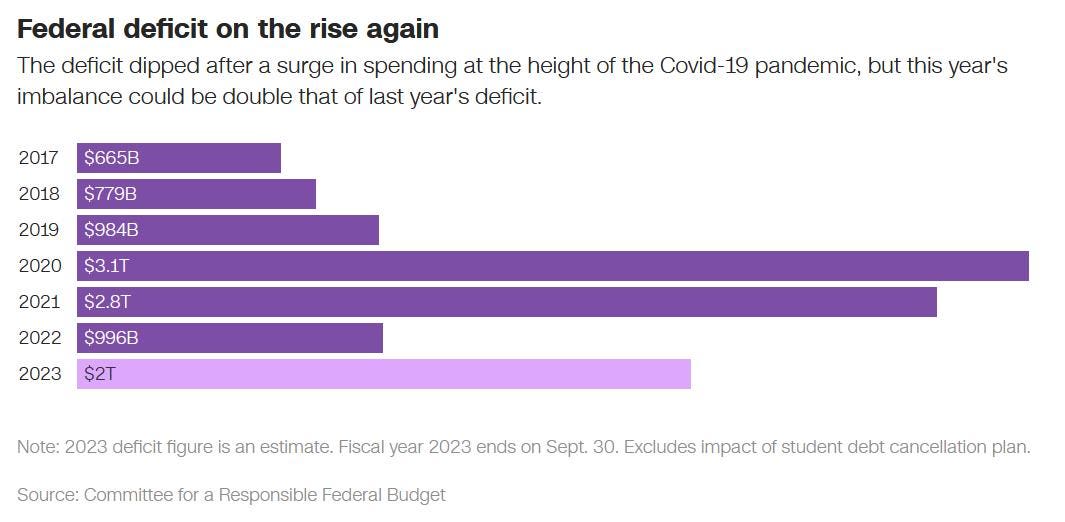

Total Federal spending for fiscal 2023 stands at over $6 trillion with a projected deficit of $2 trillion by the nonpartisan Committee for a Responsible Federal Budget (CRFB). This marks a reversal from last year’s drop, increasing concerns over deficits, inflation, and spending. The proposed budget for FY24 is $6.9 trillion, fanning the flames of the debate over allocations and deficit levels. The 19% inflation experienced since January 2020 is permanent. There are no deflationary plans to bring back price levels to what they were in 2020. Our best hope, therefore, is only to slow the amount that inflation continues to increase in the future. At the long-term average inflation rate of 3% since the formation of the CPI index in 1919, a dollar depreciates to 74 cents in a decade, and to 22 cents in 50 years.

The dollar has lost over 96% of its value since the Federal Reserve was founded in 1913. Investors are encouraged to strategize for long-term preservation and growth amidst the prevailing economic inflation scenario.

1. Budget Overview:

- Fiscal 2023:

- Projected Budget: $5.8 trillion (vs over $6 trillion actual)

- Discretionary Spending: $1.6 trillion

- Projected Deficit: $1.2 trillion (vs $2 trillion estimated by CRFB in September)

- Proposed Fiscal 2024:

- Projected Budget: $6.9 trillion

- Increase from FY23: $1.1 trillion

- Projected Deficit: $1.8 trillion (26% of the proposed budget)

2. Economic Projections & Deficit Impact:

- President Biden’s budget proposal is anticipated to curtail the deficit spending by approximately $3 trillion over the next decade which sounds impressive but may be more political since the deficit over the same period is still projected to grow by $17.1 trillion.

- Economic expansion is projected at 3.8% nominal rate in 2023 and 3.9% nominal rate in 2024, underscored by growing concerns over the pace of debt and deficit which are growing much faster than the economy.

3. Inflation Outlook:

Milton Friedman said the only reason for inflation is the government printing of money. He referred to inflation as “taxation without representation.”

“There is one and only one basic cause of inflation: too high a rate of growth in the quantity of money—too much money chasing the available supply of goods and services. These days, that cause is produced in Washington, proximately, by the Federal Reserve System, which determines what happens to the quantity of money; ultimately, by the political and other pressures impinging on the System, of which the most important are the pressures to create money in order to pay for exploding Federal spending and in order to promote the goal of “full employment.” All other alleged causes of inflation—trade union intransigence, greedy business corporations, spend-thrift consumers, bad crops, harsh winters, OPEC cartels and so on—are either consequences of inflation, or excuses by Washington, or sources of temporary blips of inflation.” – Milton Friedman

- The recent inflation surge stems from extensive money printing during the Covid crisis to offset federal budget deficits. Inflation is projected to stabilize to 3.4% by the end of 2023 and possibly to 2.3% in the subsequent years.

4. Investor Considerations:

- The prevailing fiscal environment and projected economic metrics necessitate astute investment strategies. A focus on long-term growth is imperative to navigate the permanently diminishing value of the currency.

- A structured, well-informed investment approach is crucial to counterbalance the potential fiscal challenges and leverage the arising opportunities.

- Areas receiving the most federal dollars are Education (13% increase), Health and Human Services ($11% increase), the EPA (19% increase), and the Treasury (15% increase).

Conclusion:

- The evolving fiscal landscape, marked by significant over budget allocations and persistent deficits, demands prudent investment strategies. Balancing risk and opportunity while focusing on value preservation and long-term growth is paramount in the current economic context.

- If Congress pulls back sharply on spending, or if there is another negative shock to the economy, the potential for job losses, deleveraging, and lower prices on risk assets remains high. Whenever the Federal Reserve begins the next rate cut cycle, long dated bonds stand to benefit.

- With the recent rise in interest rates, the bond market may offer an opportunity to break even with inflation, but experience no real growth. If the interest earned is consumed, there is no inflation hedge. Growing companies with pricing power and limited debt may enable the equity markets to overcome the downward pressure of inflation, although volatility is historically higher.

In 2002 Equitas Capital Advisors, LLC was established as a unique company that blends the resources of a large global corporation with the flexibility of a small boutique firm. The registered service mark of Equitas Capital Advisors is Engineering Financial Solutions® and the purpose of Equitas is to design, build, and deliver investment solutions to meet the goals and objectives of our investors. Equitas Capital Advisors, LLC located in New Orleans, has over 260 years of combined investment management consulting experience providing professional investment management services to investors such as foundations, endowments, insurance companies, oil companies, universities, corporate retirement plans, and high net worth family offices.

Disclosures and Disclaimers:

Above information is for illustrative purposes only and has been obtained from reliable sources but no guarantee is made with regard to accuracy or completeness. It is not an offer to sell or solicitation to buy any security. The specific securities used are for illustrative purposes only and not a recommendation or solicitation to purchase or sell any individual security.

Equitas Capital Advisors, LLC is registered as an investment advisor with the U.S. Securities and Exchange Commission (“SEC”) and only transacts business in states where it is properly registered, or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the advisor has attained a particular level of skill or ability.

Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the author on the date of publication and are subject to change. This publication does not involve the rendering of personalized investment advice.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment or strategy will be profitable or equal to past performance levels. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals, and economic conditions may materially alter the performance of your portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for an investor. Charts and references to returns do not represent the performance achieved by Equitas Capital Advisors, LLC, or any of its clients.

Asset allocation and diversification do not assure or guarantee better performance and cannot eliminate the risk of investment losses. All investment strategies have the potential for profit or loss. There can be no assurances that an investor’s portfolio will match or outperform any particular benchmark. Past performance does not guarantee future investment success.

Read the full article here