Carrier Global (NYSE:CARR) is a leading manufacturer of HVAC, refrigeration, and Fire & Security systems. Carrier was spun off from United Technologies in April 2020. Their portfolio includes industry-leading brands such as Carrier, Toshiba, Automated Logic, Carrier Transicold, and Kidde, among others. Carrier is currently in the process of transforming its portfolio, with plans to divest its Fire & Security and Commercial Refrigeration divisions in order to focus on higher growth areas like Climate Solutions and Heat Pumps. I believe this portfolio transformation has the potential to accelerate their revenue growth and expand margins over the next few years. Therefore, I give Carrier a ‘Strong Buy’ rating.

Viessmann Climate Solutions Acquisition: Heat Pumps

Carrier announced its acquisition of Viessmann Climate Solutions for €12 billion in cash and stock on April 25th, 2023. Viessmann Climate Solutions is a leading manufacturer of heat pumps in Europe, and I believe that heat pumps will become a significant growth driver for Carrier in the near future.

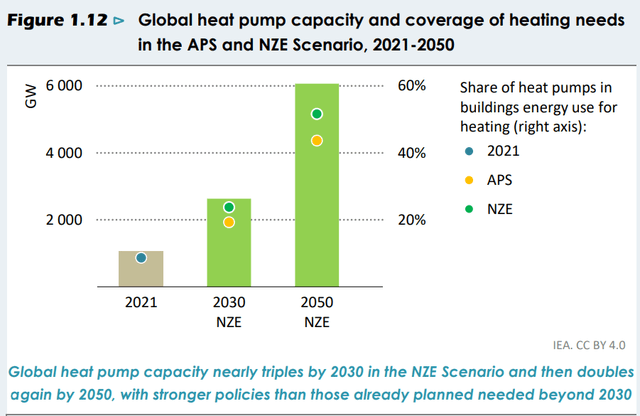

According to the European Commission, nearly 50% of all energy consumed in the EU is used for heating and cooling. Heat pumps are considered a mature technology that offers greater efficiency compared to boilers. The International Energy Agency published a report titled ‘The Future of Heat Pumps’ in which they forecast that global heat pump capacity will nearly triple by 2030 in the Net Zero Emissions Scenario and then double again by 2050.

International Energy Agency

I believe that the global heat pump market will experience tremendous growth, especially in Europe and the United States, where governments are prioritizing renewable energy initiatives.

Planned Exit of Fire & Security and Commercial Refrigeration Businesses

Carrier expects to exit its Fire & Security and Commercial Refrigeration businesses during 2024 and shift its focus to climate solutions with an accelerated growth profile. The Refrigeration and Fire & Security businesses currently account for approximately 35% of the group’s revenue. Historically, their growth rates have been lower and more volatile compared to the climate HVAC business.

The Refrigeration business serves various markets, including containers, trucks/trailers, cargos, and other commercial refrigeration markets. I believe these end-markets exhibit higher volatility than HVAC end-markets due to their connection with capital expenditure cycles.

Additionally, the Fire & Security business sells fire detection and security-related products to both residential and commercial buildings. This market is highly competitive, with numerous brands offering similar products. In summary, my preference lies with Carrier’s HVAC business.

Carrier 10Ks

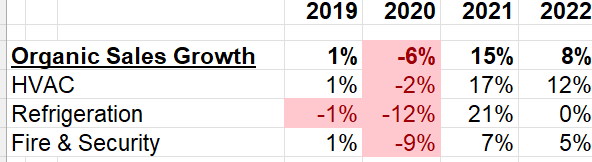

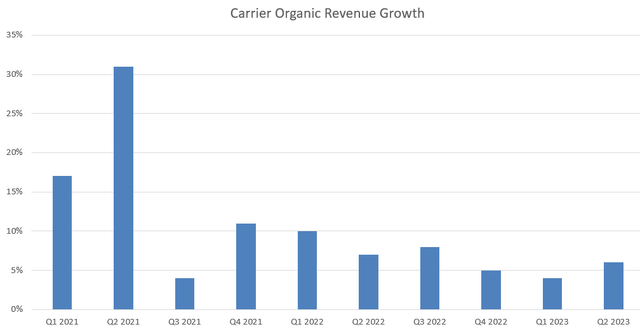

Therefore, I believe that this portfolio transformation makes strategic sense. The new Carrier will be dedicated to HVAC and Heat Pump business lines, addressing the global climate change challenge and benefiting from structural growth tailwinds. Carrier’s HVAC business has shown significant growth in the past two years, with an organic increase of 17% in FY21 and 12% in FY22.

HVAC Business Growth

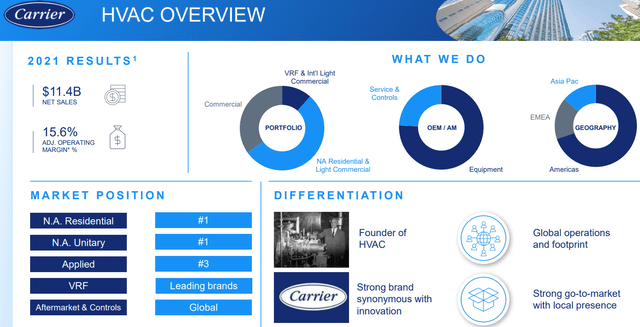

Carrier’s HVAC business is a leader in the North American residential and unitary markets, with globally recognized brands.

Carrier 2022 Investor Day

Based on my research and assessment, the competitive landscape in the HVAC market appears highly stable, with existing players demonstrating rational competition. According to Fortune Business Insights, the global HVAC market is projected to increase from $150 billion in 2022 to $228 billion by 2030, reflecting a compound annual growth rate of 5.5% during the forecast period. Notably, Carrier’s HVAC business boasts the highest operating margin among their current business segments. The higher growth rate expected in the HVAC sector has the potential to contribute to Carrier’s overall group margin expansion.

Financial and Outlook

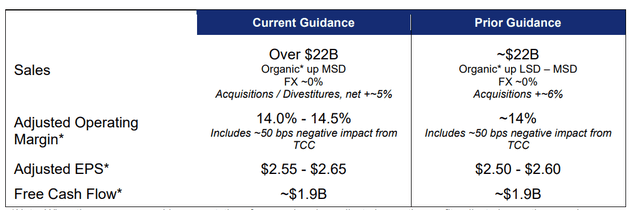

In Q2 FY23, Carrier achieved a 6% organic revenue growth, accompanied by an impressive 11.8% year-over-year increase in adjusted operating profits. As a result, they have raised their full-year guidance.

Carrier Q2 FY23 Earnings

I believe it was a strong quarter for Carrier, especially considering the current weak macroeconomic environment. Their HVAC business demonstrated robust organic revenue growth of 9%, while their Refrigeration business continued to experience slower demand, with a -6% organic growth rate.

Carrier Quarterly Results

Furthermore, Carrier’s management has indicated that their backlog remains significantly above historical levels, with a 30% year-over-year increase. They are guiding for $1.9 billion in free cash flow for the full year of FY23.

In my view, when Carrier completes its portfolio transformation in 2024, the company should become more resilient with a better growth trajectory and improved margin profile. This transformation will help reduce the cyclicality associated with their Refrigeration and Fire & Security business lines.

Key Risks

Debt Deleveraging: Carrier is actively engaged in reducing its debt load. In FY20, the company carried over $10 billion in long-term debt, and they are targeting a reduction to $4 billion in the near future, which would result in a 2.1x net debt leverage ratio. This suggests that their overall debt structure is manageable. Additionally, they are poised to gain proceeds from the divestiture of their Fire & Security and Commercial Refrigeration businesses, further supporting their deleveraging efforts.

Weak New Residential Housing Market: In Q2 FY23, Carrier’s North America residential HVAC business experienced a mid-single-digit decline, which was below their initial expectations. They also highlighted an overall mid-teens decline in residential HVAC volumes for the quarter. I hold the view that the North America residential housing market is not likely to recover in the near future. Therefore, I anticipate that Carrier’s HVAC business in the North America residential end-markets will remain weak in the short term.

Valuation

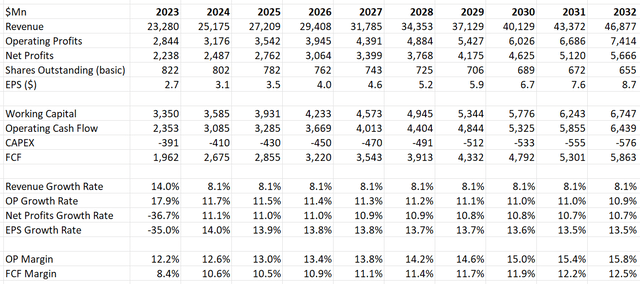

In my model, I anticipate that the Carrier will achieve organic revenue growth of 6% in FY23, followed by 7% in the subsequent years. Acquisitions are expected to contribute 8% to growth in FY23 and 1% in the following years.

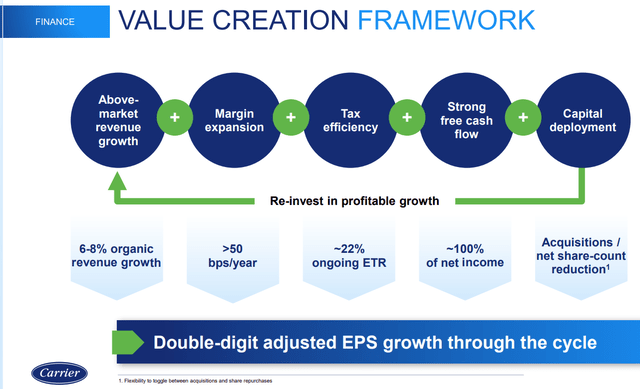

I have confidence that their projected 6-8% organic revenue growth, coupled with more than a 50 basis points margin expansion per year, can result in double-digit earnings growth over the next decade.

Carrier 2022 Investor Day

The operating margin is forecast to expand to 15.8% by FY32 and free cash flow to reach $5.8 billion.

Carrier DCF Model – Author’s Calculation

Using a 10% discount rate, a 4% terminal growth rate, and a 25% tax rate, I’ve discounted all the free cash flows from the firm and adjusted for cash and debt. Based on this analysis, the fair value of their stock price is estimated to be $60 per share.

Wrap-Up

I applaud Carrier’s strategic transformation of their business portfolios, with a focused approach on HVAC and Heat Pump segments, which I believe can drive accelerated organic revenue growth and margin expansion. Given what appears to be an undervalued stock price, I give it a ‘Strong Buy’ rating.

Read the full article here