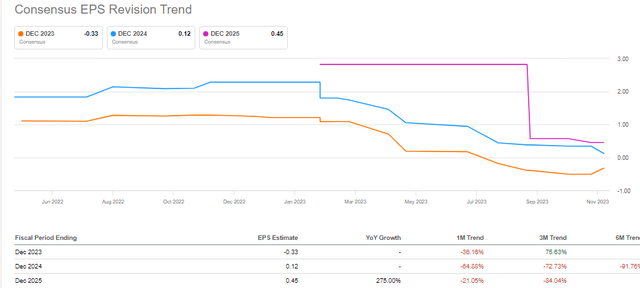

Bearish Earnings Revisions

As we see below, forward-looking earnings revisions continue to slide as the bottom line projection for fiscal 2024 is down over 60% over the past 30 days. This is worrying as the market seems to be pricing in sustained weakness in ‘Network Solution’ even though the ‘Services & Support’ segment (16.1% of revenues in Q3) grew both sequentially and over a rolling quarter basis. When starting from a low gross margin base (>30%), management knows it has to be able to turn over product quickly to increase returns. This scenario though looks to be off the table over the near term as the CEO outlines in the concluding Q3 comments below.

we continue to focus on capturing fiber footprint with our optical transport and fiber access platforms, led by the U.S. and Europe and then drive adoption of our complete portfolio, including subscriber platforms, software applications, and services. Despite broader market challenges, we still made progress against these goals. While we remain very confident in our long-term outlook, we are in a period of market uncertainty due to ongoing inventory reductions and more restrained capital spending across our service provider customer base, particularly in the large service customer segment. This uncertainty led to more order push-outs in Q3 and Q4 of this year, driving us to take a more cautious approach with our forecast and operating model.

Therefore to sum up, given Adtran’s worrying technicals, balance-sheet concerns, and bearish forward-looking EPS revisions, we believe things may have to get worse in ADTN before finally getting better. Let’s see what the fourth quarter numbers bring. We look forward to continued coverage.