Written by Nick Ackerman.

Real estate investment trusts (“REITs”) have been getting hit hard by higher yields as the Fed ramped up interest rates. Additionally, utility companies are being hit by the same thing. In fact, utilities are the worst-performing sector on a YTD basis by a wide margin. Other defensive sectors, such as consumer staples and healthcare, also aren’t looking too healthy this year, either.

Softer guidance from NextEra Energy (NEE) has sent the sector spiraling lower, which, in combination with seeing the risk-free rates rising, is driving the sector significantly lower more recently.

U.S. Equity Sector Performance (Seeking Alpha)

Besides risk-free Treasury yields becoming more attractive alternatives to riskier equity assets, REITs and utilities are also business operations that generally rely on debt. A main form of growth for REITs is through financing new projects or acquisitions to grow their earnings. Utilities face heavy CAPEX requirements as infrastructure takes a tremendous amount of materials and labor to construct and maintain reliable services to customers.

Lower interest rates could certainly be a tailwind, but it also depends on the circumstance of why the Fed would have to cut interest rates. On the other hand, even if rates stay where they are and one believes that we are near peak interest rates from the Fed, we could anticipate some stabilization in these sectors as well. So, I don’t believe that we necessarily need to wait for the next one or possibly two hikes from the Fed to try to squeeze out the absolute bottom. Investing is a long-term game over many years, not generally trying to time the market from month to month.

All this being said, there are plenty of names for dividend investors looking at attractive yields and wanting some dividend growth in the future for long-term investors. Two names that look interesting and, I believe, deserve some investor attention are the NNN REIT (NNN) and WEC Energy Group (WEC).

NNN REIT

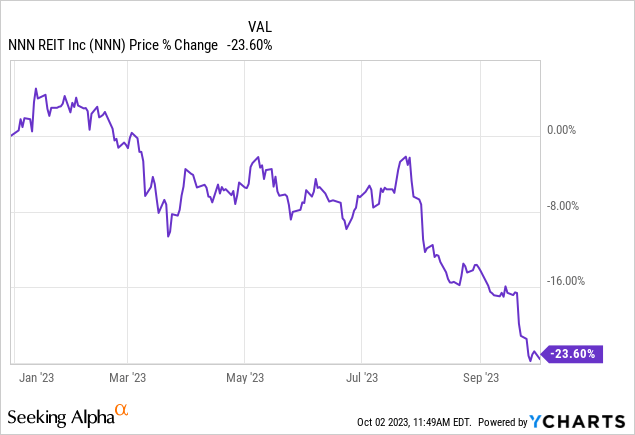

NNN REIT was formerly National Retail Properties, but they changed their name earlier this year. Unfortunately, the name change did very little to slow down the share price decrease that the REIT has been experiencing. Shares are now off nearly 24% on a YTD basis.

NNN holds a basket of single-tenant net lease retail properties with a high occupancy level of 99.4% as of their latest update. This is across 3479 properties in 49 different states. For further diversification measures, the REIT notes over 385 different national and regional retail tenants, so they are exposed to a varied basket of retail tenants. However, it’s worth noting that the top 25 accounts for roughly 55% of their rents.

They certainly aren’t any strangers to different economic conditions as they boast a 39-year track record, with 34 of those years seeing consecutive dividend increases. Additionally, they noted that a 20-year low occupancy rate only ever touched 96.4%. This is promising, considering that most economists are expecting some sort of recession as we head into 2024 or even in the tail end of 2023.

Thus, a recession, one of the reasons why we would anticipate potentially lower interest rates from the Fed in the next couple of years, is to help alleviate pressure from REITs and utilities.

Of course, the counter-argument to that is the tougher operating environment could then become the new headwind. So, seeing data that suggests a strong track record in even black swan events is somewhat comforting. It’s impossible to predict, but it more or less depends on the depths of the recession when one occurs and how much damage could be done. A shallow or mild recession could see limited pressure on the types of tenants that NNN leases to, but a deeper and prolonged recession would certainly hurt.

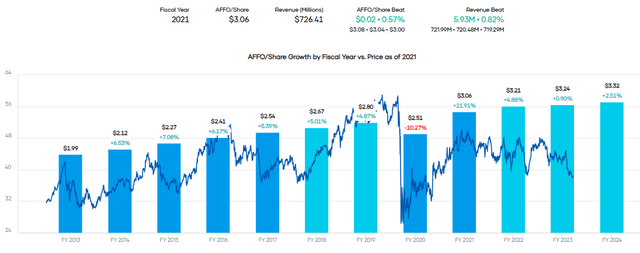

In terms of growth going forward, NNN is expected to produce some positive AFFO growth in the coming years. It certainly isn’t the most exciting name, but that could be considered one of its particular charms. The company has often been able to beat earnings over the last several years as well, with 9 of the last 10 FFO quarterly numbers exceeding those of analysts. Last quarter was the sole detractor from that trend as it only met expectations.

NNN Earnings Past and Future Estimates (Portfolio Insights)

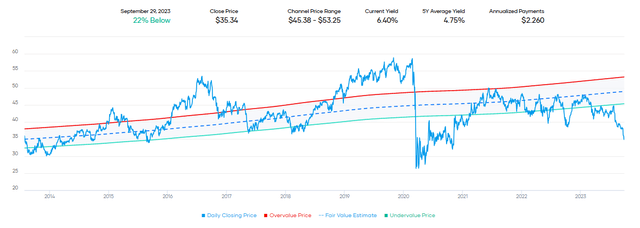

Given the more boring but consistent nature of NNN’s earnings, one might anticipate a higher yield being appropriate. For the most part, that is pretty much what has occurred over the life of this REIT. However, with this sharp sell-off, the yield is now pushing closer to 6.5%, well above its historical average. Some of this is mostly deserved as the risk-free rate has also ticked up, of course. Still, this is where the longer-term opportunity could come from in being rewarded in the future with growth and if/when yields subside.

NNN Fair Value Dividend Range (Portfolio Insight)

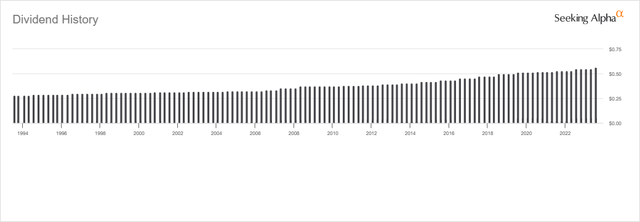

This dividend has been consistent in terms of seeing consecutive growth, as we noted above, boasting 34 years of consecutive increases. Based on the earnings estimates for next year and the recently announced dividend increase, the forward AFFO payout ratio is sitting around 70%. That leaves plenty of room for further increases in the future and some cushion if earnings take a hit during the next recession.

NNN Dividend History (Seeking Alpha)

WEC Energy Group

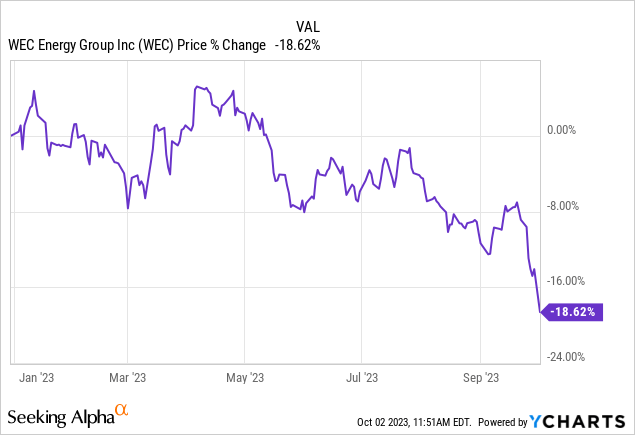

Another name that has been hit harder recently is WEC Energy Group. Shares are off only around 18.5% this year. Most of this coming in the last few days since NEE announced a soft outlook with its yield cutting distribution growth expectations in half. Unfortunately for me, I had sold $75 puts right before this latest plunge. The probability of assignment was 2% before NEE’s announcement.

There is no surprise here as the theme of covering NNN and WEC is due to being rate-sensitive. The announcement from NEE was more of an admission that higher rates are going to be impacting their outlook more significantly than they probably wanted to admit. After seeing risk-free yields breach new levels above last October 2022, it makes sense to see renewed pressure in this space – and we even saw it more broadly across the equity market as well.

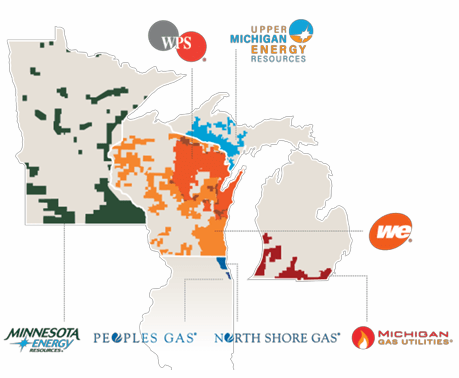

Even after some recovery from the lows, the shares are still attractively priced for a long-term income investor looking for a solid utility play. WEC Energy operates several utility companies under its grouping umbrella, serving 4.6 million retail customers with operations throughout Minnesota, Michigan, Wisconsin and Illinois.

WEC Energy Group Operations (WEC Energy Group)

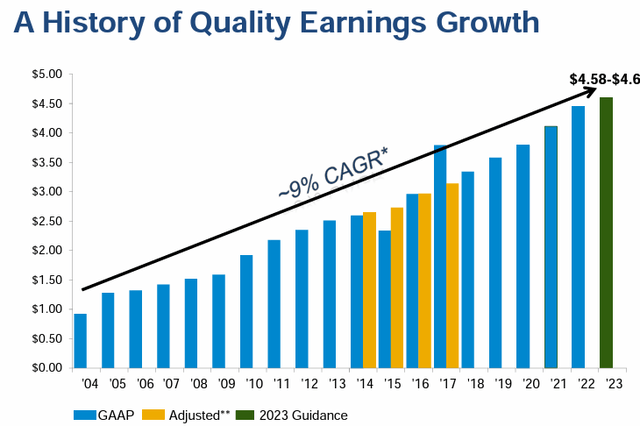

This company has been able to deliver solid earnings growth for shareholders going back to 2004. Even through the global financial crisis, earnings kept ticking higher.

WEC Earnings Growth History (WEC Energy Group)

Besides the company’s forecast for earnings growth heading through 2023, this is supported by analysts as well. The guidance delivered by the company is also something that should be weighed, given that they have now exceeded their guidance for every year for 19 years now.

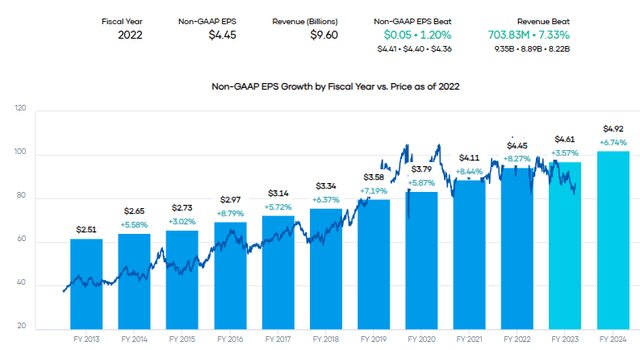

Analysts believe that the company will continue to deliver around 4-7% non-GAAP EPS growth in the next two years.

WEC Earnings History and Forecast (Portfolio Insight)

Interestingly, this is below just the more recently reaffirmed guidance from the company of 6.5 to 7% growth they are anticipating. Given that dynamic, they really are set up to exceed analyst expectations. That’s another feature of WEC that isn’t anything new as they have done for 16 out of the last 16 quarters beat analysts’ expectations.

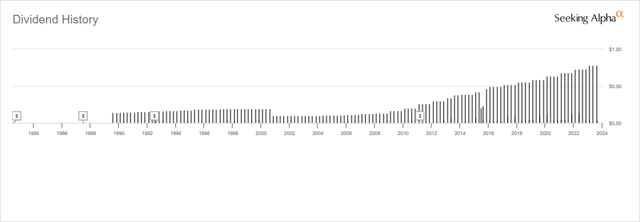

This company delivers consistent and boring growth. That growth has also translated into a steadily growing dividend to shareholders who can be patient over the long term. They’ve raised their dividend for 20 consecutive years, and they anticipate the growth to continue to be in line with their earnings growth.

WEC Dividend History (Seeking Alpha)

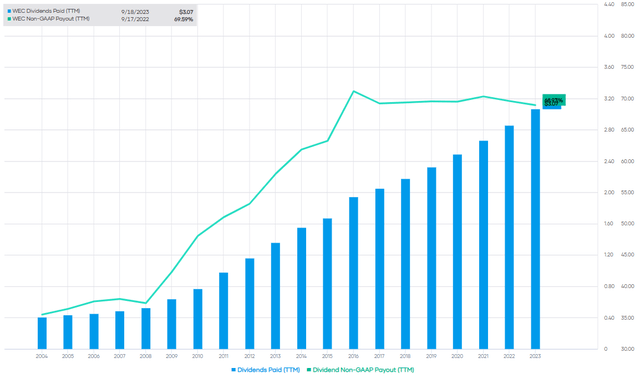

Based on the forward earnings estimates, we are looking at a payout ratio of 67.7%. This payout ratio has been fairly steady since going back to around 2015. Utilities and REITs generally pay a fairly sizeable amount of their earnings to investors, so this is another case of a healthy payout level with some cushion for a potential slowdown.

WEC Dividend Payout Ratio (Portfolio Insight)

Of course, if there is a potential slowdown, utilities can often be the ultimate defensive play, and that could be a tailwind for WEC. Their earnings are often not hit materially in a slowdown as consumers still consume electricity.

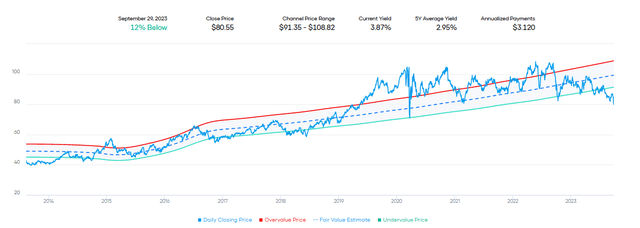

The yield might not be the highest for this consistent utility name, but it still represents an attractive entry for an investor from a historical fair value yield range. As of writing, shares are down another ~5% today.

WEC Fair Value Dividend Range (Portfolio Insight)

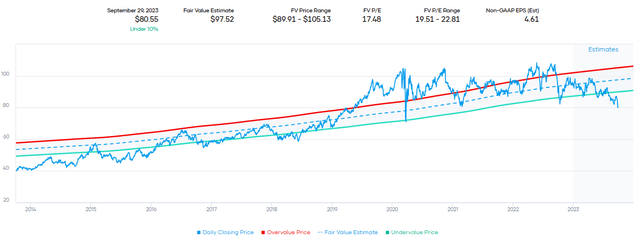

Additionally, if we look at the historical fair value P/E range, shares are also looking quite tempting.

WEC Fair Value Range (Portfolio Insight)

Again, similar to what was mentioned with NNN. The risk-free rate is definitely higher now, which is one of the main pressures that put WEC shares where they are today. However, this could still be a good long-term bet or even a short-term bet to get more defensive if one believes that the economy will start to slow down from here.

Read the full article here