Even if you love your bond fund, you have had to be patient because bonds’ market values decline as interest rates rise. It isn’t fun to watch your share price go down. Then again, if the fund’s yield is high and you are being paid monthly, it is much easier to wait.

The River Canyon Total Return Bond Fund has about $500 million in assets and a five-star rating (the highest) in Morningstar’s “Multisector Bond” category. Canyon Partners is based in Dallas and manages about $24 billion, mostly in hedge funds.

During an interview, Sam Reid, one of the fund’s portfolio managers, explained how it is able to make use of the credit analysis and underwriting employed by the firm’s hedge funds within the River Canyon Total Return Bond Fund without the restrictions on the timing or size of redemptions that hedge funds typically employ.

The River Canyon Total Return Bond Fund quoted an SEC 30-day yield of 6.65% as of June 30 for its institutional shares RCTIX, net of annual expenses that come to 0.66% of the fund’s assets under management. But over the past 12 months, the monthly payouts have totaled 75.5 cents a share, which works out to a distribution yield of 7.53%, based on Wednesday’s closing price of $10.03. And the most recent monthly dividend, paid on July 28, was 77.3 cents a share, which if annualized would make for a distribution yield of 7.71%.

The fund’s shares are distributed through investment advisers but you can also purchase them directly through brokerage platforms, such as Charles Schwab, for example, for a fee of about $50.

The River Canyon Total Return Bond’s performance benchmark is the Bloomberg U.S. Aggregate Bond Index, which has a yield to maturity of 5.14% and a portfolio duration of 6.3 years, according to FactSet. The fund’s portfolio yield is about 8.3% (which is before expenses), and its duration is 2.8. The duration helps investors to understand how much volatility to expect as interest rates move up and down. If interest rates move up by 1%, the market value of the benchmark index can be expected to decline by 6.2%, while the market value of the shorter-duration fund would decline 2.8%.

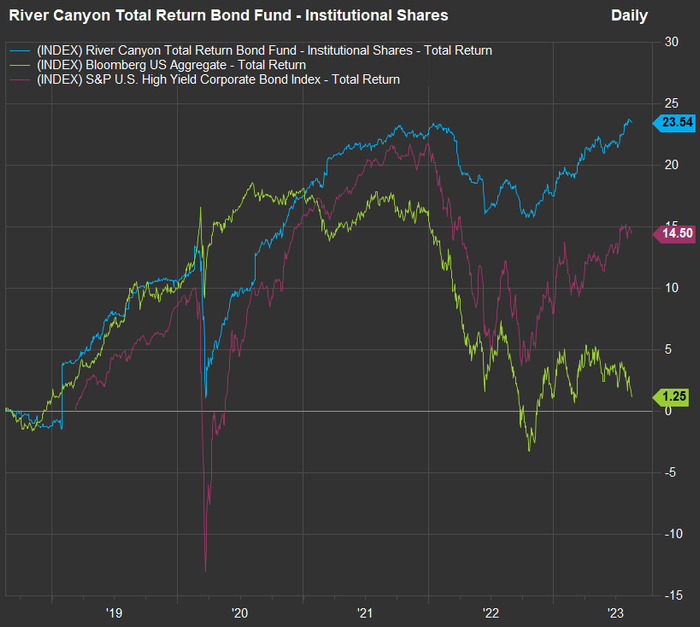

For a one-year performance comparison, we can add the S&P U.S. High Yield Corporate Bond Index, which has a yield to maturity of 8.76% and a duration of 4.2 years, according to FactSet:

And now let’s look at five-year total returns:

At the end of June 27% of the fund was invested in securities rated BBB or higher by Standard & Poor’s or Baa or higher by Moody’s, which are considered “investment-grade.” But the fund’s guidelines for having at least 35% of its assets invested in investment-grade securities include those that are rated such by other entities, including Fitch, DBRS Morningstar, and Kroll. With those added in, 43.5% of the fund’s assets were considered investment-grade as of June 30, according to River Canyon Fund Management.

Reid explained that the firm’s hedge-fund managers were focused on all aspects of credit, especially specialized structures used to help troubled companies. He also said that the River Canyon Total Return Bond Fund is focused on “more liquid and more defensive strategies” than those employed by the hedge funds operated by Canyon Partners.

He said that “50% of the fund has to be in what we categorize as highly liquid investments, by virtue of our single-day liquidity,” offered to investors in the fund.

He further explained that with the growth of private credit, “it can take years to get your money out,” if you invest in a hedge fund that is involved with providing distressed financing to companies or even to local governments.

One focus of the fund is financing companies going through bankruptcy. “If a company goes into bankruptcy, often they need a bridge. They issue debtor-in-possession securities, at the top of the stack, 12 to 18 months; they don’t get rated,” Reid said.

The “stack” refers to a company’s capital structure. If a company goes bankrupt it might be able to continue to operate after the bankruptcy process is completed, in which case the debtor-in-possession securities will be paid-off in full. But if the company has to be liquidated, secured creditors are paid before stockholders (if there is any money left for the stockholders). Among the creditors, there will be senior and junior liens, so they have to get in line as well. Reid emphasized that debtor-in-possession securities held by the fund (which are often underwritten by Canyon Partners with financing through its hedge funds) are first to be paid if a company is unable to emerge from bankruptcy.

The debtor-in-possession securities’ yields are typically set at the Secured Overnight Financing Rate (SOFR) plus 500 basis points, Reid said. That most recent SOFR rate posted by the Wall Street Journal was 5.3%, which would make for a 10.3% rate on a newly issued security of this type.

These securities can often be purchased at discounts to face value, “adding a total return component” to the investments because they are expected to be repaid relatively quickly, Reid said.

So the fund is very much operating within the high-yield or “junk” space, and as you can see from the returns above, the strategy has worked out well in an environment that has led to volatility for bond prices.

One thing to keep in mind is that if the fund keeps defaults to a minimum, its low duration means that bonds whose market values have fallen will rise to their face value as they near maturity. So the effect of rising rates on the value of its securities holdings will be minimized.

Of course, interest rates won’t go up forever. When asked what might happen if the Federal Reserve were to change course and begin lowering interest rates rapidly to spur economic growth, Reid said that if the yield on 10-year U.S. Treasury notes

BX:TMUBMUSD10Y

were to drop this year to 2.00% from its current level of about 4.29%, “we would probably deliver similar returns to what the [Bloomberg] Aggregate would give you,” because the index’s higher duration means its market value would rise more quickly.

“But next year I would have a higher yield. The starting point next year for [the Bloomberg Aggregate] would be 2%,” he said.

When asked about his strategy two years ago, when short-term rates were near zero, 10-year Treasury notes were yielding 1.26%, the Bloomberg U.S. Aggregate had a yield to maturity of 1.44% and the S&P U.S. High Yield Corporate Bond Index had a yield to maturity of 4.45%, Reid said he was targeting yields of 5% to 7%. “The target will change. The duration will change,” he said, adding that the fund’s duration was unlikely to exceed four years.

When discussing the fund and its performance, Reid emphasized the advantage from the firm’s expertise in credit underwriting for its hedge funds.

“If you have a manager who understands credit, can take apart a balance sheet and understand credit documents, you can underwrite more complex investments, understand why a yield might be higher and understand the creditworthiness without relying on a rating,” he said.

Don’t miss: These 20 dividend stocks have been the best income growers in the S&P 500

Read the full article here