Investment Thesis

Adriatic Metals (OTCPK:ADMLF) is a polymetallic development company, which is close to production with its core Vares project in Bosnia & Herzegovina. This is a stock I have covered a few times over the last couple of years and I have owned Adriatic Metals during part of that period as well. The prior articles can be found here.

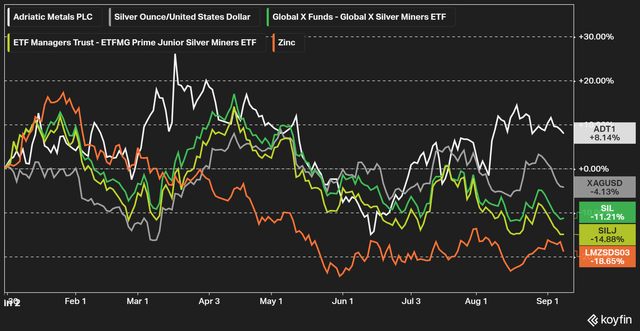

Adriatic Metals has had a relatively good year, up slightly, outperforming most silver miners this year. The performance is impressive in a year when the zinc price has been weak. Silver and zinc are the two main metals Vares will be producing, although there are material amounts of gold and lead as well.

Figure 1 – Source: Koyfin

Part of the reason for the positive performance is likely due to the exploration success the company has had, and we have possibly also started to see a re-rating begin as we approach production, even if there is likely more re-rating potential over the coming year as Vares scales up production.

Recent Developments

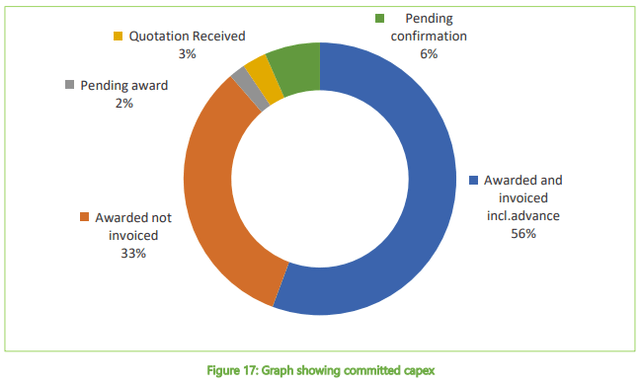

I covered this stock last in early July of this year, and the company has since that time had a few developments. Adriatic Metals did in late July release its quarterly activities report on Vares, which confirmed that 84% of the construction was then complete. The company did in late Q2 have its first ore drive and first concentrate production is expected to occur in November of this year.

With 94% of capital expenditure excluding contingency being awarded, pending award, or recently quoted, any further significant cost overruns would be very unlikely. The final project cost is now estimated to $182m, only 8% above the 2021 feasibility study, which is a great achievement in the inflationary environment we have seen over the last few years.

Figure 2 – Source: Adriatic Metals Quarterly Activities Report

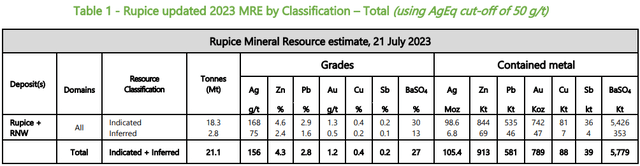

Adriatic Metals also released a resource update on the Vares project during the summer, from a lot of exploration drilling over the last few years. It is based on drilling up until May of this year. The resource update showed a 93% increase in indicated tones compared to the 2020 resource update, using a 50 g/t AgEq cut-off.

Figure 3 – Source: Adriatic Metals July 2023 Resource Update

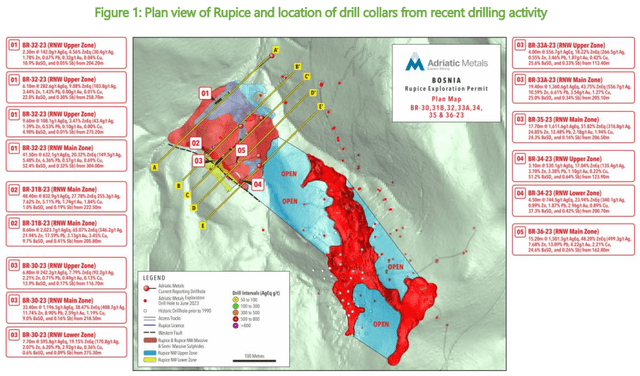

Now, it remains to be seen how much of that can be converted to reserves and can ultimately extend the mine life of the operation. However, based on the very impressive grades, it is fair to say the results do so far look very good. Recent drill results after the resource update have continued to be extremely good, so additional resource growth is also likely.

Figure 4 – Source: August 2023 Drill Results

In early August, the company did announce and complete a bought deal of around $32M, at a price £1.70 per share. Where the proceed will primarily be used to accelerate the exploration at Vares and some working capital requirements. This was a relatively small capital raise, offered at a minimal discount to the prior close, and it was very well-received by the market. The stock price bounced back very quickly following the announcement.

With that said, I always find it somewhat disappointing when management boost how undervalued the company is and how much free cash flow the operation will soon produce, and then not have the patience to wait for that cashflow to expand the exploration budget. This is, however, a very common behavior among junior mining companies.

Valuation & Conclusion

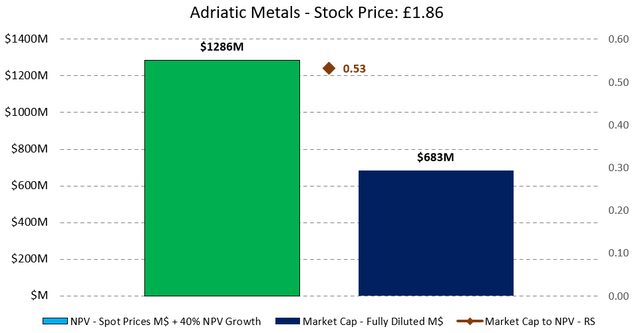

For the valuation of Adriatic Metals, I relied on the feasibility study as a base, which used an 8% discount rate, then adjusted the values to reflect metal spot prices. I have also assumed a 40% NPV growth, which is in my view a relatively conservative assumption based on the July 2023 resource update and the consequent drill results. The newly issued shares are included in this calculation.

Figure 5 – Source: My Estimates

We can see that Adriatic Metals is now trading with a market cap to NPV of 0.53, which is far from expensive if the company can execute on the production ramp up over the next few quarters. So, based on the valuation and potential growth prospects, Adriatic Metals looks attractive.

While I am not long the stock today, I might add it to the portfolio if we get a smaller correction. I have primarily changed my rating on the stock to a buy given the very impressive resource growth during 2023 and due to the fact that we are now even closer to production.

The large base metals’ exposure is a slight cause for concern, even if that is more of personal preference. Also, it is not uncommon to see delays in the ramp up of new mines, and we have lately seen a few precious metals companies be slow to re-rate following the commencement of production, even after commercial production has been achieved. So, a potential re-rate of Adriatic Metals might happen in 2024 first.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here