Sea Limited (SE) soared on Monday on news that the Indonesian government may be seeking to issue a new regulation on “social commerce.” SE had traded weakly heading into this news due to management appearing to reverse course on the progress made on the profitability front. SE had previously aimed to offset decelerating revenue growth with strict cost discipline and appeared to achieve some success in these efforts, generating GAAP profits for three straight quarters. Management discussed intentions to reinvigorate growth in its e-commerce segment in a “disciplined” manner but Wall Street has shown great skepticism given the company’s relatively brief track record of profitability. The stock is looking cheap here regardless of what happens in Indonesia, though the company direction remains a wildcard.

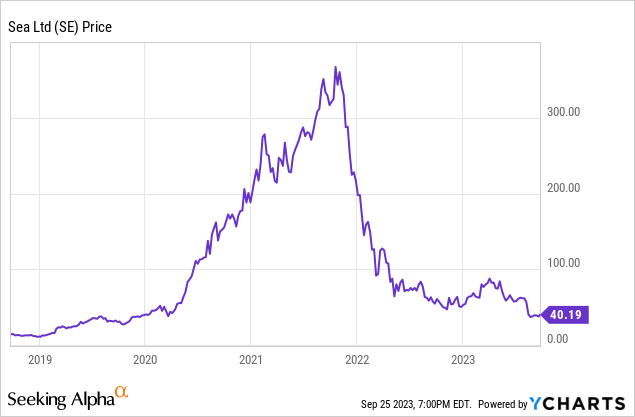

SE Stock Price

SE peaked above $350 per share during the pandemic tech bubble. The stock has since crashed around 90% and continues to trade at these low levels.

I last covered SE in July where I rated the stock a buy due to the shift to profitability. In hindsight, this rating was misguided as my calculated fair value offered insufficient margin of safety. After the 34% plunge since that report though, the stock is offering compelling value, highlighted by a strong balance sheet.

SE Stock Key Metrics

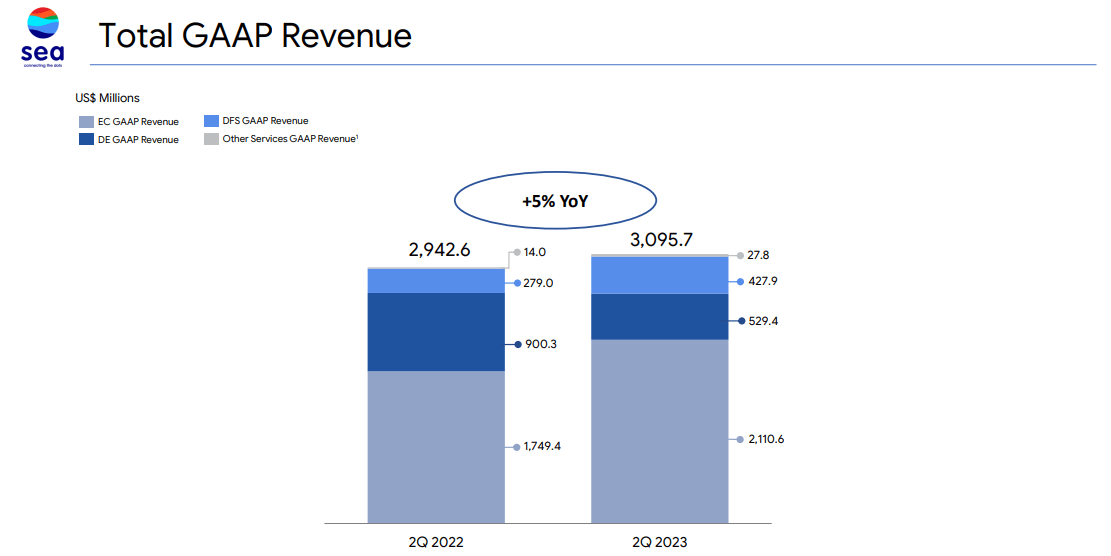

In its most recent quarter, SE delivered 5% YoY revenue growth – a far cry from the hyper-growth reported during the pandemic but understandable given the tough macro environment. The swift rise in interest rates has exposed SE as being a large beneficiary from the low interest rates as higher cost of capital has limited the effectiveness (and implementation) of promotional activity.

2023 Q2 Presentation

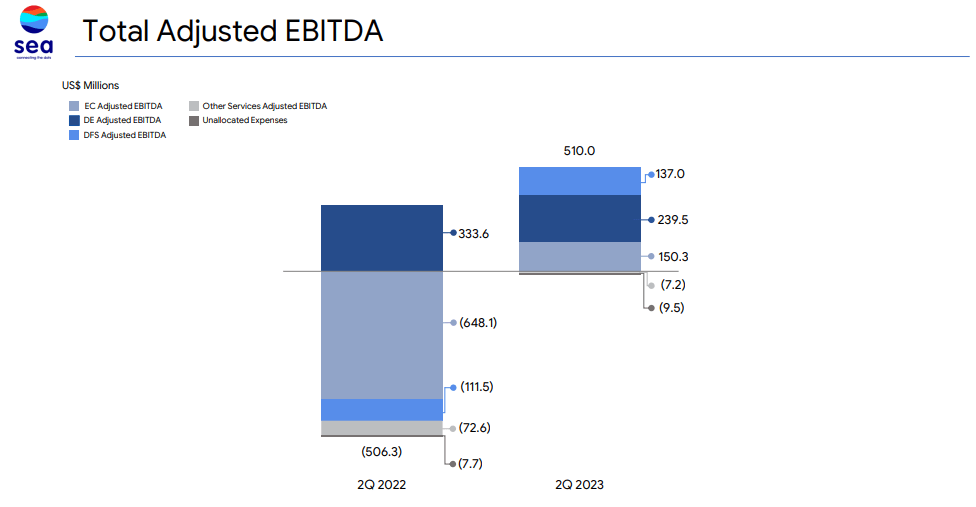

SE saw adjusted EBITDA rise to $510 million on a consolidated basis, up from the $506 million adjusted EBITDA loss in the prior year.

2023 Q2 Presentation

SE was even able to report $331 million in GAAP net income, up from the $931 million net loss in the prior year. The slowdown in revenue growth was disappointing, but with the stock undergoing a brutal valuation reset, the shift to GAAP profitability should have been enough (but commentary on the conference call nullified this, as we’ll discuss later).

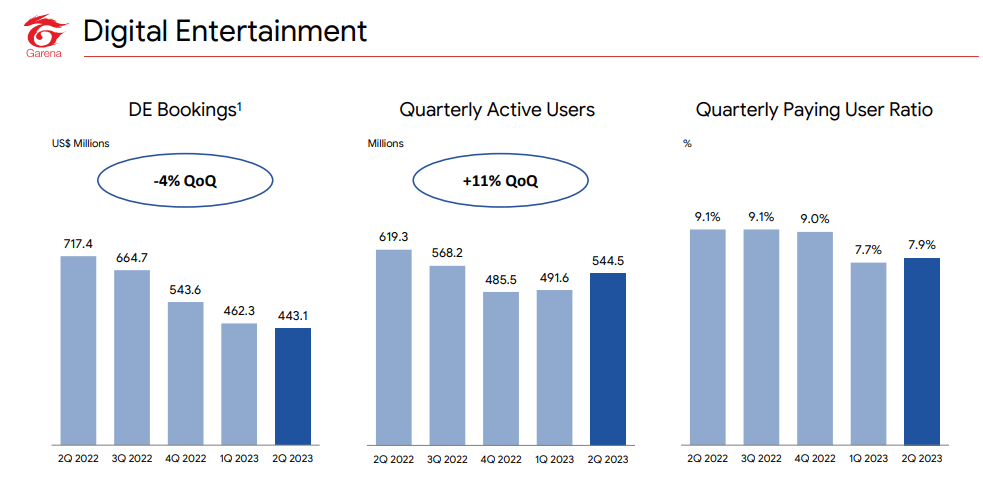

As usual, SE saw continued weakness in its video game segment with bookings declining 38% YoY. It is worth noting that digital entertainment bookings peaked at $1.2 billion in the third quarter of 2021. Adjusted EBITDA declined by nearly $100 million in this unit.

2023 Q2 Presentation

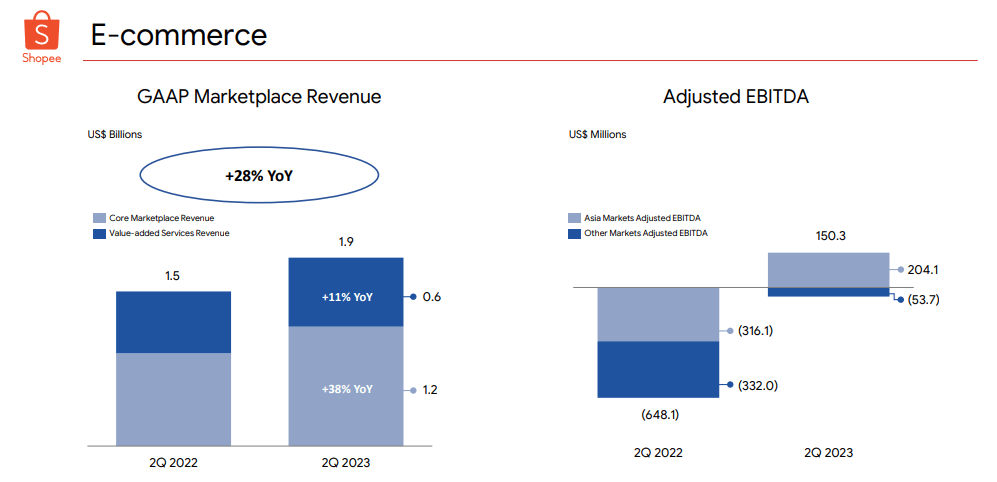

Historically, digital entertainment has been the cash cow for the business, helping to offset the losses generated by e-commerce operations. That narrative has flipped, with the company generating 28% YoY growth in e-commerce revenues (largely driven by take rate expansion) and seeing its adjusted EBITDA swing from a $648 million loss to $150 million profit.

2023 Q2 Presentation

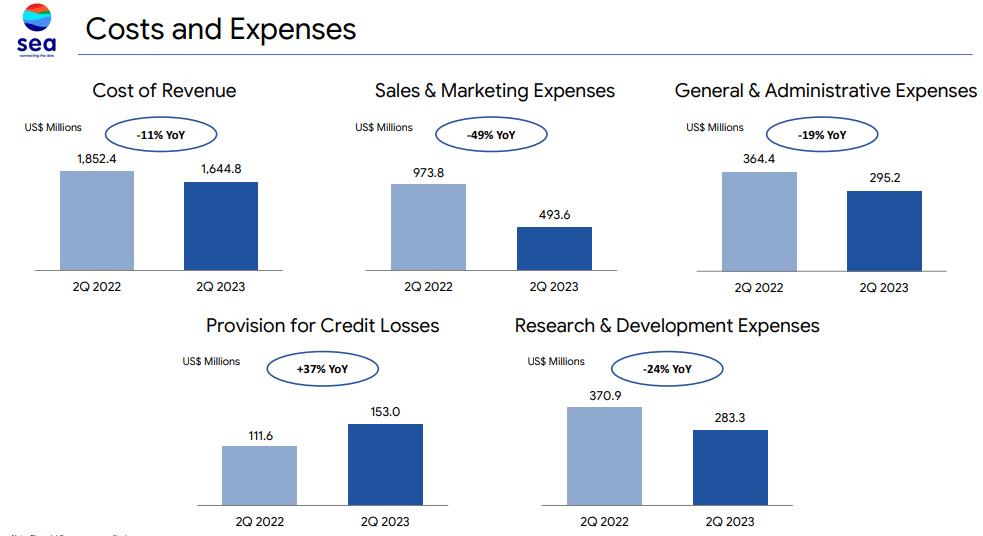

I must emphasize that the bulk of the top-line growth was driven by take rate expansion as investors should temper expectations for top-line growth moving forward for this segment. SE delivered its profitability gains through both operating leverage as well as aggressive cost discipline, highlighted by a 49% YoY reduction in S&M expenses.

2023 Q2 Presentation

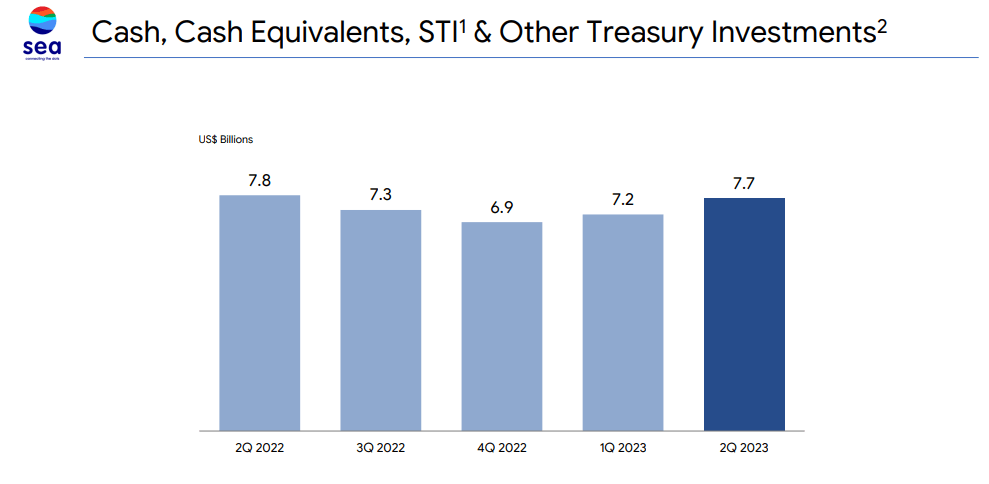

SE ended the quarter with $7.7 billion of cash and investments versus $3.4 billion of debt. The stock recently traded hands at around a $22 billion market cap.

2023 Q2 Presentation

On the conference call, management noted that they “have started, and will continue, to ramp up our investments in growing the e-commerce business.” Management expects this investment to lead to losses for both Shopee (the e-commerce business) as well as the company “in certain periods.” This shift in capital allocation caught investors off guard and appears inconsistent with the progress made in the last several quarters. While management stressed that they will continue to possess “unwavering emphasis on self-sufficiency,” the change in investment direction felt like a gamble that Wall Street would just believe in management after three quarters of GAAP profits. Yes, the past three quarters have been particularly impressive, but this track record is short and there has not been enough visibility in the company’s ability to balance growth and profitability on a long-term basis. Personally, I would have preferred a more consistent focus on profitability with the aim of only increasing growth ambitions upon a material improvement in the macro environment. At the very least, SE still has a robust net cash position that can help support losses in the near term. We will have to see in the upcoming quarters just how aggressively management intends to invest in growth.

Why Is Sea Stock Rising?

SE stock soared double-digits on Monday amidst reports that the Indonesian government could issue regulations on social commerce. Some investors may be confused by the stock price’s reaction – management even stated on the conference call that they were “the leading live streaming e-commerce platform in Indonesia,” but focus should be on competition from TikTok. TikTok has been a formidable competitor on a global scale and may have been forcing SE to invest in social media creators, holding back profit margins. Investors may be hoping that this regulation may help to both accelerate revenue growth due to lower competition, as well as boost profit margins due to lower investment in social commerce.

Is SE Stock A Buy, Sell, or Hold?

SE at one point traded as one of the most expensive stocks in the tech sector. Now, it is trading at value multiples, with the stock recently trading hands at around 18x earnings.

Seeking Alpha

Net cash makes up around 20% of the market cap, but probably should be excluded from fair value calculations due to management’s intent to invest aggressively in e-commerce growth. In my prior report, I arrived at $35 billion in fair value for the stock. The stock is trading at around a $22 billion market cap, implying solid upside to that target.

What are the key risks? The main risk at this point centers around just how aggressively the company invests in e-commerce growth. The company has a track record of unprofitable growth and investors may be fearful that management will return to those unprofitable ways. I retain hopes that management is committed to more profitable growth, but like others would like to see evidence of that commitment moving forward. The company’s video game segment appears to be stabilizing, but the apparent stabilization has only occurred for one quarter and may prove to be an illusion. In this higher interest rate environment, I wouldn’t be surprised if SE stock sees its valuation compress dramatically in the event that it ends up reversing course on profitability, as investors are unlikely to assign it the same nosebleed valuations as during the pandemic.

I am sticking by my buy rating due to the conservative valuation and ample net cash, but note that I am purposefully avoiding a strong buy rating given the potential for increased losses ahead and low visibility in a return to sustainable growth.

Read the full article here