The following commentary is from the October 1st issue of my Short Seller’s Journal.

Housing market update – The highest mortgage rates in 20 years, the worst level of affordability since 1984 and increasingly tight household finances are starting to torpedo housing market activity.

After rising slightly in three of the previous five weeks, (from 142 to 147), the mortgage purchase applications index fell from 147 to 144 last week.

I suspect that it will fall more this week, as the 10-yr yield has risen inexorably from 3.35% in May to 4.60%, and from 4.38% to 4.60% just this past week alone.

The base 30-yr fixed rate mortgage has jumped to 7.5% (20% down, 740+ FICO), which means housing purchase affordability continues to get worse.

New home sales in August fell 8.7% from July vs. the consensus expectation of a 2.2% decline, while July’s 4.4% increase over June was revised higher to 8%.

I suspect the numbers for both July and August as estimated by the Census Bureau are wildly inaccurate. At the 90% level of statistical confidence, the August number could vary from +6.9% to -24.3%.

Why even bother putting together the data series? The months’ supply of new homes according to the Census Bureau is now at 8 months. I thought the narrative was that there’s a shortage of new home supply?

Recall that new home “sales” are based on contracts signed. As mentioned last week, 15.7% of all home purchase contracts signed in August were canceled at the highest rate in 20 years.

Based on the weekly trend in mortgage purchase contracts in July and August, and given the cancellation rate in August, I’d say it’s more likely that the 8% increase in new home contracts in July was lower than calculated by the Census Bureau, while the 8.7% decline was more severe than the CB calculus shows.

As more housing data from July and August is released, it looks like my view that home sales hit a wall in July and August may be correct. Existing and pending home sales have declined to near-historic annualized lows.

New home sales took off in January primarily because of the low inventory of existing home sale listings. In addition, homebuilders began to offer steep discounts to the list price along with other incentives.

Then in 2023, the rate buydown became all the rage, which enabled homebuilders to prevent sales from declining. But the incentives discounts have hammered profitability, as I have detailed in the recent earnings reports of D.R. Horton (DHI), Lennar Corp. (LEN) and KB Home (KBH).

It’s going to get worse, especially with the 10yr Treasury rate relentlessly grinding higher.

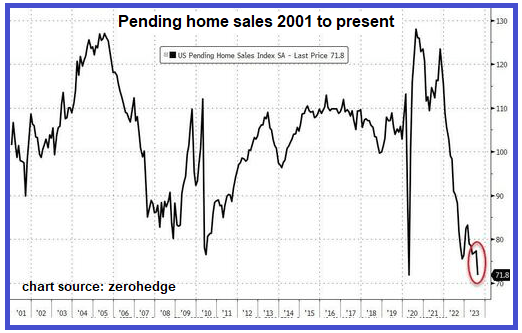

Pending home sales for August plunged 7.1% from July and 18.7% YoY. The decline hit all four regions (west, northeast, midwest, southeast), with the southeast down 9.1%.

The southeast had been the hottest region during the inflation of the bubble. The pending home sales index is down to the lowest reading during the pandemic lockdown, which is the lowest index level on record.

Pending home sales are based on contracts signed on existing homes. To be sure, there may some element of inventory selection holding back some potential sales.

But the pending number corroborates the August plunge in both new and used home sales. It’s now confirmed that the housing market hit a wall in July/August and the level of activity is lower than during the depths of the great financial crisis.

All of the homebuilder stocks have declined quite a bit since peaking in August. But all of them are still substantially higher than they were in late 2022, when new home sales started to take off.

I firmly believe that these stocks will retrace back to where they were trading in late 2022. The reason I say this is that, despite steady sales volume, the discounting, etc., has hammered profitability and earnings for all of these builders.

As an example, KB Home reported EPS for its FY Q2 2022 at $2.86 vs. $1.80 for the same quarter this year. Yet, the stock is trading 80% higher than where it was trading a year ago.

Similarly, LEN reported $5.03 for its FY Q3 2022 vs. $3.87 this year. Yet, the stock is 52% higher than it was a year ago. These valuation levels will soon be reset considerably lower.

Right now, I am expressing a bearish view on the housing market with Airbnb (ABNB) puts. This is more of a bearish bet on the existing home sales market because I expect that there will be a deluge of ABNB properties for sale in the next 6-12 months.

However, I’m going to invest in some Toll Brothers (TOL) and PulteGroup (PHM) puts because, on a percentage basis, these two stocks have not declined as much as the other homebuilders.

My understanding is that the market for high-end and luxury homes is transitioning into a bloodbath.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here